Thai exports saw slowing momentum in July as exports to China plummeted.

The value of Thai exports in July 2022 was at USD 23,629.3 million, increasing by 4.3%YOY (compared to the same period in the prior year).

Value of Thai merchandise export growth in July stalled to a 17 months low.

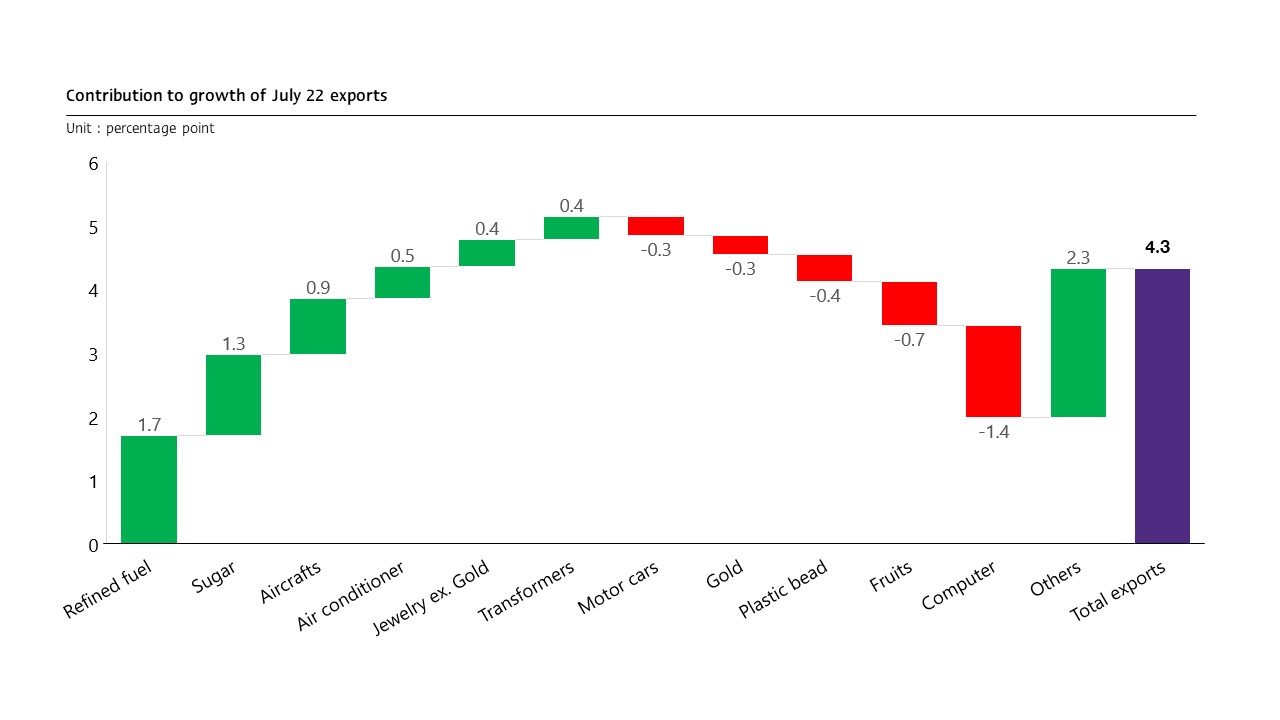

The value of Thai exports in July 2022 was at USD 23,629.3 million, increasing by 4.3%YOY (compared to the same period in the prior year). Such a performance drastically slowed from the 11.9% expansion in June. Despite such growth marking a 17 consecutive months increase, the expansion weakened to a 17 months low. Excluding gold, exports during the month also expanded by 4.7%, slowing considerably from the previous month at 11.5% growth. In terms of the seasonally adjusted month-on-month growth, exports contracted by -7.8%MOM_sa from June. Excluding gold, exports tumbled by -11.9%MOM_sa. During the first 7 months of 2022, Thai exports enjoyed an 11.5% increase. Excluding gold, exports grew by 9.7%.

