Thai exports continued to shrink for the fourth consecutive month. Despite a bleak outlook, China’s reopening should support growth in the periods ahead.

Thai merchandise exports may continue to decline. However, China’s reopening should support growth to some extent.

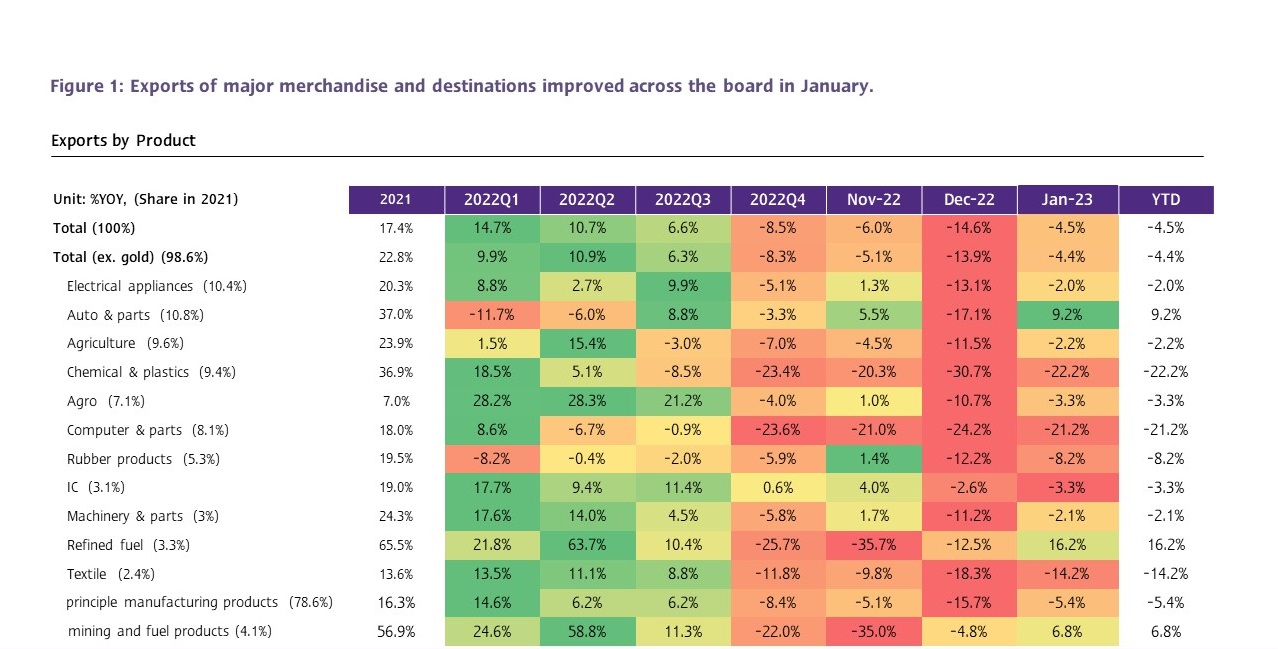

Thai merchandise exports weakened in January, marking a fourth consecutive month decline.

The value of Thai exports in January 2023 was at USD 20,249.5 million, falling by -4.5%YOY. Despite declining for 4 consecutive months, exports in January decline at a slower pace from -14.6%YOY in December, in part because of the low base. In terms of the seasonally adjusted month-on-month growth, exports in January shrank by -3.0%MOM_sa. Nevertheless, excluding gold (a product that does not reflect actual international trade conditions), Thai exports during the month dropped by -4.4%YOY compared to -13.9%YOY in December.

