Global economic frictions prompted Thai exports in October to face the most severe contraction in 2 years. A clouded recovery anticipated in 2023.

EIC views In 2023, Thai exports may expand by 1.2%.

Thai merchandise exports in October saw the first contraction in 20 months.

The value of Thai exports in October was at USD 21,772.4 million, contracting by -4.4%YOY (compared to the same period in the prior year). Such a performance drastically slowed from the 7.8%YOY expansion in the previous month. The weak performance during the month also represented the first contraction in 20 months, marking the most severe contraction in 2 years. In terms of the seasonally adjusted month-on-month growth, exports contracted by -8.5%MOM_sa after increasing by 6.9%MOM_sa in the previous month. Excluding gold (a product that does not reflect actual international trade conditions), exports tumbled by -12.5%MOM_sa from September. Despite such conditions, during the first 10 months of 2022, Thai exports enjoyed a 9.1% increase.

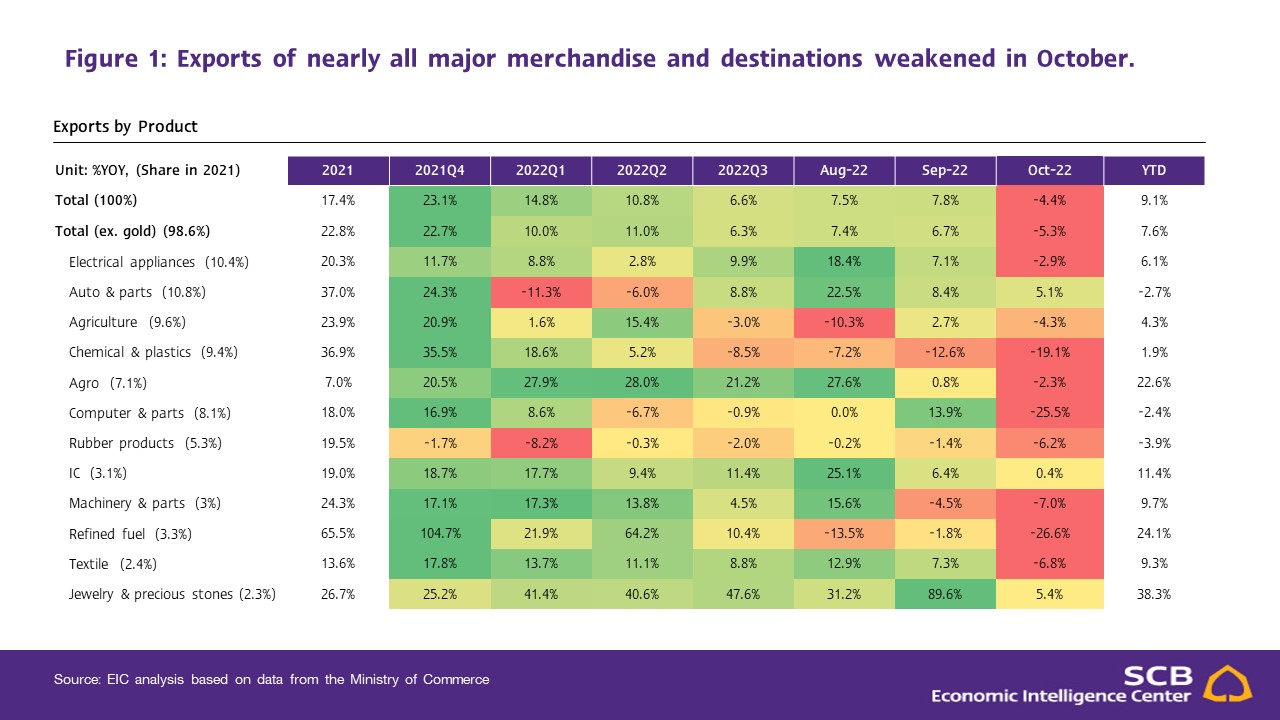

Exports of major products fell across the board, except automotive and parts.

