Thai exports continued to be worrisome in November following 2 consecutive months of sharp declines.

The value of Thai exports in November 2022 was at USD 22,308 million, contracting by -6%YOY (compared to the same period in the prior year).

Thai merchandise exports in November continued to drop significantly for 2 consecutive months.

The value of Thai exports in November 2022 was at USD 22,308 million, contracting by -6%YOY (compared to the same period in the prior year). This drop persisted after the contraction of -4.4% in October. Furthermore, the contraction marked a 2 consecutive months drop after expanding continually for as long as 20 months. In terms of the seasonally adjusted month-on-month growth, exports in November grew by 2.5%MOM_sa, recovering from the plunge of -8.5%MOM_sa in October. Nevertheless, excluding gold (a product that does not reflect actual international trade conditions), Thai exports contracted by -5.1%YOY. During the first 11 months of 2022, Thai exports grew by 7.6%.

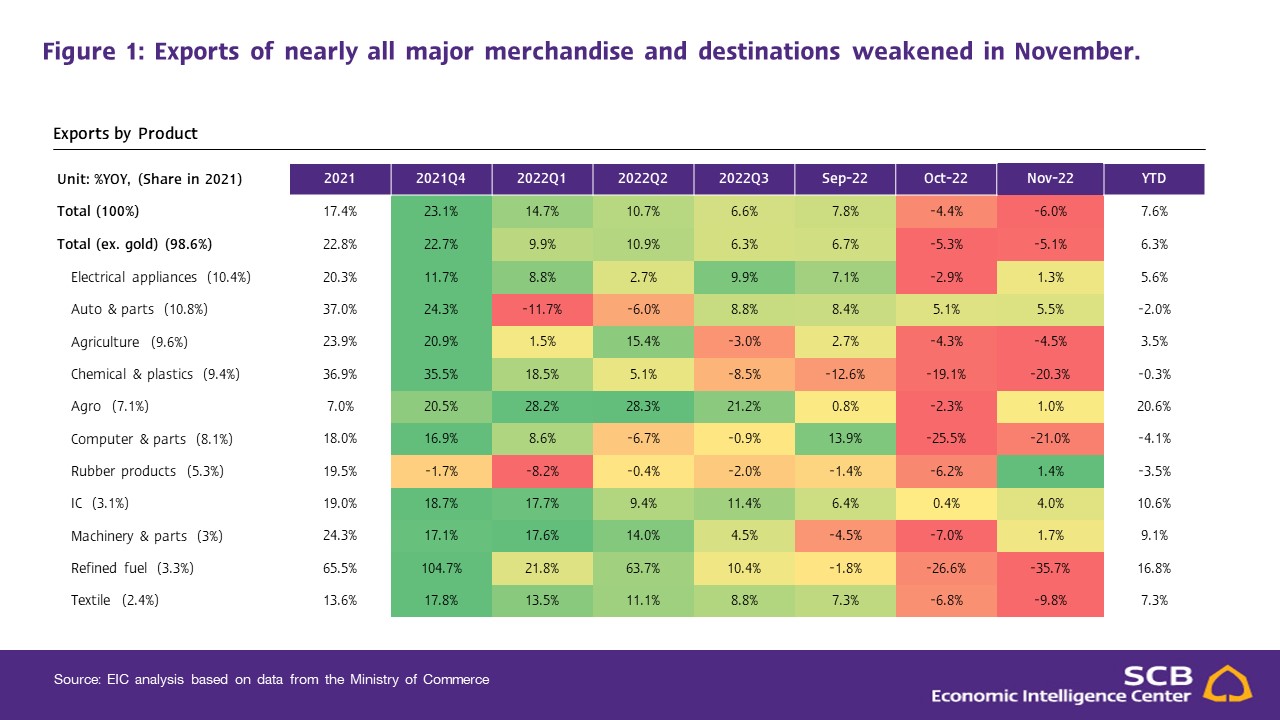

Exports of nearly all major products fell, except cars and parts.