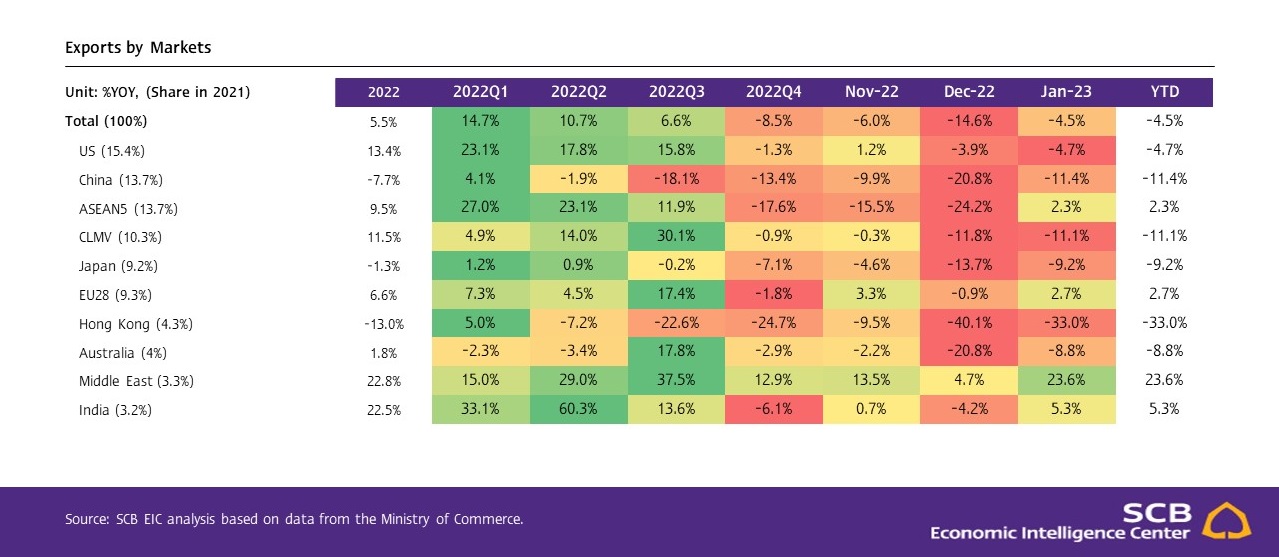

Exports of all major products dropped by a slower rate. While exports of mineral and fuel products expanded for the first time in 6 months.

Exports of major products weakened by a slower rate in January, in which (1) Exports of agricultural products improved to -2.2%YOY from -11.5% in December. The key products including rubber, tapioca products, and prepared poultry continued to shrink. On the other hand, exports of rice soared by 72.3%, backed by the low base and India’s rice export curbs that increased the price of rice on the global market as well as heightened the demand for Thai rice. Furthermore, exports of chilled or frozen poultry cuts continued to expand for the eighth consecutive month. (2) Exports of agro-industrial products stalled to -3.3% after dropping by -10.7% in December. Nevertheless, the key products such as prepared or preserved fruits, prepared or preserved seafood, and sugar continued to shrink, while exports of animal or vegetable fats and oils grew drastically by 124%. (3) Exports of manufacturing products fell by a slower rate to -5.4%, from -15.7% in December. The key products that boosted growth were plastic beads, chemical products, and rubber products. Meanwhile, exports of motor cars, parts and accessories continued to improve as the gradually recovering chip supply heightened the production of cars for exports; and (4) Exports of mining and fuel products expanded 6.8% after dropping by -4.8% in the prior month supported by refined fuels exports that expanded for the first time in 6 months.

Exports to nearly all key markets fell by a slower rate. Meanwhile, exports to the Middle East continued to improve, and exports to ASEAN5 reverted to an expansion.

In the big picture, exports to nearly all key markets fell by a slower rate in January, with some markets reverting to an expansion. Such conditions reflected brighter global demand outlooks amidst prolonged weakening sentiment, in which (1) Exports to China fell by -11.4%, improving from -20.8% in the previous month. (2) Exports to the US dropped by -4.7% compared to -3.9% in the prior month. Such a condition was in line with worsening US economic signals this year. (3) Exports to EU28 reverted to a 2.7% growth after falling by -0.9% in the previous month as risks of entering an economic recession waned; and (4) Exports to CLMV continued to drop for the 3rd consecutive month at -11.1% after expanding for as long as 14 consecutive months. Such a growth slightly improved from -11.8% in the previous month. Meanwhile, exports to ASEAN5 returned to a 2.3% growth after tumbling for 3 consecutive months. Moreover, as the market with the highest growth in January, exports to the Middle East accelerated to 23.6% from 4.7% in December.

Thai trade deficit continued to widen for the tenth consecutive month, while imports returned to an expansion.

The value of imports in January stood at USD 24,899.1 million, returning to an expansion of 5.5% after shrinking for the first time in Q4/2022. Imports of nearly all major merchandise expaned, except imports of capital goods and raw materials and intermediate raw materials, which continued to weaken by -10.3% and -7.4%, respectively. Meanwhile, imports of fuel products improved considerably by 84.4% (contracted by -13.2% in the prior month). Such a growth was supported by soaring crude oil imports, with growth at 132.0% (contracted by -16.6% in the prior month). Furthermore, imports of motor cars, motor vehicles, parts and accessories returned to growth at 28.4%, a drastic improvement from the contraction witnessed throughout 2022. Nevertheless, Thai imports grew following the Thai economic recovery pace, while exports continued to stall following the global economic slowdown. As such, the customs basis trade balance registered at a deficit of USD -4,649.6 million in January. Such a posted result marked 10 consecutive months of deficit.