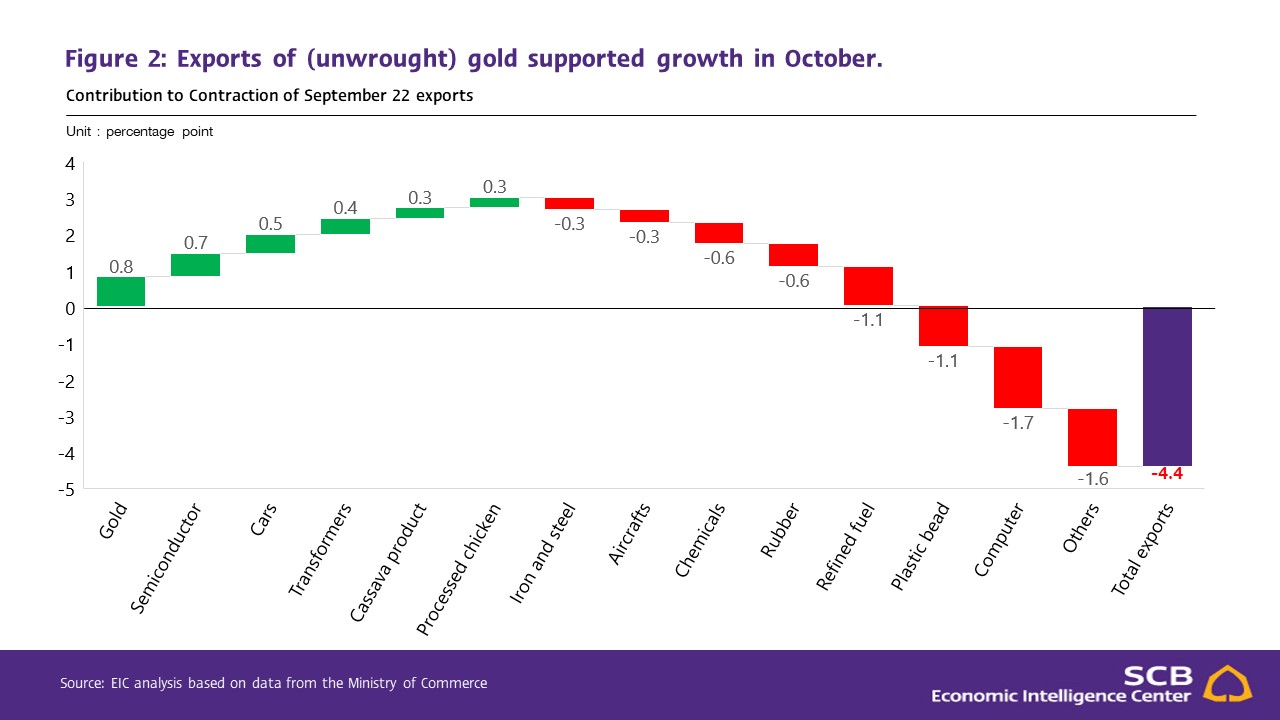

In the big picture, exports of nearly all major products weakened in October, in which (1) Exports of agricultural products dropped, once again, by -4.3% after returning to a 2.7% growth in September. Exports of rubber products shrank considerably, while exports of cassava products and chicken continued to expand. Also, exports of fruits considerably slowed growth, (2) Exports of agro-industrial products weakened by -2.3% after expanding for 20 consecutive months. Worsening agricultural and agro-industrial export conditions could be partly influenced by floods in agricultural areas that occurred from Q3/2022 to late October. However, the flooding incidents started to ease in late October. Thus, such conditions should have a low impact on Thai exports during the remainder of the year, (3) Exports of industrial products contracted by -3.5%, weakening from the 9.4% expansion in September. The key products supporting growth during the month included unwrought gold, semiconductor device, transistors, and diodes, motor cars, parts and accessories (especially motor cars), and transformers and components. Such better conditions partially urged by easing chip shortages. Meanwhile, exports of computer and parts, plastic beads, chemicals, aircraft, spacecraft, and parts, iron, steel and products, and rubber products plummeted, (4) Exports of mineral and fuel products tumbled by -23.9% after expanding by 1.2% in the previous month following stalling product prices, and (5) Exports of unwrought gold soared by as high as 56.9%YOY. Thus, making exports of unwrought gold one of the most important export drivers during the month (Figure 2).