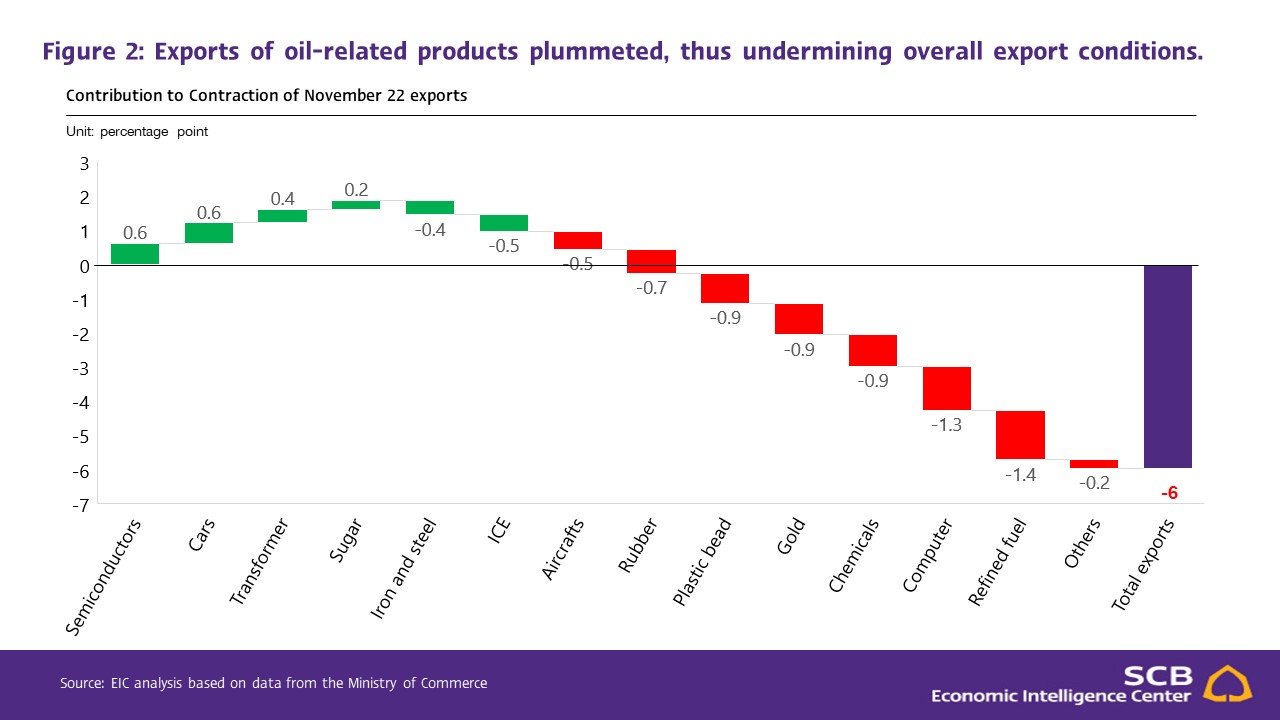

In the big picture, exports of nearly all major products weakened in November, in which (1) Exports of agricultural products dropped to -4.5% after contracting by -4.3% in October. Exports of rubber products shrank considerably following lower global demand during the COVID-19 crisis, while exports of processed chicken, fresh/ chilled/ frozen chicken, and fresh/ chilled/ frozen/ dried fruits continued to expand during the month, (2) Exports of agro-industrial products returned to a slight growth at 1% after falling by -2.3% in October. During the past 20 months, exports of agro-industrial products continued to improve. The key products driving growth were sugar, and wheat and other instant food products, (3) Exports of industrial products contracted by -5.1%, weakening from the -3.5% contraction in October. The key products that continued to support growth included cars and parts with growth at 5.5%, slightly increasing from the 5.1% expansion in the prior month, in addition to transformers and components, jewelry and precious stones (excluding gold), and motorcycles and parts. On the other hand, exports of computer and parts, chemicals, unwrought gold, plastic beads, aircraft, spacecraft, and parts, internal combustion engines and parts, and iron, steel, and products, undermined growth, and (4) Exports of mineral and fuel products continued to drop by -35% after falling by -23.9% in the previous month following stalling demand and product prices.

