SCB EIC views that merchandise exports will expand by 1.2% in 2023 as signs of recovery emerge, despite a negative growth of exports in February

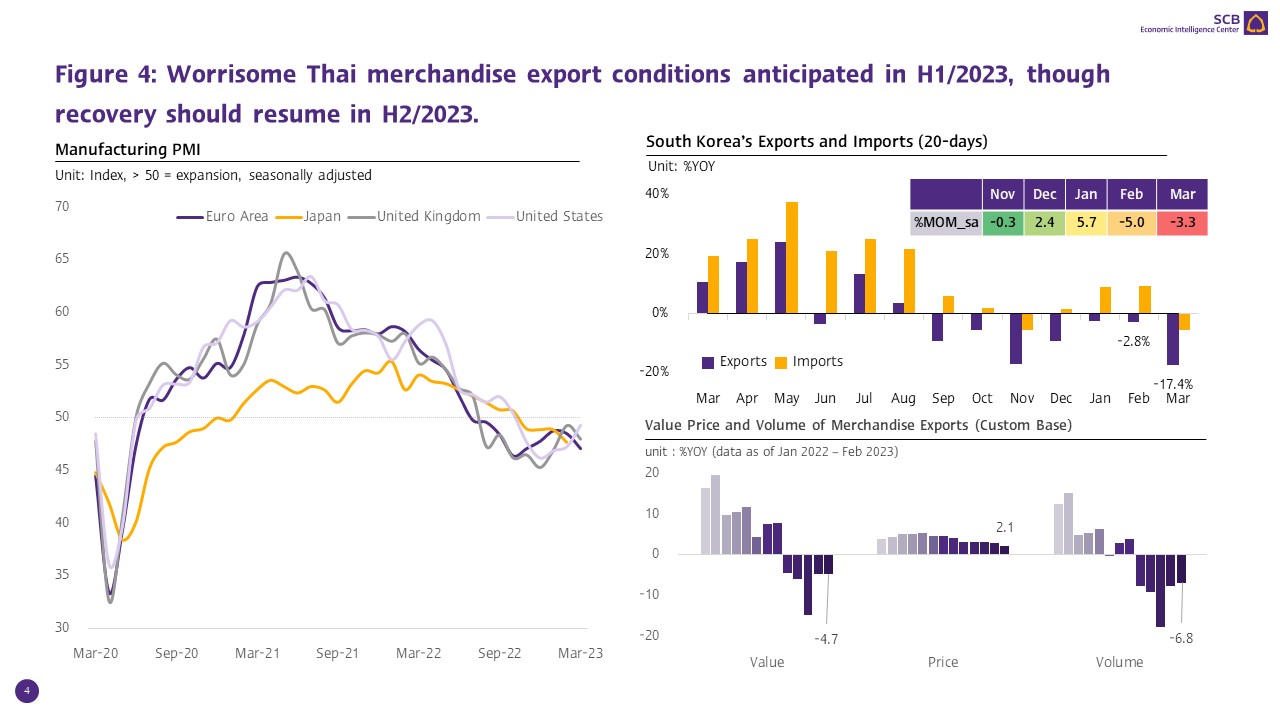

SCB EIC anticipates worrisome merchandise export conditions in H1/2023, though recovery should resume in H2/2023.

Thai merchandise exports contracted in February, marking a fifth consecutive month decline. However, signs of recovery started to emerge.

The value of Thai exports in February 2023 was at USD 22,376.3 million, down by -4.7%YOY. Such growth marked a 5 consecutive months decline, with the contraction slightly decelerating from -4.5%YOY in January. However,

in terms of the seasonally adjusted month-on-month growth, exports in February improved by 3.8%MOM_sa, significantly improved from -3.0%MOM_sa in the prior month. Furthermore, excluding gold (a product that does not reflect actual international trade conditions), Thai exports during the month contracted by merely -2.5%YOY compared to -4.4%YOY in January.

