The trade balance in May 2026 remained in a large deficit due to the impact of the Middle East war, though the severity appears to have passed its trough.

SCB EIC expects Thai exports to perform better than previously anticipated and has revised up its 2026 export value growth forecast to 10%

Overall, Thai exports in May 2026 slowed significantly.

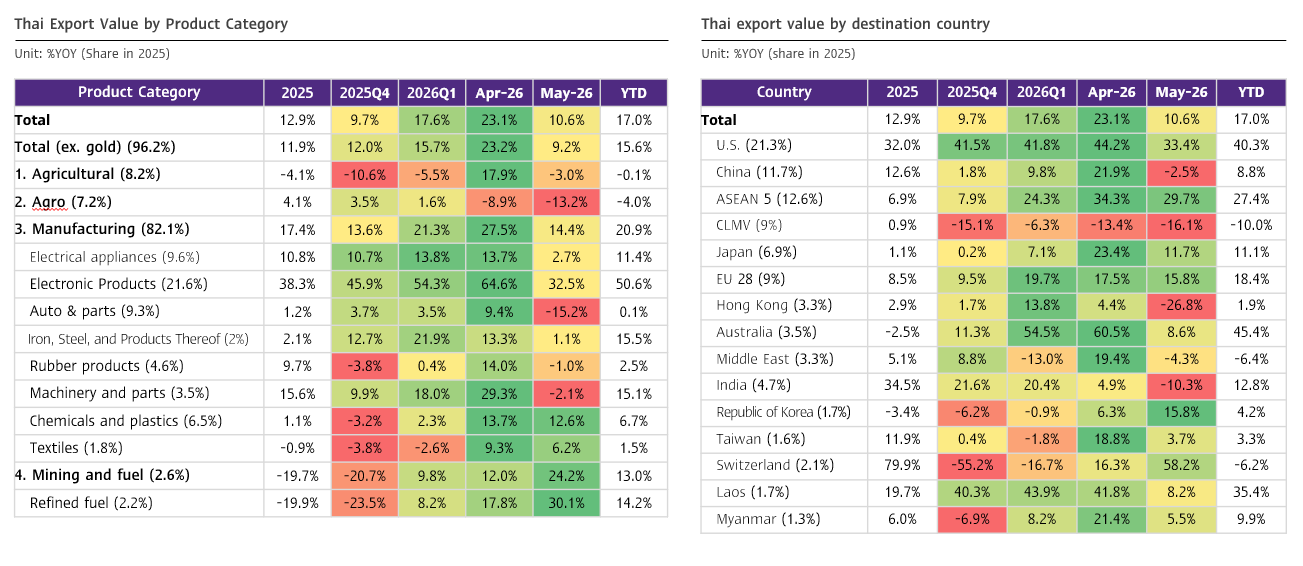

Export value in May 2026 stood at USD 34,333.1 million, expanding by 10.6%, slowing sharply from 23.1% in the previous month, but slightly exceeding expectations (SCB EIC estimated 8.8%, while the Reuters Poll median was 12%). Seasonally adjusted export value contracted for the first time in 3 months by -3.5%MOM_SA. Overall, Thai export value during the first 5 months of 2026 still expanded by 17%.

Exports this month were supported almost entirely by electronic products and a renewed wave of front-loading shipments to the US ahead of the implementation of new tariff measures under Section 301.