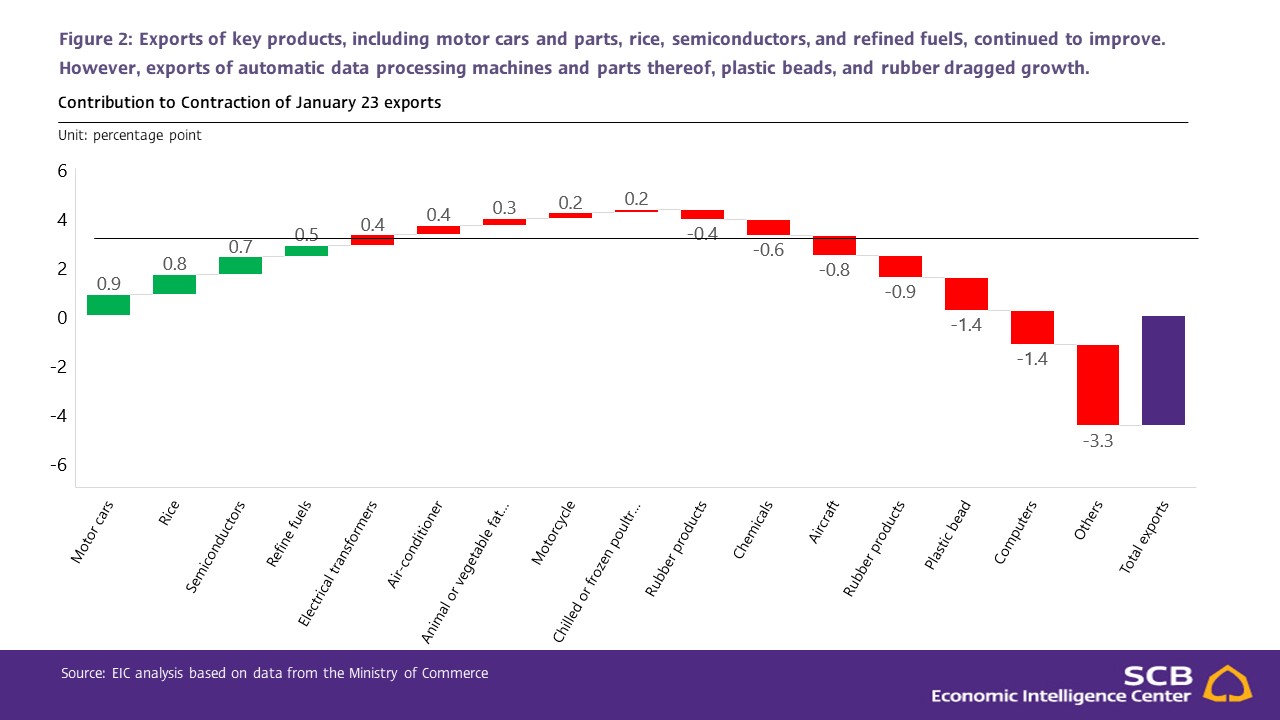

Thai merchandise exports could continue to worsen. However, support from China’s reopening should somewhat support growth with a more pronounced impact in H2/2023.

Going forward, Thai exports could continue to weaken as global economic and trade conditions slowed considerably. However, further contractions should not be as severe as previously anticipated, which should somewhat urge gradual export recovery, in which (1) The Global Manufacturing PMI index stood at 50.0 in February. Despite the reading improving to indicate no change for the first time after signaling contraction for as long as 6 months, most of the improvement was due to alleviating supply bottlenecks. Notable backing included the Manufacturing Production Index reading that edged up for the first time since July 2022 to 50.8 coupled with slower demand sector recovery as demonstrated by the New Order and New Export Order Index that improved though still signaling contraction at 49.3 and 48.3, respectively. (2) South Korea’s export performance in February continued to drop by -7.5%. Despite the figure improving from -16.6% in the previous month, the improvement was partly short-lived following the seasonal effects of the Chinese New Year. Excluding the event, exports in February should continue to plummet; and (3) The QuantCube International Trade Index indicated that the global trade outlook remained bleak, with trade conditions of major economies, such as the US, Japan, and the UK weakening during late 2022 with no clear signs of recovery.