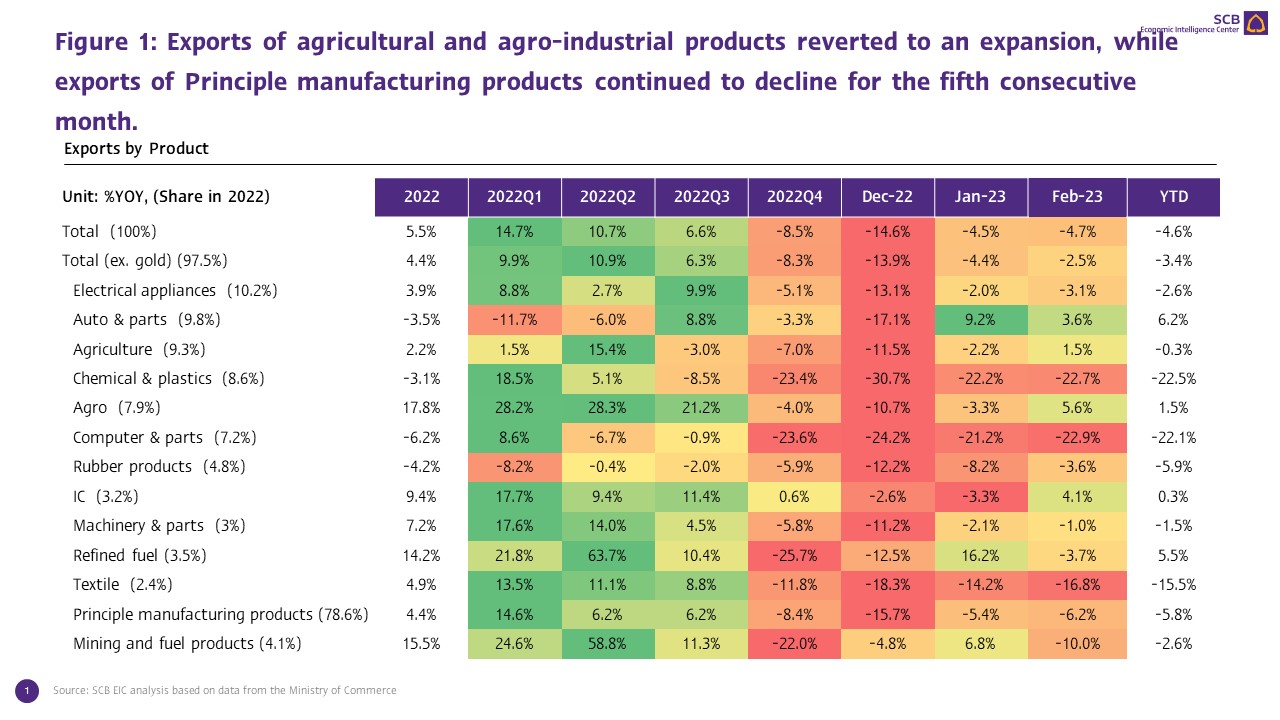

Exports of agricultural and agro-industrial products returned to an expansion, while exports of principle manufacturing products continued to shrink.