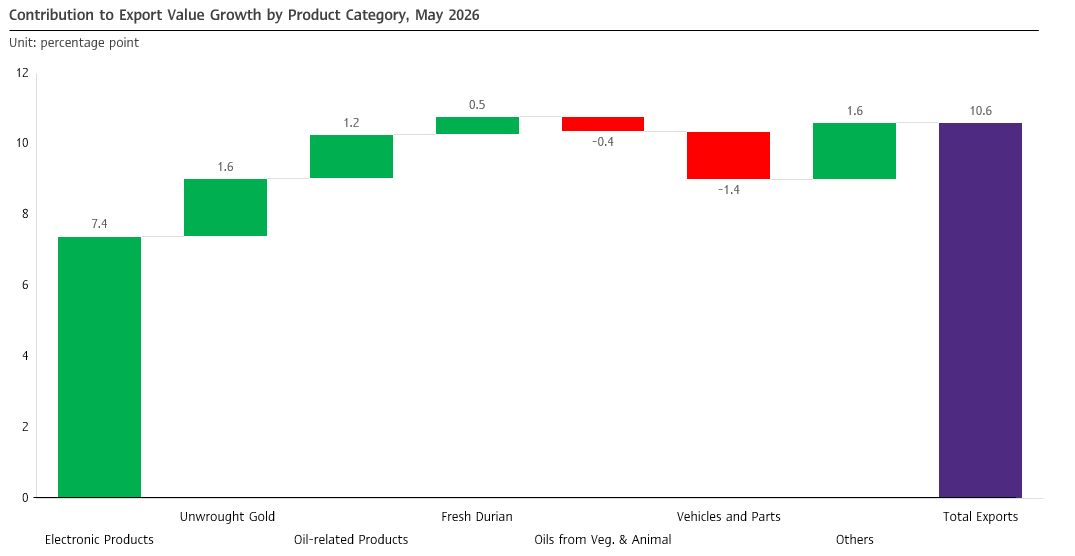

(1) Electronic product exports continued to expand strongly by 32.5%, despite slowing from 64.6% in the previous month, partly due to a high base effect. This marked continued expansion for 2 years and 2 months. This product group continued to be supported by the electronics upcycle, in line with the global expansion trend in investment in the electronics industry and data centers, as well as front-loaded orders amid concerns over supply chains and rising costs. This was reflected in exports of this product group to 12 out of Thailand’s 15 key trading partners continuing to expand strongly. Electronic products contributed 7.4% to Thai export growth this month, accounting for almost all of the total export growth of 10.6%.

(2) Exports to the US expanded strongly by 33.4%, despite slowing from 44.2% in the previous month. Exports of electronic products not yet subject to additional US import tariffs surged by 70.2% (accounting for 55.1% of Thailand’s total export value to the US this month), while other product groups excluding electronics expanded by 5.5%, reflecting ongoing demand for Thai products in the US market. Exports to the US contributed 6.7% to export growth this month.

(3) Exports of unwrought gold expanded by 55.8%, accelerating from 20.8% in the previous month, driven by exports to the UAE, Singapore, Switzerland, and Hong Kong, which grew strongly by 3,481.3%, 332.2%, 138.5%, and 838.4%, respectively. Unwrought gold exports contributed 1.6% to Thai export growth this month.

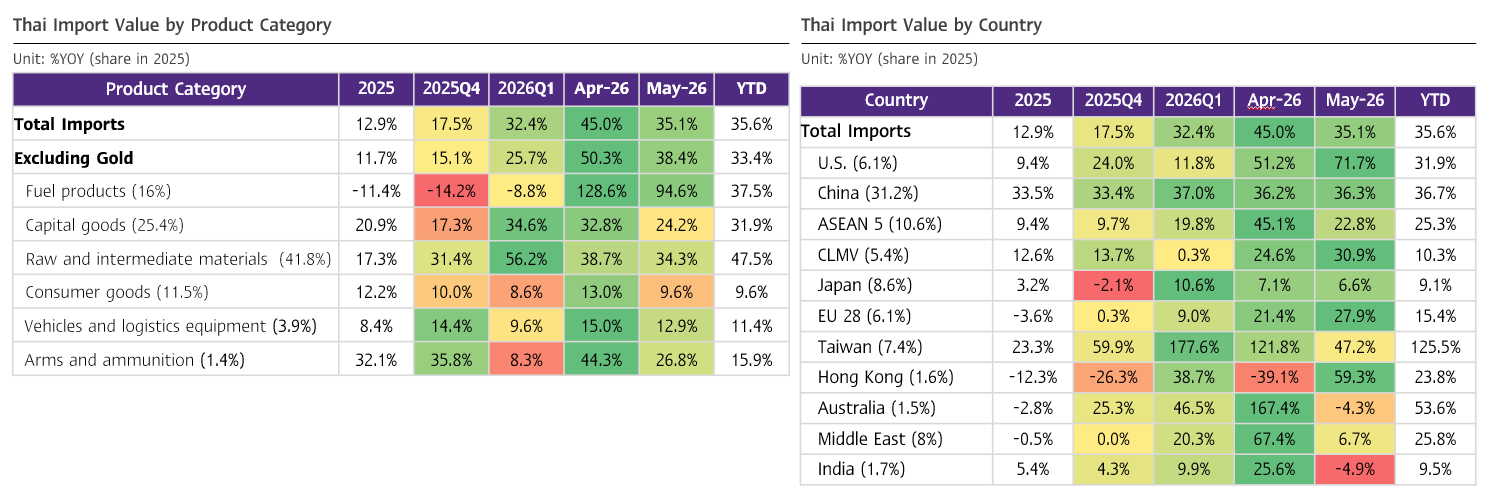

Imports continued to accelerate, driven by raw materials and intermediate goods, as well as fuel products.

