Thai exports plummeted at the end of the Tiger year, whilst still achieving 5.5% growth overall. Going forward, exports may benefit from China’s reopening.

SCB EIC views that Thai merchandise exports going forward should see support from China’s ZERO-COVID policy termination.

Thai merchandise exports in December continued to plummet for the third consecutive month.

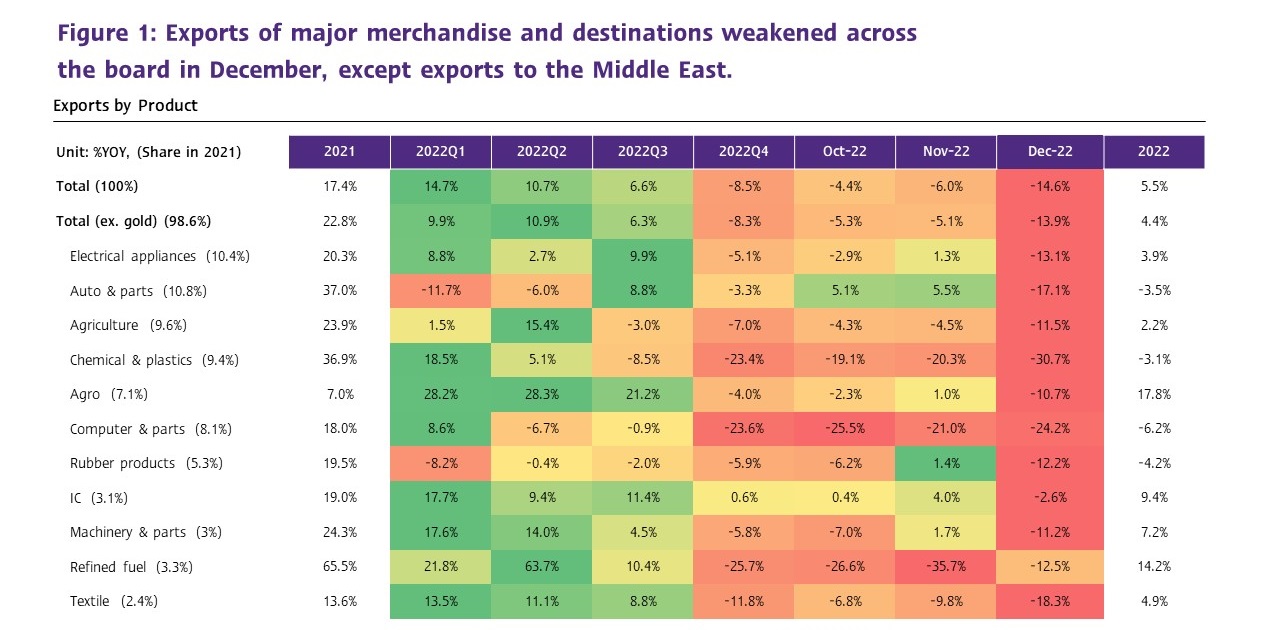

The value of Thai exports in December 2022 was at USD 21,718.8 million, falling sharply by -14.6%YOY (compared to the same period in the prior year). Such a decline persisted after weakening by -6% in November, partly due to the high base. Furthermore, the contraction marked a 3 consecutive months drop after expanding continually for as long as 20 months. In terms of the seasonally adjusted month-on-month growth, exports in December shrank by -2.1%MOM_sa, but still the softest contraction during the second half of 2022. Nevertheless, excluding gold (a product that does not reflect actual international trade conditions), Thai exports during the month weakened by -13.9%YOY. Despite such conditions, the value of Thai exports in 2022 stood at USD 287,067.9 million, marking a 5.5%YOY growth, thanks to support from buyers around the globe sourcing backup food reserves, slowing freight, and the gradually increasing numbers of shipping containers.