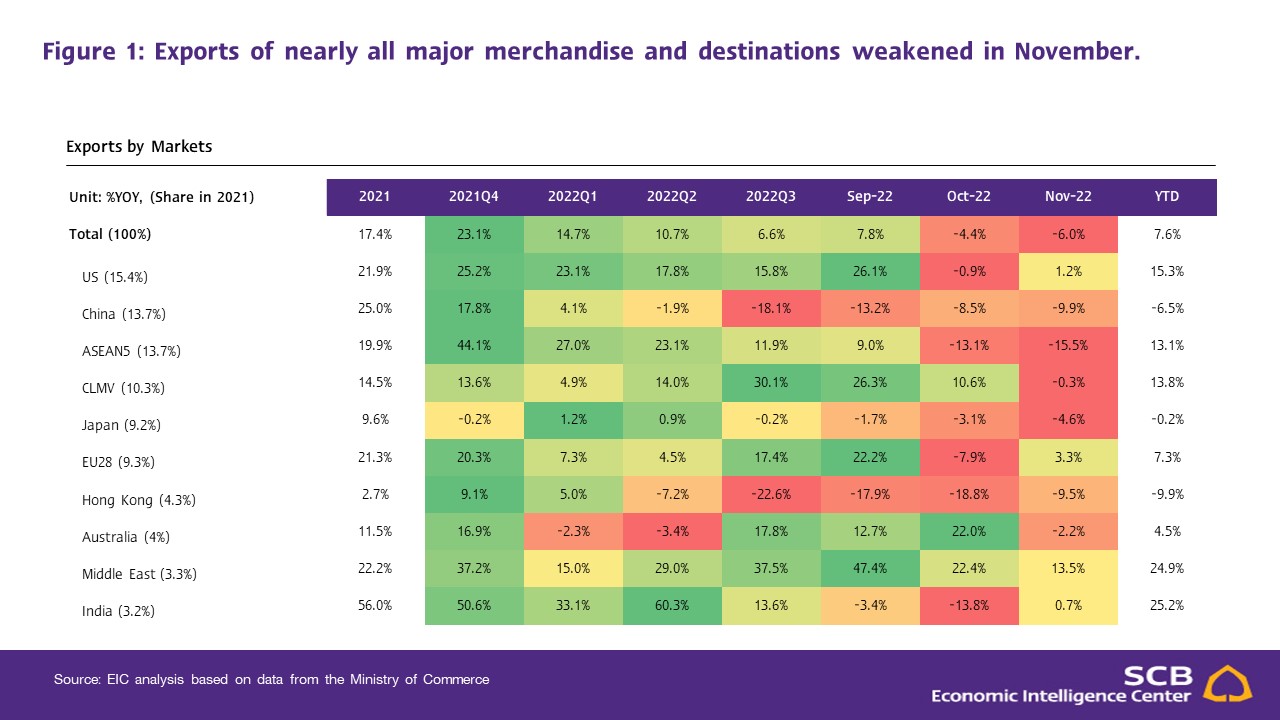

Exports to China continued to drop. Similarly, exports to CLMV contracted for the first time in 15 months.

Overall, exports by key destinations continued to shrink, reflecting an accelerated decline in global demand, in which (1) Exports to China continued to drop for 6 consecutive months with a contraction at -9.9% in November, (2) Exports to the US and EU28 returned to growth after contracting in October, although, growth rate of 1.2% and 3.3% was low compared to the first three quarters of 2022. Such a weak condition was in line with worsening economic signals and exacerbating economic uncertainties in both markets, and (3) Exports to CLMV, which used to be robust, saw the first contraction in 15 months at -0.3%, deaccelerating considerably from 10.6% in the previous month. Meanwhile, exports to ASEAN5 declined by -15.5%, worsening from the contraction at -13.1% in October. However, exports to the Middle East continued to improve. Most importantly, the destination was the only major market Thai exports saw 10 consecutive months growth.

Thai trade balance continued to deficit.

The value of imports in November stood at USD 23,650.3 million, returning to growth of 5.6% compared to the -2.3% contraction in October. Such a performance followed accelerated imports of fuel products with growth at 50.6%YOY compared to the prior month at only 7.5%. Furthermore, imports of weaponry and military supplies expanded by 2,027.6% due to the low base effect. Meanwhile, imports of capital goods, including scientific and medical instruments, aircraft and aviation tools, continued to improve. Evidently, Thai imports stalled at a considerably slower rate compared to exports following the Thai economic recovery pace and a broadened global economic slowdown, causing the custom basis trade balance to register at a deficit of USD -1,342.3 million in November. Such a posted result marked 8 consecutive months of deficit. As such, during the first 11 months of 2022, imports grew by 16.3%, while the trade deficit stood at USD -15,088.9 million.