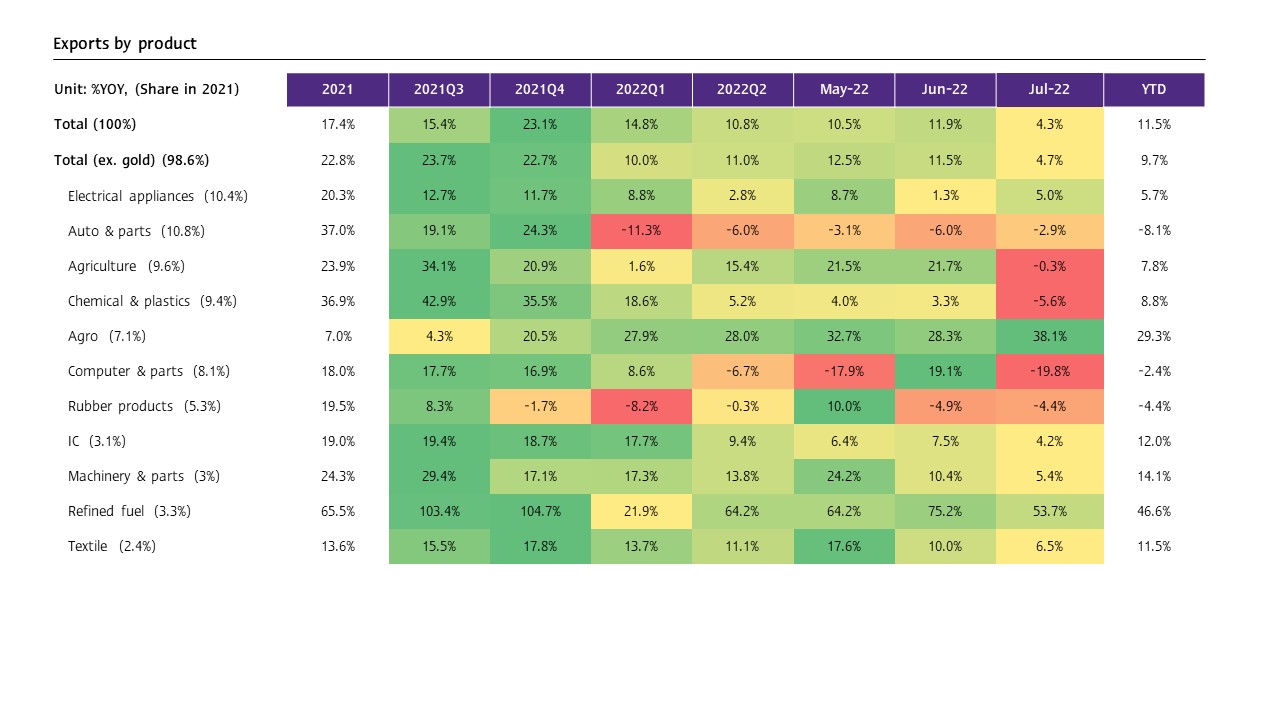

Exports of agro-industrial and mineral and fuel products continued to drive growth. However, exports of agricultural products reverted to a slight contraction.

Analysis of key merchandise export data revealed that (1) Exports of agricultural products that used to see robust growth saw a slight contraction for the first time in 5 months at -0.3%, falling from the 21.7% surge in the prior month. The key products supporting growth during the month included chicken, rice, and rubber. Meanwhile, exports of fruits (especially fresh fruits to China) weakened considerably, (2) Nevertheless, exports of agro-industrial products soared by 38.1%, accelerating from 28.3% in the prior month. The key products driving growth during the month included sugar, animal or vegetable fats and oil, animal feed, and canned and processed seafood, (3) Exports of industrial products stabilized at 0.1%, dropping from 6.7% in the previous month. Excluding industrial products that did not reflect actual export conditions, such as gold, weaponry, and aircraft, exports of industrial products dropped by -0.6%. The key products supporting growth during the month included aircraft, air conditioner and parts, precious stones and jewelry excluding gold, and transformers and components. Meanwhile, exports of computer and parts, plastic beads, gold, motor cars, equipment and parts plummeted, reflecting the impact of the existing chip shortage conditions, and (4) Exports of mineral and fuel products continued to surge by 47.2% after dropping from 73.7% in the prior month. Such a condition was anticipated by EIC in the Flash Exports - June edition that exports of Thai fuel may slow according to global crude oil prices and lower refining costs following concerns that various key economies could enter a recession.