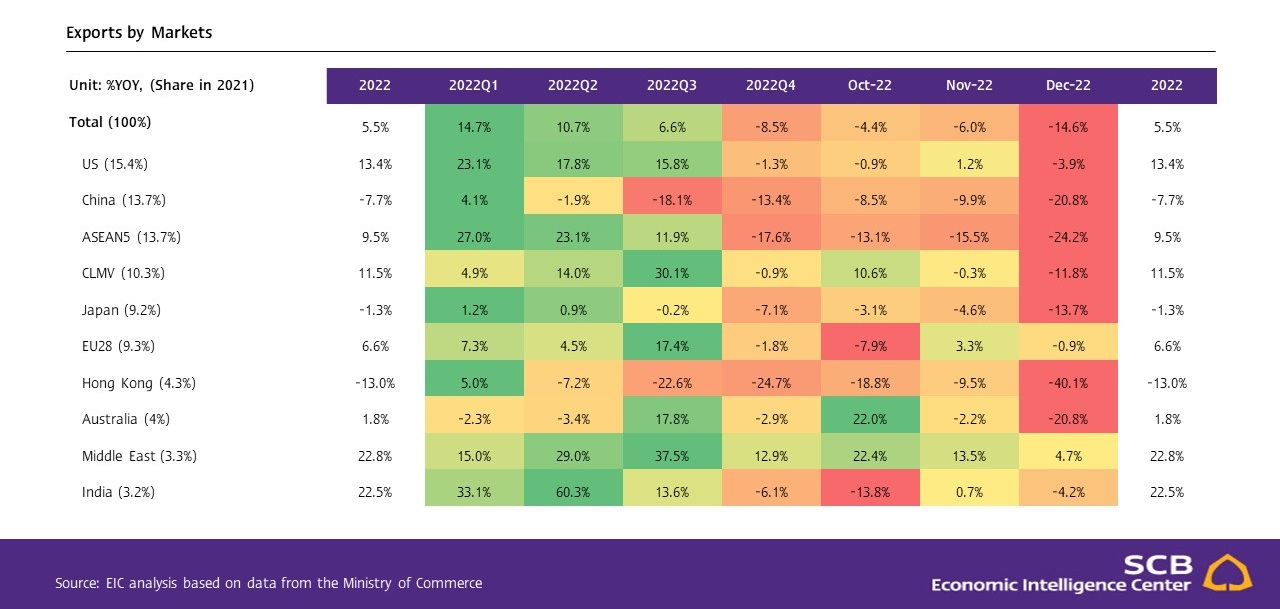

Exports of major products fell across the board.

Exports of all key products weakened in December, in which (1) Exports of agricultural products plummeted to -11.5% compared to contracting by -4.5% in November. Exports of rubber, cassava products, processed chicken, and rice shrank considerably, while exports of chilled or frozen poultry cuts and Fresh and frozen fruits continued to expand. (2) Exports of agro-industrial products reverted to a contraction of -10.7%, after slightly improving by 1% in November and used to be a product group that continued to expand well for 20 months. The key products that undermined growth included sugar, canned fruits, and prepared or preserved fruits, while animal or vegetable fats and oils somewhat expanded. (3) Exports of industrial products dropped by -15.7%, worsening from -5.1%

in November. The key products that weighed down growth were motor cars, parts and accessories, automatic data processing machines and accessories, chemical products, polymers of ethylene, propylene, etc in primary forms, rubber products, parts aircraft and accessories thereof, and iron and steel and their products. Meanwhile, exports of Semi-conductor devices, transistors and diodes, electrical transformers and parts thereof, and motorcycles, and parts and accessories continued to grow; and (4) Exports of mineral and fuel products fell by -4.8%, drastically improving from -35% in the previous month following continually growing crude oil exports despite at a slower rate.

Exports to China continued to fall for the 7th consecutive month. Also, exports to the US returned to a contraction following increasing recession risks.

Overall, exports by key destinations in December continued to shrink across the board, reflecting an accelerated decline in global demand, in which (1) Exports to China continued to drop for 7 consecutive months with a fall of -20.8% in December compared to -9.9% in the previous month. (2) Exports to the US reverted to a contraction of -3.9% after expanding by 1.2% in the prior month. Such a worsening condition was in line with drastically worsening US economic activities. (3) Exports to EU28 fell by -0.9% after expanding by 3.3% in the previous month as economic conditions slowed following to the energy crisis; and (4) Exports to CLMV considerably weakened for the 2nd month within 15 month with a contraction of -11.8% in December. Meanwhile, exports to ASEAN5 worsened to -24.2% compared to -15.5% in November. On the other hand, exports to the Middle East continued to improve by 4.7%, despite considerably slowing from the 22.4% and 13.5% expansion in October and November, respectively. Nevertheless, the destination was the only key market Thai exports saw 11 consecutive months growth.

Thai trade deficit continued to widen.

The value of imports in December stood at USD 22,752.7 million, returning to a contraction of -11.9% compared to an expansion of 5.6% in November. Imports of major merchandise fell across the board, especially imports of raw and intermediate raw materials, which saw the sharpest decline at -17.1% in comparison to -1.7% in the previous month. Similarly, imports of fuel products dropped by -13.2% as energy prices slowed. Nevertheless, Thai imports stalled at a considerably slower rate compared to exports following the Thai economic recovery pace and a broadened global economic slowdown, causing the customs basis trade balance to register at a deficit of USD -1,033.9 million in December. Such a posted result marked 9 consecutive months of deficit. As such, imports grew by 13.6%, while the trade deficit stood at USD -16,122.8 million in 2022.

Thai merchandise exports should see benefits from China’s ZERO-COVID policy termination in the periods ahead. However, the global economic slowdown and new import tax mechanisms by key trading partners may limit growth.

