The MPC raised its policy rate 0.25% to 1.75% as expected. In the baseline scenario, SCB EIC expects policy rate to continue rising to 2% in the middle of this year.

SCB EIC assesses that the Thai economy in 2023 will likely expand more than expected driven by tourism and private consumption

The MPC voted unanimously to raise the policy rate 0.25% from 1.5% to 1.75%.

The Thai economy should continue to expand, driven mainly by tourism and private consumption. Exports of goods are recovering and expected to gain strength in the second half of this year. However, the global economic uncertainty has increased, in part from persistent inflationary pressures and episodes of banking stresses in advanced economies. Headline inflation would likely return to the target range in the middle of the year, but core inflation remains elevated with upside risks from higher cost pass-through and demand pressures. A continuation of gradual policy normalization is thus appropriate in light of the growth and inflation outlook.

The MPC projects the Thai economy to continue expanding at 3.6% and 3.8% in 2023 and 2024.

The Thai economy should continue growing on the back of foreign tourists that have been increasing in almost all nationalities. This should promote employment and labor income, in turn sustaining private consumption. Meanwhile, merchandise exports in the first quarter show signs of rebounding after contracting the previous period, and should gather momentum in the second half of this year.

The MPC expects headlind inflation to be 2.9% and 2.4% in 2023 and 2024.

Headline inflation would likely return to the target range by mid-2023 thanks to easing supply-side pressures notably from electricity and oil prices. Meanwhile, core inflation is projected to decline from 2022 to 2.4% in 2023 before gradually falling to 2% in 2024. However, persistently high inflation remains a risk, as producers could pass on higher costs absorbed in the past and demand-side pressures could pick up as the recovery gains traction. The Committee will continue to closely monitor price developments.

The MPC assesses that the overall financial system remains resilient. Recent banking stresses in some advanced economies have not had a significant impact on the Thai financial system,

as Thai financial institutions and corporations have limited linkages with the troubled banks and risky assets. Moreover, financial institutions maintain high levels of capital and loan loss provision. As for households and businesses, the ongoing economic recovery has improved debt serviceability. Financial fragilities nonetheless remain for some SMEs and certain households exposed to rising living costs and higher debt burden. The Committee agrees that financial institutions should continue to press ahead with debt restructuring and deems it important to have in place targeted measures and sustainable debt resolution for vulnerable groups. Overall financial conditions remain accommodative, tightening somewhat from higher private sector funding costs consistent with the policy interest rate. On balance, financial conditions are supportive of the ongoing recovery and mobilization of funds by the private sector. The baht continues to fluctuate against the US dollar, driven by the Federal Reserve’s uncertain policy outlook and financial market volatility induced by banking stresses in advanced economies.