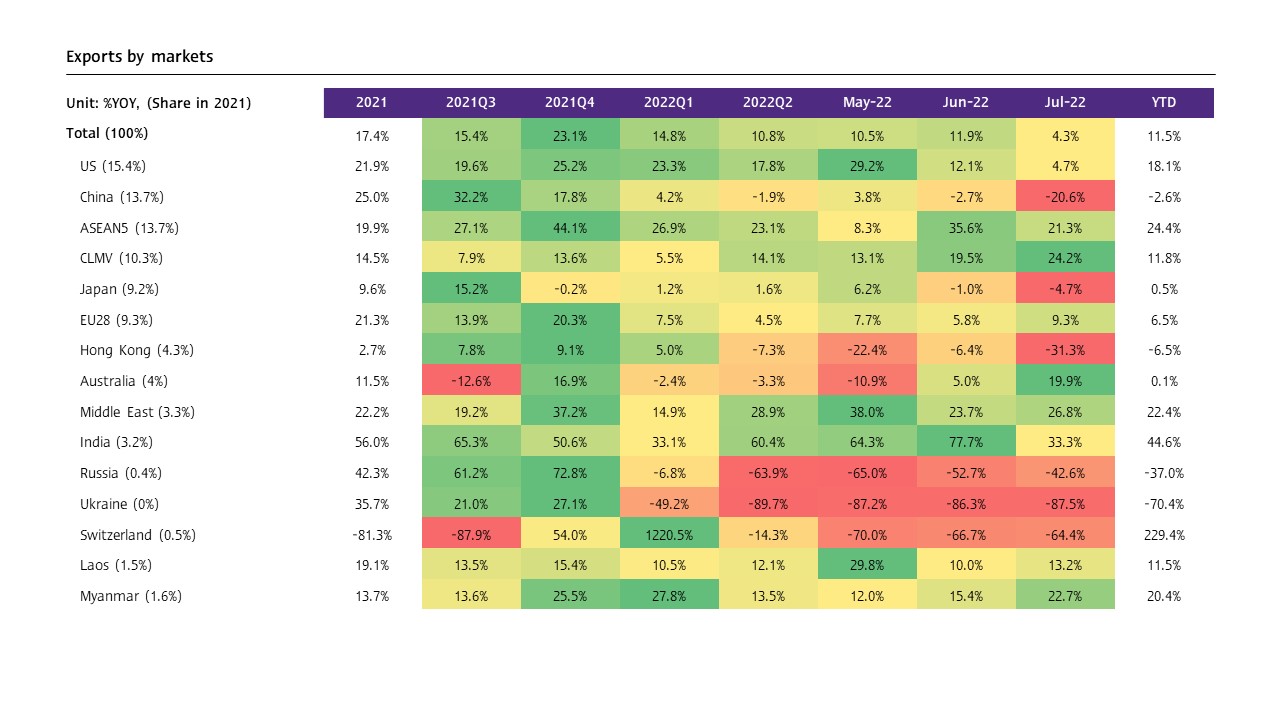

Exports to various destinations signaled clearer slowdowns, especially China, Hong Kong, and Japan.