Import value in May stood at USD 40,044.5 million, expanding strongly by 35.1%, though slowing somewhat from 45.0% in the previous month and below expectations (SCB EIC estimated 41.2%, while the Reuters Poll median was 35.0%). Overall, Thai import value during the first 5 months of 2026 continued to expand by 35.6%. Major imports this month included the following (Figures 3 and 4):

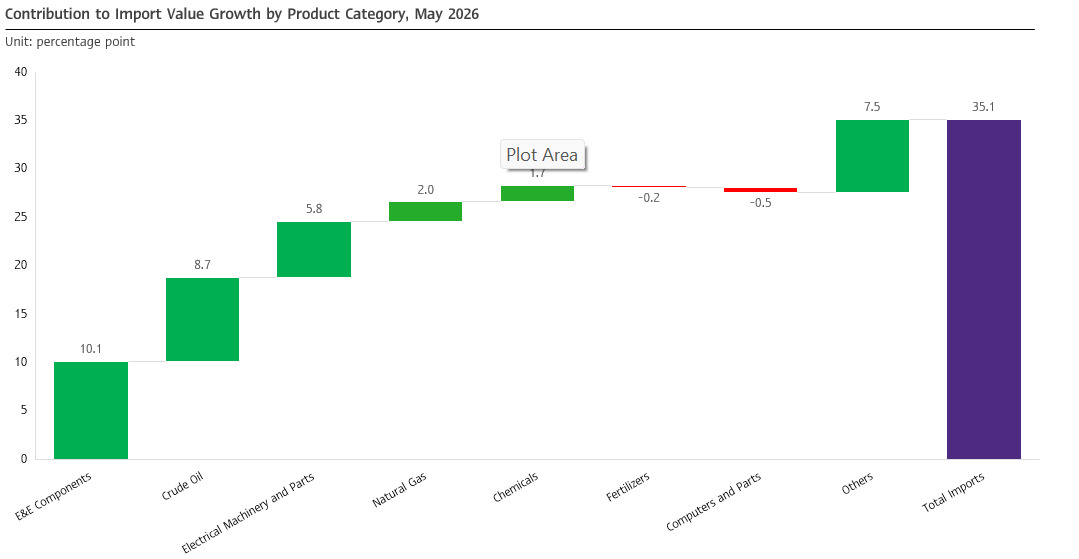

(1) Raw materials and intermediate goods expanded strongly by 34.3%, continuing from 38.7% in the previous month. Imports in this category contributed 15.2% to import growth this month, out of total import growth of 35.1%. Key products included electrical appliance and electronic equipment components, particularly electrical circuit boards, which expanded strongly by more than 101.6% and 121.5%, respectively (CTG: 10.1% and 9.2%). Part of the increase is assessed to reflect demand for upstream and midstream inputs for production and exports, as well as investment demand in Thailand. As a result, Thailand had to import this product group from key producers, particularly China and Taiwan, which expanded by 30% and 149.5%, respectively.

(2) Fuel products expanded strongly by 94.6%, despite slowing from 128.6% in the previous month. Imports in this category contributed 11.2% to import growth this month, out of total import growth of 35.1%. Crude oil imports expanded strongly by 121.5% (CTG: 8.7%), while natural gas imports expanded by 85.4% (CTG: 2%), in line with developments in the Middle East, as global energy prices remained elevated despite moderating somewhat from the earlier period. Most imports came from the US, which expanded by more than 223.9% (accounting for 22.4% of Thailand’s total import value in this category this month).

(3) Capital goods expanded by 24.2%, slowing from 32.8% in the previous month. Imports in this category contributed 6.9% to Thai import growth this month, out of total import growth of 35.1%. Key products included electrical machinery and parts, which expanded by 67.4% (CTG: 5.8%). This may partly reflect Thailand’s limited capacity to produce capital goods in this category, while rising investment trends in technology industries, such as data centers, have increased demand for capital goods imports in machinery and technology categories. This was particularly evident in imports from China, which expanded by 51.2% and accounted for 52.3% of Thailand’s total capital goods import value this month.

The customs basis trade balance remained in deficit at USD -5,711.4 million this month, smaller than expected (SCB EIC estimated USD -8,000 million, while the Reuters Poll median was USD -6,120 million). Thailand’s cumulative trade deficit during the first 5 months of 2026 stood at USD -25,209.3 million.

SCB EIC revised up its 2026 export and import forecasts to 10% and 16.9%, respectively.