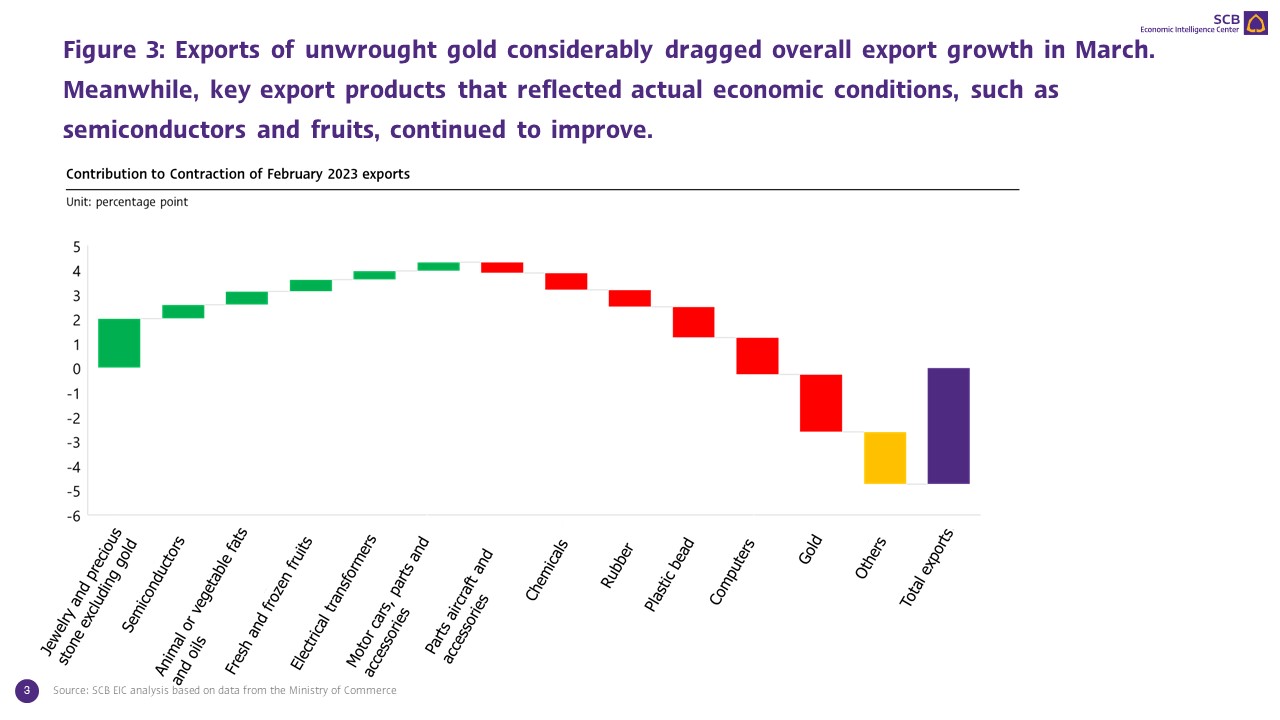

In February, exports of major products started to show signs of improvement, in which (1) Exports of agricultural products returned to growth for the first time in 5 months at 1.5%. The key products driving growth were fresh/ frozen/ dried fruits, with 95.0% growth primarily from exports to China, a sizable market with robust growth after COVID-19 curbs eased, in addition to boosts from the low base in the prior year. Other key drivers included Chilled or frozen poultry cuts, with 61.6% growth, up from 50.0% from the prior month. (2) Exports of agro-industrial products also returned to growth for the first time in 3 months at 5.6%, after declining by -3.3% in January. The key products that boosted growth were exports of animal or vegetable fats and oils, which increased by 171.4%, improving from 124.0% in January. Similarly, exports of sugar returned to the first contraction in 3 months at 21.4%. (3) Exports of principle manufacturing products continued to contract for the fifth consecutive month at -6.2%, worsening from -5.4% in January. Such weakening growth was prompted by the slump in unwrought gold exports at -75.3%, compared to -14.8% in the prior month, as well as exports of plastic beads and chemicals product that continued to plummet for the eighth and tenth consecutive month, respectively. On the other hand, exports of other manufacturing products, including semi-conductors devices, transistors, and diodes, Electrical transformers and parts thereof, and motor cars, parts and accessories, continued to improve; and (4) Exports of mining and fuel products dropped by -10.0%, after increasing by 6.8% in the prior month, as exports of refined fuels decreased by -3.7% compared to 16.2% in January.