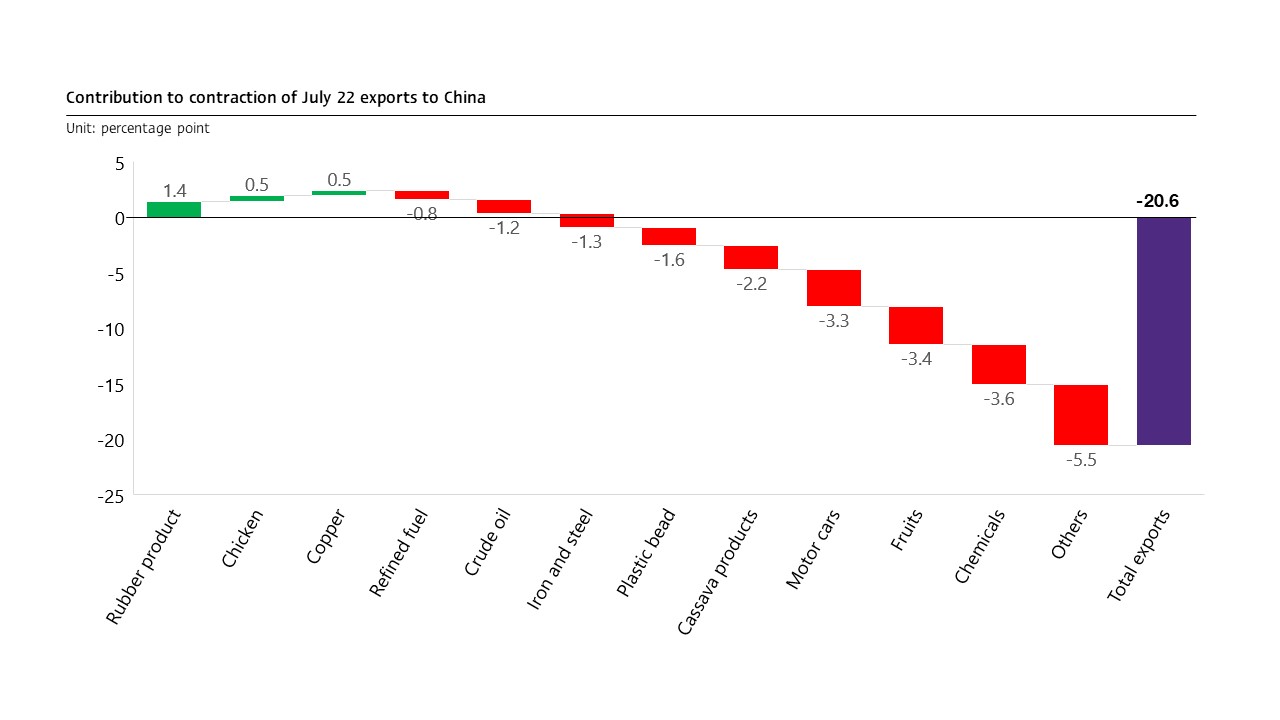

Exports to various destinations signaled clearer slowdowns, in which (1) Exports to China during the month contracted by -20.6%, significantly weaker than -2.7% in the previous month. Such a condition was in line with China’s import figure in July, which grew by only 2.3%, a rate lower than market estimates at 4% (Reuters Consensus). In terms of seasonally adjusted month-on-month growth, the figure also dropped by -1.9% MOM_sa compared to the prior month. Furthermore, the value of China’s imports from Thailand fell by -8.6% (or -12.3%MOM_sa). The key products that undermined exports to China during the month were chemicals, fruits (especially fresh fruits), motor cars, equipment and parts, cassava products, plastic beads, iron, steel, and products, (2) Exports to Japan and Hong Kong fell by -4.7% and -31.3%, respectively, (3) Exports to the US continued to signal slowdowns due to the slowing and uncertain economic conditions, (4) Exports to EU28 continued to grow by 9.3%, despite facing severe economic pressures, and (5) Exports to Russia and Ukraine continued to plummet by -42.6% and -87.5%, respectively. However, such contractions did not have a significant impact on the Thai economy as the markets contributed to only a small share of Thai exports. Meanwhile, exports to CLMV and ASEAN5 continued to improve following gradual economic recovery.

Import growth slowed slightly, prompting the trade balance (in the customs basis) to continue to weaken.

The value of imports in July stood at USD 27,289.8 million, increasing by 23.9%, slightly lower than the 24.5% growth in the prior month. Global energy prices somewhat dropped, thus causing fuel import growth to stall to 79% from 124.8% in the prior month. Imports of vehicles and transportation equipment continued to shrink by -21%. Meanwhile, imports of capital goods and consumer goods reverted to a contraction of -1% and -4.6%, respectively. However, imports of raw materials and intermediate raw products, which had the highest import share at 43.6% of total imports in 2021, surged by 30.2% during the month, accelerating from 11.6% in the prior month. With such regards, the trade deficit during the month registered at USD -3,660.5 million. During the first 7 months of 2022, imports grew by 21.4%, while the trade deficit weakened to USD -9,916.3 million.