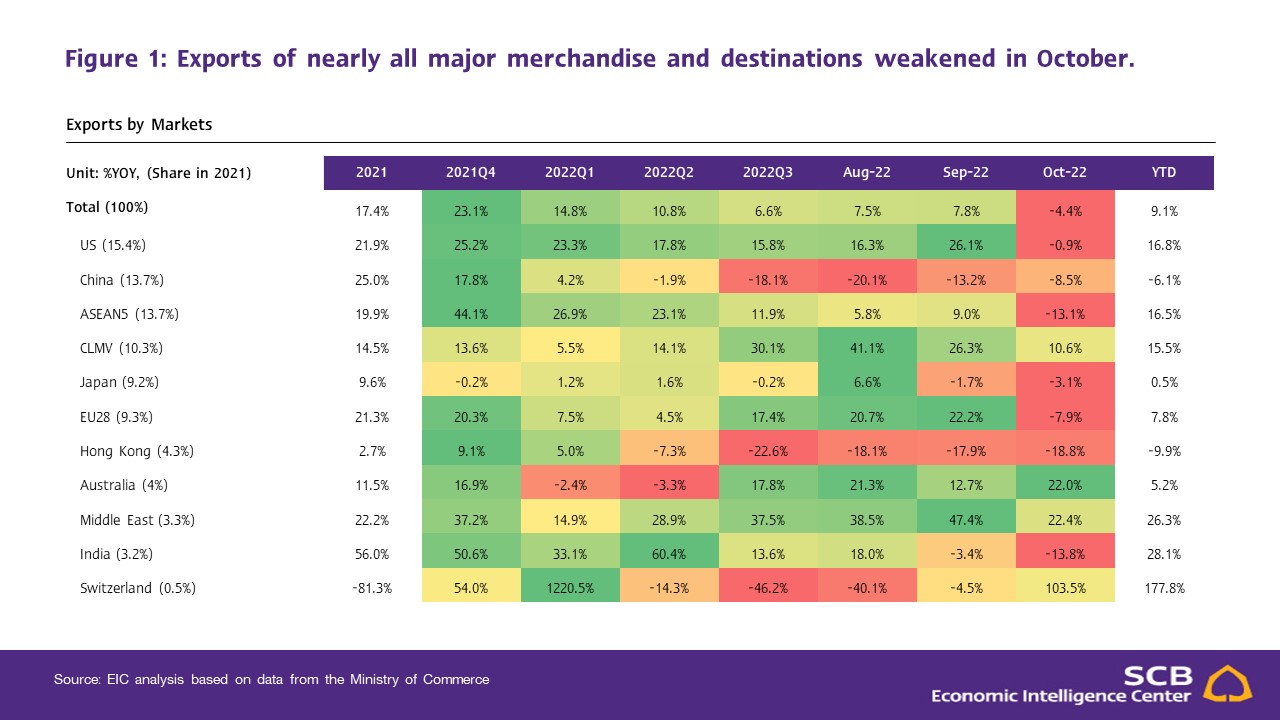

Exports to major destinations significantly contracted. However, exports to CLMV continued to be robust.

Analysis of exports by destinations revealed contractions in nearly all key markets, reflecting a sharp slowdown in global demand, in which (1) Exports to China continued to fall for 5 consecutive months with a -8.5% contraction during the month following the continual enforcement of the strict Zero COVID policy, (2) Exports to the US and EU28 contracted by -0.9% and -7.9% compared to 26.1% and 22.2% growth in the previous month, respectively. Such conditions were in line with the clearer signs of global economic slowdowns, as well as heightening economic uncertainties in the two mentioned markets, and (3) Exports to CLMV continued to expand by 10.6%. Meanwhile, exports to ASEAN5 fell by -13.1% after expansions in the prior periods. Further analysis of export figures found that exports to Switzerland surged by 103.5% as exports of gold increased by as high as 159.8%.

Thai trade deficit continued.