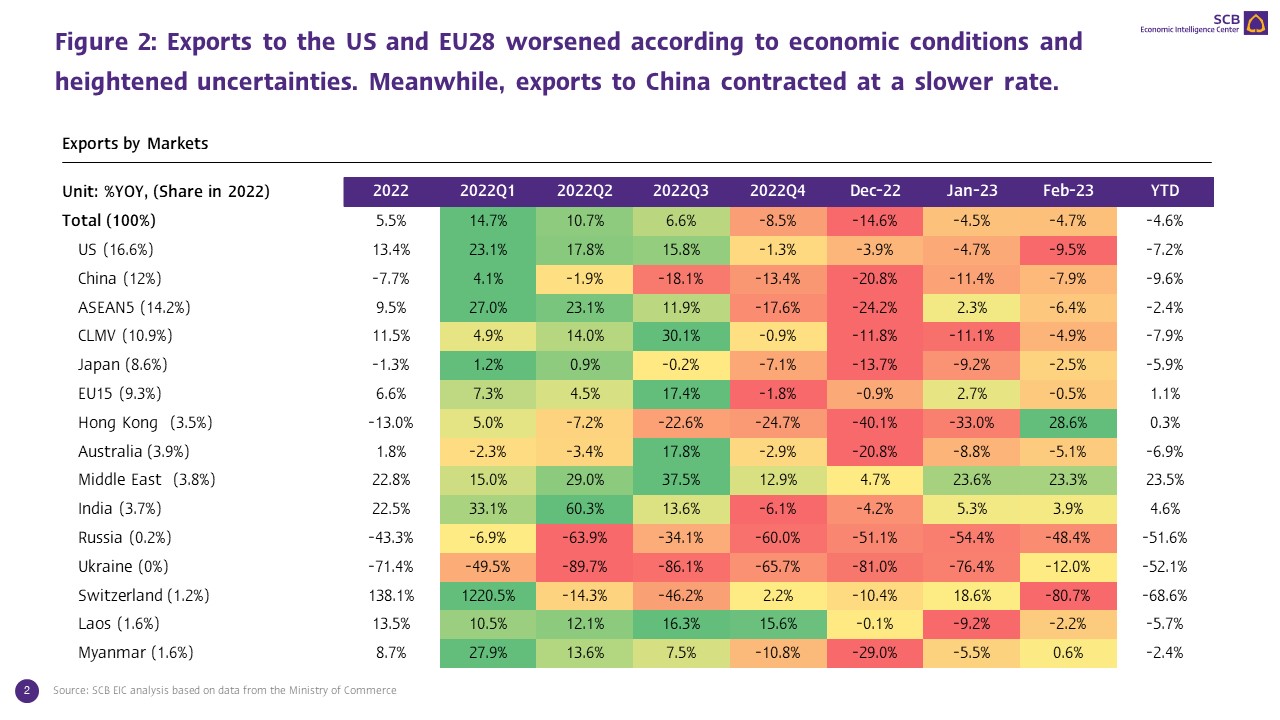

Exports to the US and EU28 worsened according to economic conditions and heightened uncertainties. Meanwhile, exports to China contracted at a slower rate.

In the big picture, exports to different markets saw uneven growth in February. Exports to the western markets declined following economic conditions as well as heightened uncertainties. Meanwhile, exports to China and new potential markets for Thai exports improved, in which (1) Exports to the US contracted by -9.5% compared to -4.7% in the prior month. Such a performance marked a 33 months low following weakening US economic conditions, which should further worsen this year. (2) Exports to EU28 reverted to a -0.5% contraction after increasing by 2.7% in the prior month. The decline was led by exports to Switzerland that tumbled by -80.7% after surging by 138.1% in 2022 as exports of Precious stones and jewellery plummeted. (3) Exports to China started to recover despite posting declining growth at -7.9% as the dropped drastically improved from -20.8% in the prior month. Furthermore, such a performance was the smallest contraction in the past 8 months, suggesting the resumption of Chinese demand after the reopening. Furthermore, exports to Hong Kong also returned to the first expansion in 10 months at 28.6%. (4) Exports to CLMV continued to decline for the fifth consecutive month at -4.9%, though stalling from -11.1% in the previous month; and (5) Exports to the Middle East continued to surge by 23.3%, despite slightly stalling from 23.6% in January. Exports to Saudi Arabia led the growth, with an expansion of 56.2%, making Saudi Arabia the market with the highest export growth in February.

Thai trade deficit continued to widen for the eleventh consecutive month, while import growth stalled.

The value of imports in February stood at USD 23,489.7 million, increasing by 1.1%, or slowing compared to the 5.5% growth in the prior month. However, excluding gold (a product that does not reflect actual international trade conditions), imports improved by 3.4%, reflecting that import demand still remains and should improve following the recovery of Thai economic conditions. On the contrary, exports continued to stall following the global economic slowdown. As such, the customs basis trade balance registered at a deficit of USD -1,113.4 million in February. Such a posted result marked 11 consecutive months of deficit.

SCB EIC anticipates worrisome merchandise export conditions in H1/2023, though recovery should resume in H2/2023.