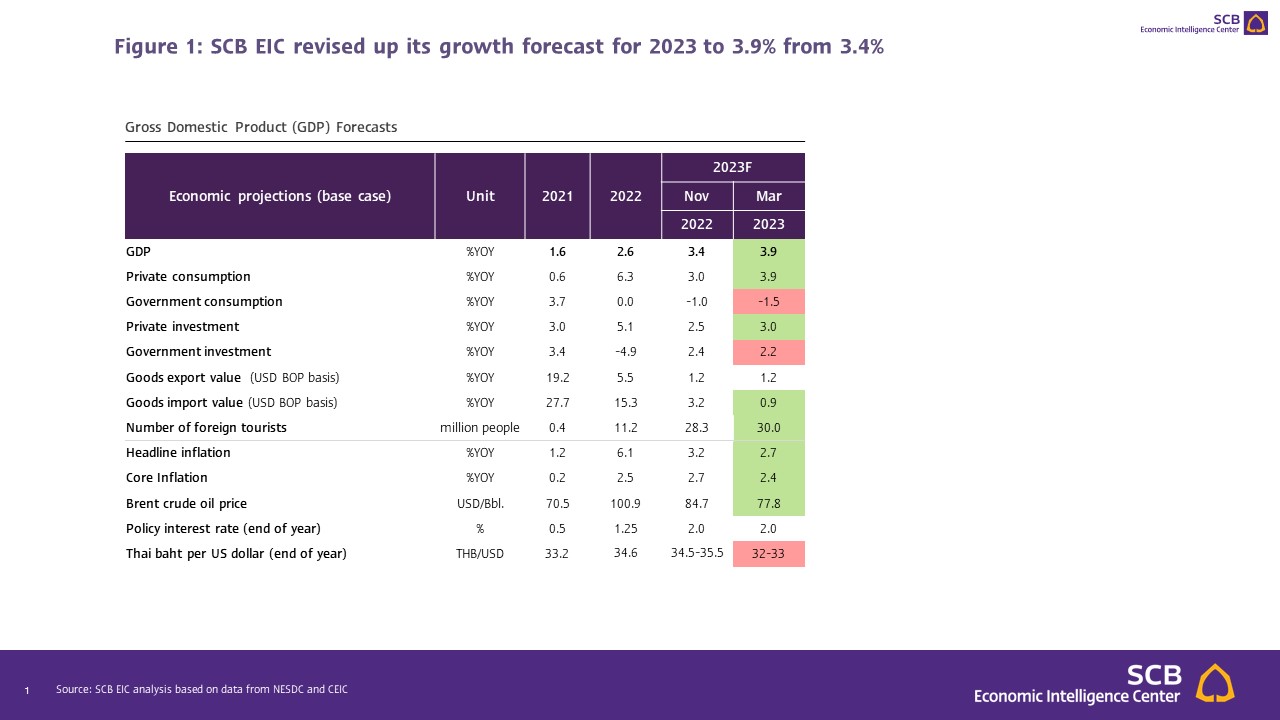

SCB EIC assesses that the Thai economy in 2023 will likely expand more than expected

driven by tourism and private consumption as the Chinese economy recovers faster and stronger than expected. SCB EIC has revised up its growth forecast this year to 3.9% from 3.4% (figure 1) and the forecast of foreign tourists in 2023 from 28 to 30 million. This will support the labor market and private consumption to continue recovering. Moreover, domestic demand has improved in line with business and consumer confidence. Labor market has also recovered with many indicators returning to near pre-COVID levels. Although there remains some fragilities in the labor market, these will likely improve in line with the economic recovery and employment in the tourism sector.

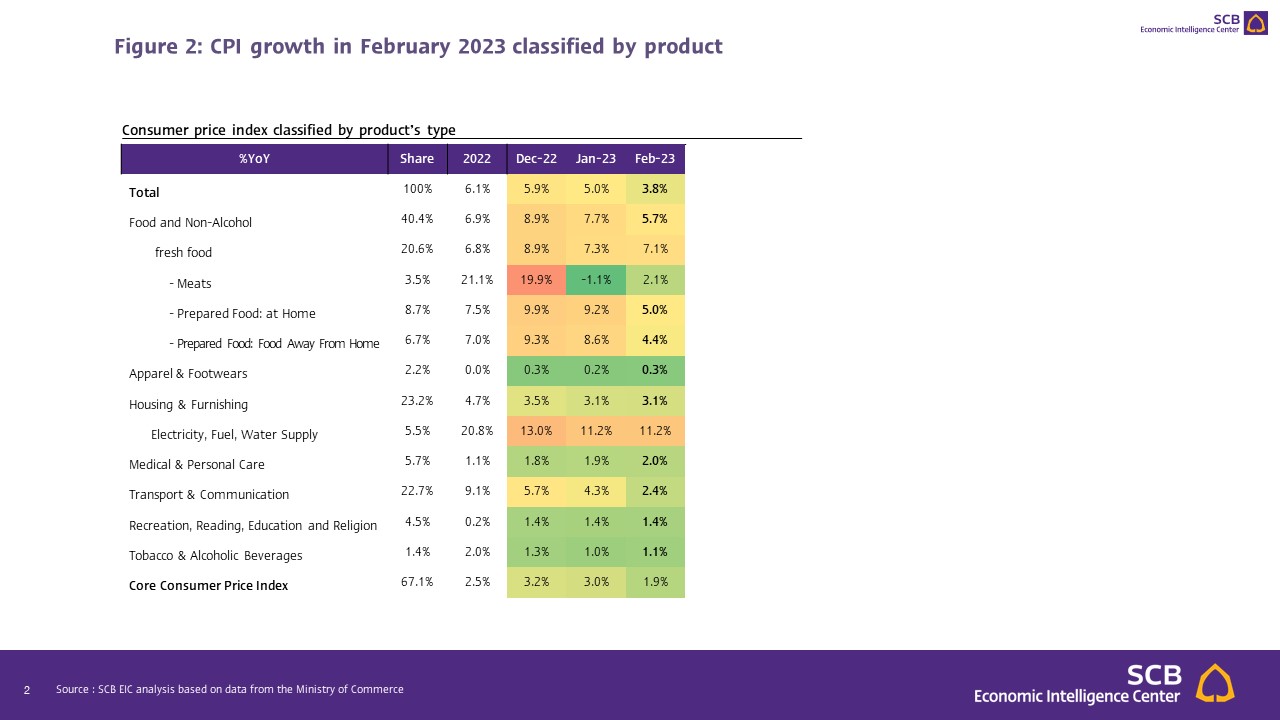

Headline inflation in 2023 is expected to moderate and will return to the BOT’s target range of 1-3% this year.

SCB EIC expects headline inflation to fall to 2.7% due to a decline in global energy prices and continuing domestic energy subsidies. Meanwhile, core inflation will likely fall to 2.4% this year. Looking ahead, core inflation may not decline fast given the gradual cost passthrough and demand pressures in line with the economic recovery.