The value of imports in October stood at USD 22,368.8 million, dropping by -2.3%, the first contraction in 21 months. Such a contraction weakened from the surge of 15.6% in the previous month partly as import prices slowed. Imports of capital goods tumbled by -16.4%, while both imports of raw and intermediate raw materials and consumer goods slightly dropped by -0.4%. Despite imports of fuel expanding by 7.5%, the expansion weakened to a 19 months low. Meanwhile, imports of vehicles and transportation equipment, and weaponry continued to improve by 0.3% and 2,993% (due to the low-base effect), respectively. Nevertheless, Thai imports stalled at a considerably slower rate compared to exports, causing the custom basis trade balance to register at a deficit of USD -596.4 million in October. Such a posted result marked a 7 consecutive months of deficit. As such, during the first 10 months of 2022, imports grew by 18.3%, while the trade deficit widened to USD -15,581.3 million.

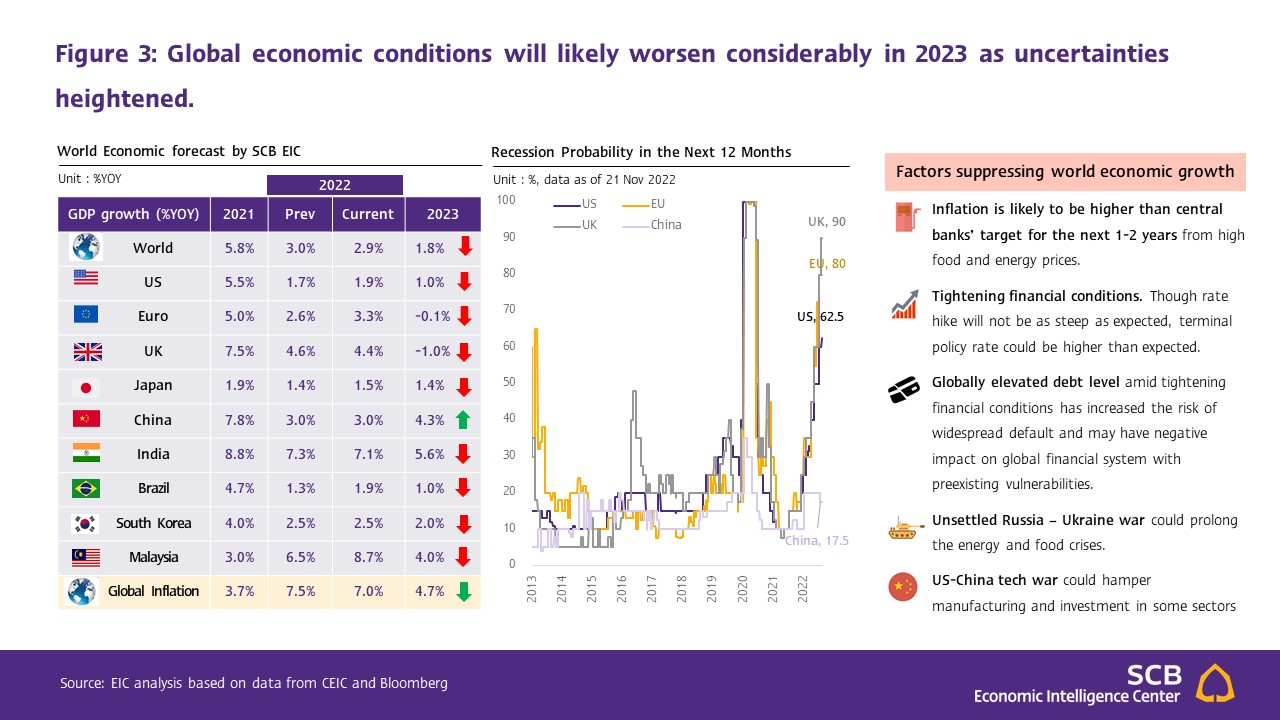

EIC views that Thai merchandise exports should continue to slow in the periods ahead following worsening global economic conditions. In 2023, Thai exports may expand by 1.2%.