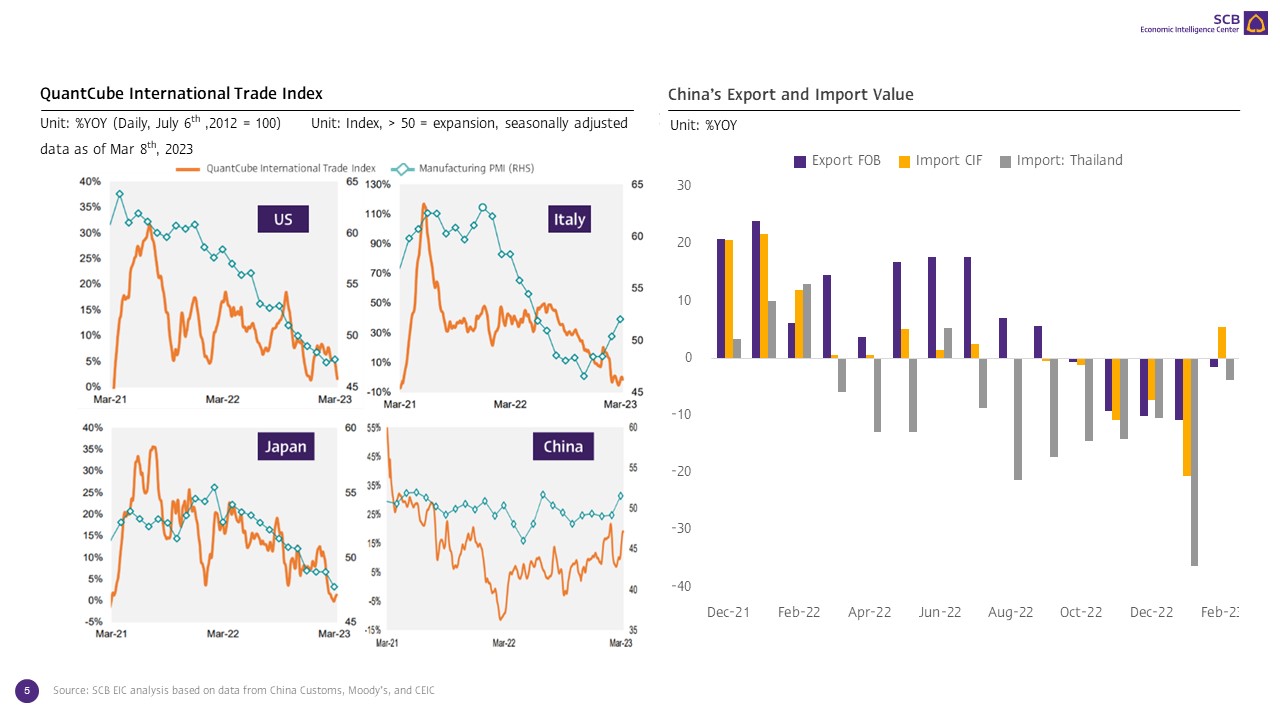

Thai merchandise exports should continue to decline in H1/2023 (Figure 1), following (1) The Flash Manufacturing PMI1 of key economies weakening considerably in March triggered by slowing manufacturing activities in the Eurozone and the UK that shrank to 4 months and 2 months low, respectively. On the other hand, although the reading of the US Manufacturing PMI improved to 49.3 this month from 47.3 in February, such an improvement was partly driven by easing supply bottlenecks. Furthermore, the New export order index continued to contract for the 10th consecutive month. (2) South Korea’s export performance during the first 20 days in March dropped by -17.4%, worsening from -2.8% in the prior month, indicating weakening merchandise demand throughout Q1/2023. (3) The QuantCube International Trade Index in March indicated that the global trade outlook remained bleak, with trade conditions of major economies, such as the US, Japan, and Italy weakening since late 2022 with no signs of recovery; and (4) The high base with implications on growth until mid-2023; the figure in March, in particular, had a record-high base. Moreover, other notable risks undermining Thai merchandise exports warrant monitoring, including stringent liquidity positions in financial institutions in the US and Europe that may trigger a global economic recession and the wealth effect declining from high financial market volatilities. Such factors should undermine merchandise import demand accordingly.

Nevertheless, Thai exports in H2/2023 should see boosts from China’s private consumption recovery after the cancellation of Zero-COVID measures, with a more pronounced impact on import demand in H2/2023. China’s economic indicators suggested recovery, despite such readings somewhat stalling in early 2023 due to the Chinese New Year. Furthermore, global economic conditions passed the trough, with reported growth exceeding the forecasted rate in late 2022. As such, SCB EIC maintains Thailand’s 2023 export forecast at 1.2%.

1Early estimates of the PMI index is based on approximately 85% to 90% of total PMI survey responses each month.