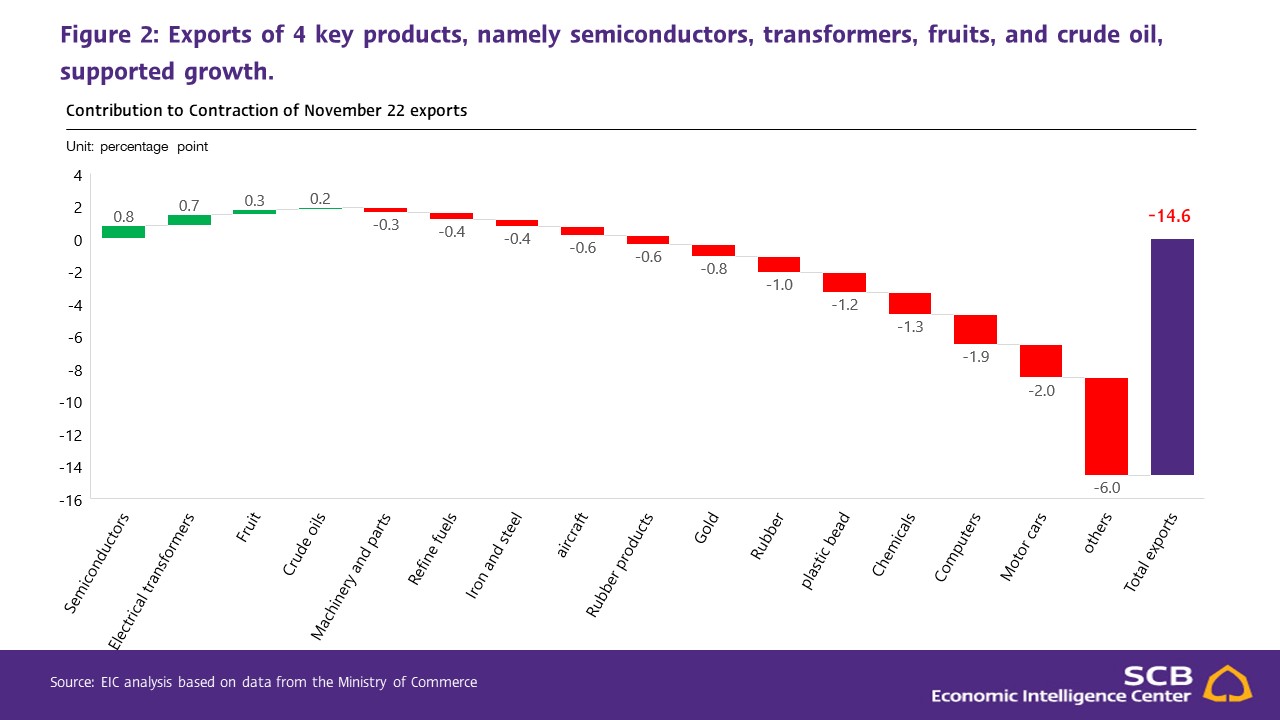

Despite worrisome Thai export outlooks following weakening global economic conditions, better-than-expected signals are beginning to emerge, including

(1) The Global Manufacturing PMI index dropped to 48.6 in December and was the most severe contraction in 30 months as the number of new orders gradually declined. This reflects the declining demand for manufacturing products going forward. Meanwhile, manufacturing output PMI, although still in a contraction area but the pace in December stalled in comparison to November as supply bottlenecks eased. A notable supporting indicator included the supply delivery time index reading that despite the rate still being under 50 but continued to improve for 8 consecutive months.

(2) South Korea’s export performance during the first 20 days in January weakened by -2.7%. Despite the figure falling for 5th consecutive months, the rate slowed compared to -8.8% in the previous month; and (3) Chinese exports considerably fell by -9.9% in December, marking the sharpest decline in 34 months. Moreover, such a drop slightly weakened from -8.9% in November. Meanwhile, Chinese imports improved to -7.5% in December from -10.6% in November. Similarly, Chinese imports from Thailand weakened by -10.5% in December edged up from -14.1% in November, but still, this was the 9th decline within the past 10 months. However, China’s Zero-COVID policy termination may prompt an increase in demand for products in the Chinese market in the periods ahead, though with limited short-term impact due to high uncertainties.Furthermore, China’s economic conditions and consumer demand have not yet fully recovered.

Despite improving signals, various risks warrant monitoring. Thai exports may see additional pressure from new import tax mechanisms by key trading partners. Some will commence in part from this year, starting from the EU’s imposition of 2 new environmental tax mechanisms, namely (1) Carbon Border Adjustment Mechanism (CBAM), which mandates importers to report carbon emissions figures on products imported into the EU expecting to be effective on October 1st, 2023, with a transitional period proposed until 2027, when taxes should then be levied. Key Thai exports to Europe that CBAM encapsulates include steel, machinery, electronic integrated circuits, rubber products, and automatic data processing machines and parts thereof. Such mentioned products account for approximately 30.8% of total exports to Europe; and (2) Deforestation-free product legislation, approved by the EU and due to come into force in 2024, obligates importers to report deforestation-related information on products imported into the EU. Key Thai exports to Europe that the regulation encapsulates include palm oils, beef, woods, and rubber products. Meanwhile, India plans to increase customs duty on 35 items. Such key exports from Thailand to India could include plastic products and jewelry and precious stone, which account for approximately 21% of total exports to India. More details of the hike should be released by the Indian government on February 1st, 2023.

Overall, although demand in the global market may weaken following the global economic slowdown and high uncertainty conditions, supply bottlenecks should continue to ease. Furthermore, China’s reopening should somewhat nudge Thai merchandise exports amidst the negative ambiance experienced in recent months.