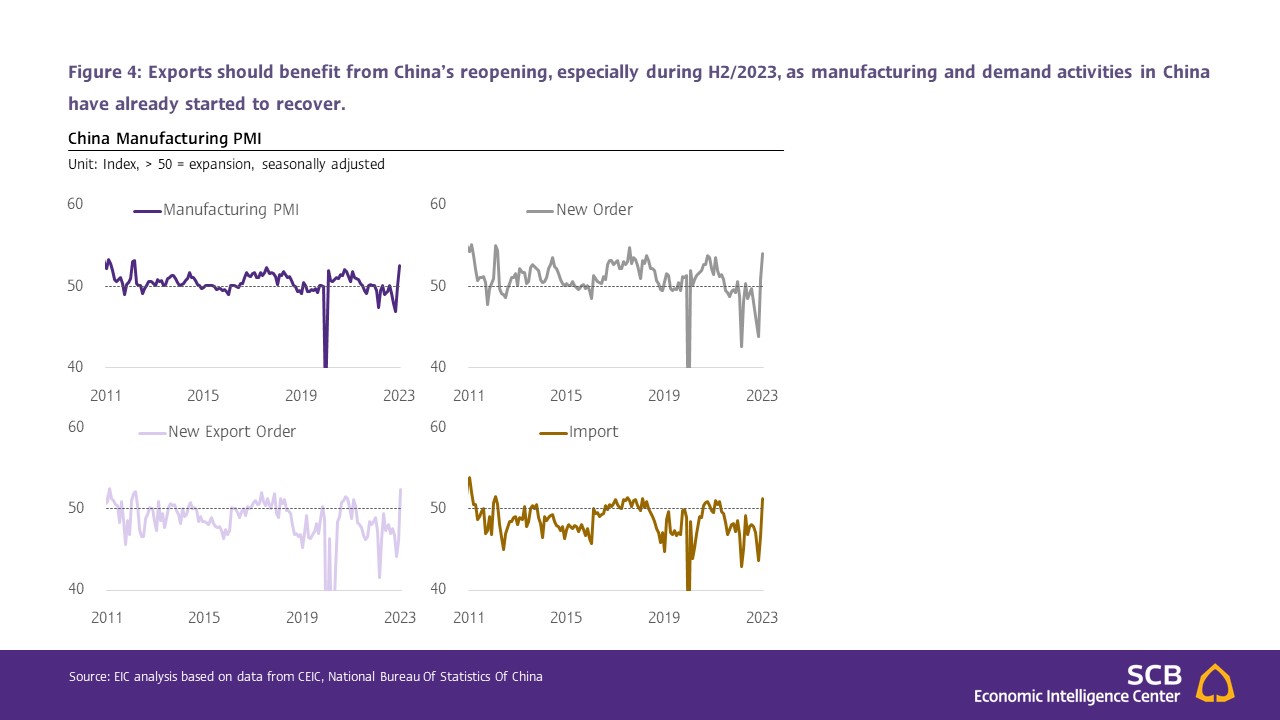

Nevertheless, Thai exports in 2023 should benefit from China’s Zero-COVID policy termination, which will prompt private consumption recovery, thus increasing demand for imports, especially during H2/2023. China’s international trade indicators have already witnessed recovery, though with some slowdowns during early 2023 due to the long Chinese New Year holiday. Similarly, the manufacturing sector started to recover as China’s Manufacturing PMI reading in February improved to 52.6, the highest rate since April 2012. Other indicators that signaled a recovery in Chinese demand included the New Orders Index, New Export Orders Index, and China’s imports that expanded for the first time in over 6 months.

Although Thai exports may be undermined by the aforementioned factors, SCB EIC evaluates that Thai exports should benefit from these 3 potential markets, namely the Middle East with boosts from recovering Thai – Saudi Arabia ties and higher expected economic growth compared to the global market, CLMV with support from the Thai government in the forms of accelerating exports through border trade as well as higher expected economic growth compared to the global market, and Latin America, a new potential export market the Ministry of Commerce is eyeing. Latin America is a small market with great growth prospects despite the distance limitations

SCB EIC is currently assessing export conditions; and the update of export along with other economic forecasts will be released in mid-March.