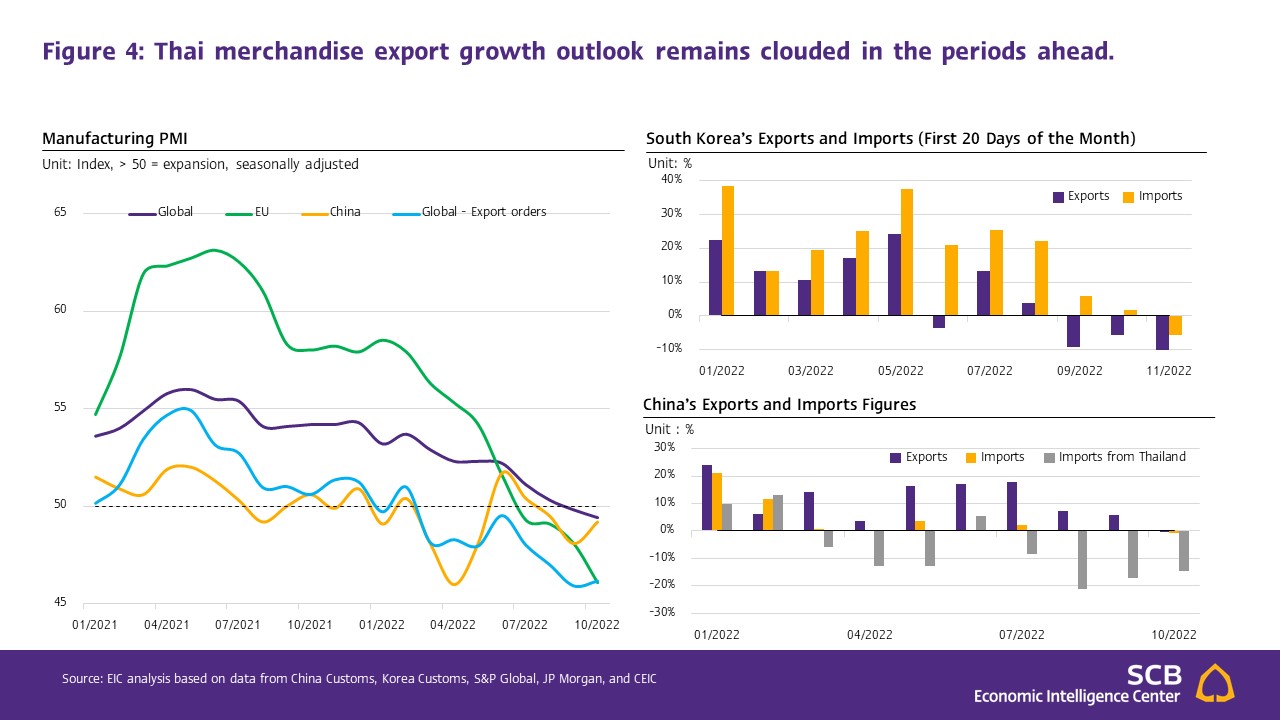

Thai merchandise export growth outlook remains clouded in the periods ahead following worsening global economic conditions. EIC expects that some major economies may face with a recession. The first economies in line are the European Union and the UK that may enter a recession in late 2022, followed by the US in H2/2023. Furthermore, global demand increasingly slowed (Figure 3) as (1) Manufacturing PMI readings of various key partner economies and the Exports order were below 50, (2) South Korea’s export performance during the first 20 days in November tumbled by -16.7%, marking the sharpest contraction in 30 months. During the month, markets that dragged growth were China (-28.3%) and Hong Kong (-35.6%). Meanwhile, South Korea’s import figure dropped by -5.5%, the first contraction in nearly 2 years, and (3) Chinese exports fell in October for the first time in 2 years at -0.3%. Chinese imports also shrank for the first time since August 2020 at -0.7%. Meanwhile, Thai exports to China dropped by -14.5%, representing a 7 consecutive months decline. Such worsening export conditions in China and South Korea clearly reflected a slowdown in global demand (Figure 4) (despite some influence from China’s strict city lockdowns and COVID-19 curbs), which will inevitably slow demand for Thai merchandise as well. With such regards, EIC cuts the Thai export growth forecast in 2023 to 1.2% from the prior forecast of 2.5% in September.