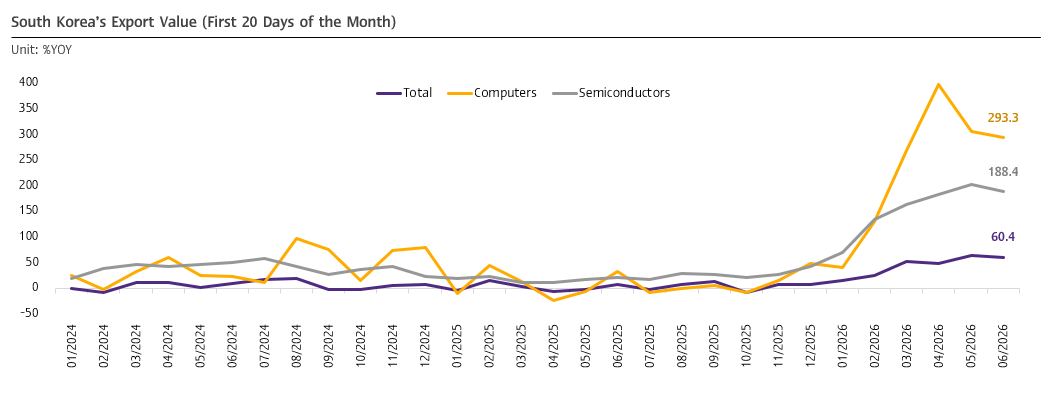

SCB EIC expects Thai exports to perform better than previously anticipated and has revised up its 2026 export value growth forecast to 10% (from the previous forecast of 7.8%, balance of payments basis), supported by the stronger-than-expected outturn in the first 5 months of the year, during which exports expanded by 17%. In addition, electronic product exports are expected to continue expanding strongly. This is reflected in South Korea’s preliminary export data for the first 20 days of June, which recorded robust growth of 60.5%, particularly exports of computers and parts, and semiconductors, which surged by 293.3% and 188.4%, respectively (Figure 5).

Import value this year is expected to expand by 16.9% (from the previous forecast of 15.8%, balance of payments basis), in line with the outturn during the first 5 months of the year, which expanded by 35.6%. This was driven particularly by imports of electronics-related intermediate goods from China and Taiwan, capital goods from China, and higher fuel imports following elevated global energy prices after the Middle East war. As a result, Thailand’s trade balance outlook this year is expected to deteriorate significantly.

SCB EIC views that Thailand’s trade deficit likely passed its trough in April, following the easing of the Middle East war and progress in negotiations between the US and Iran, which have led global energy prices to decline steadily. SCB EIC assesses that the trade balance on a balance of payments basis is likely to gradually return to surplus in H2, while the customs basis trade balance is expected to remain in deficit. This is because the two systems use different calculation standards, while customs-basis imports also include freight costs in import value. However, close monitoring is still needed over whether the war could escalate again and trigger another surge in global energy prices.

Special Topic: US Import Tariffs Under Section 301 Remain a Key Risk to Monitor

On June 2, the US government announced guidelines for imposing import tariffs under Section 301 on forced labour issues, covering 60 trading partners at rates of 10%–12.5% across two groups. The US government is expected to announce the final tariff rates under Section 301 on forced labour issues before July 24, as a replacement measure for the temporary tariffs under Section 122, which are set to expire after 150 days on July 24.

Thailand risks being classified in the group subject to US import tariffs under Section 301 on forced labour issues at a rate of 12.5%, as USTR views that Thailand still lacks clear legal measures to prohibit imports of goods produced using forced labour and has not been able to enforce such measures effectively. However, SCB EIC views that the impact on Thailand will likely be relatively limited, as the tariff rate faced by Thailand would rise from 10% to 12.5% (an increase of only 2.5%) and would still be lower than the 19% reciprocal tariff that the US had imposed on Thailand from the middle of last year until early this year. In addition, data from Global Trade Alert indicate that if the US shifts from tariffs under Section 122 to Section 301 on forced labour issues, Thailand’s average effective tariff rate would be around 14.7%, as some export products are assessed to receive more tariff exemptions under Section 301.

In addition to the Forced Labor case, Thailand is also one of 16 countries currently under US investigation on excess capacity issues for potential additional tariffs under Section 301. This remains a key downside risk that could undermine Thailand’s competitiveness in the US market.

Figure 1: Thai Export Value by Product Category and Key Markets.

Source: SCB EIC analysis based on data from the Ministry of Commerce.

Figure 2: Electronic Products Remained the Main Driver of Thai Exports in May 2026.

Source: SCB EIC analysis based on data from the Ministry of Commerce.

Figure 3: Thai Import Value by Product Category and Key Markets.

Source: SCB EIC analysis based on data from the Ministry of Commerce.

Figure 4: Electronic Components, Crude Oil, and Electrical Machinery Were the Main Imports in May 2026.

Source: SCB EIC analysis based on data from the Ministry of Commerce.

Figure 5: South Korea’s Exports Continued to Expand Strongly in June, Led by Electronic Products.

Source: SCB EIC analysis based on data from the Korea Customs Service.