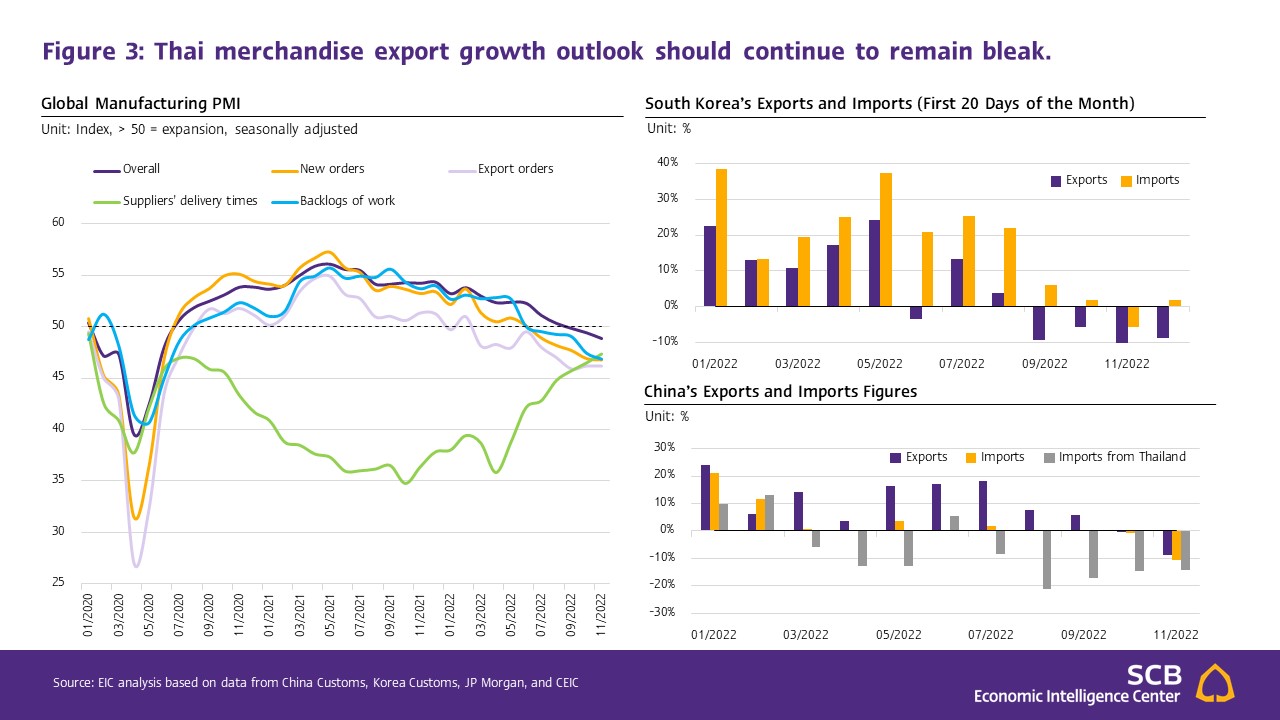

Thai merchandise export growth outlook should continue to remain bleak in line with global economic conditions. However, the Middle East market may be an opportunity for Thai exports.

Going forward, Thai export conditions should continue to remain worrisome as (1) The Global Manufacturing PMI reading dropped to 48.8 in November, marking the sharpest decline in the manufacturing sector in 29 months. Similarly, readings of PMI sub-indices, including new orders, exports orders, and backlog of work, worsened, reflecting significantly weakened demand for manufacturing products in the periods ahead due to global economic conditions. On the other hand, such weakening demand should somewhat ease supply shortage conditions evident from the continually improving supplier delivery time sub-index reading, though remaining under 50 level threshold, (2) South Korea’s export performance during the first 20 days in December continued to fall by -8.8% despite improving from -16.7% in the previous month, and (3) Chinese exports considerably fell by -8.9% in November, marking the sharpest decline in 33 months. Such a drop weakened drastically from the slight contraction in October. Also, Chinese imports shrank for 2 consecutive months with the sharpest drop since May 2020 at -10.6%. Furthermore, Chinese imports from Thailand fell by -14.1%, representing the 8th decline within the past 9 months. Nevertheless, China’s recent Zero-COVID easing may prompt an increase in demand for products in the Chinese market in the periods ahead, though with limited short-term impact due to high uncertainties. Furthermore, China’s economic conditions and consumer demand have not yet fully recovered. Such 3 mentioned conditions indicated a clear slowdown in global demand that should also weigh down demand for Thai exports.

However, amidst challenges in the periods ahead, the Middle East market may be an opportunity for Thai exports as export values to the market continued to increase throughout 2022. and has the potential to continuously grow. Some of the destinations with the highest potential include Saudi Arabia, the United Arab Emirates, and Qatar, while target products are food, automotive parts, building materials, and air conditioners.