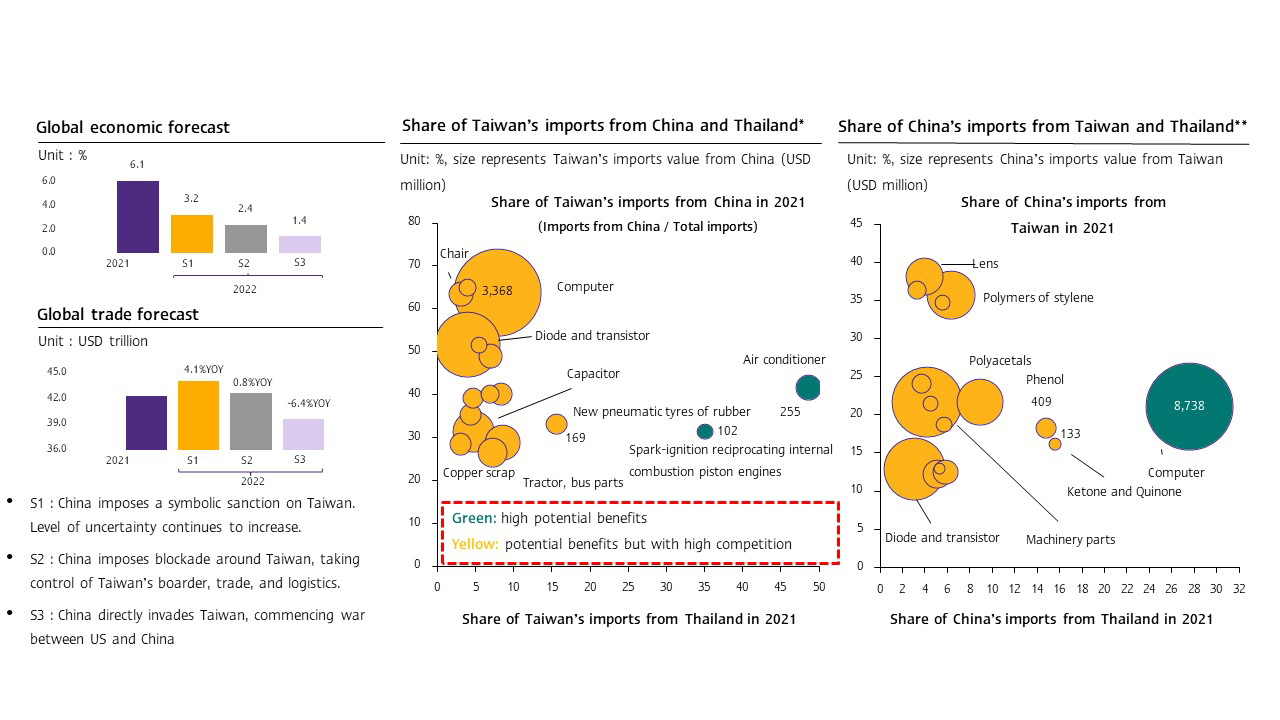

EIC views that the tensions between China, the US, and Taiwan will remain at status quo with limited impact on global economic and trade conditions.

EIC evaluates that the current tensions relating to Taiwan will remain at status quo. In the base case, China could impose a symbolic economic sanction on Taiwan and increase military drills temporarily. Meanwhile, the US may not yet sanction China directly. In such a case, EIC views that global economic and trade conditions should see limited impact. The global economy should continue to recover by 3.2% amid global trade expanding by 4.1% in 2022. However, in the long run, such tensions could accelerate the decoupling of the US and China, thereby slowing international trade and hindering transportation and logistics activities. Regarding trade flows, if trade between China and Taiwan weakens, exports of certain Thai products could benefit, including computers, air conditioners, and engines, as both countries highly depend on such products from the other, and Thailand has market share of such products in the countries.

Going forward, exports should slow due to the risk of a global recession.

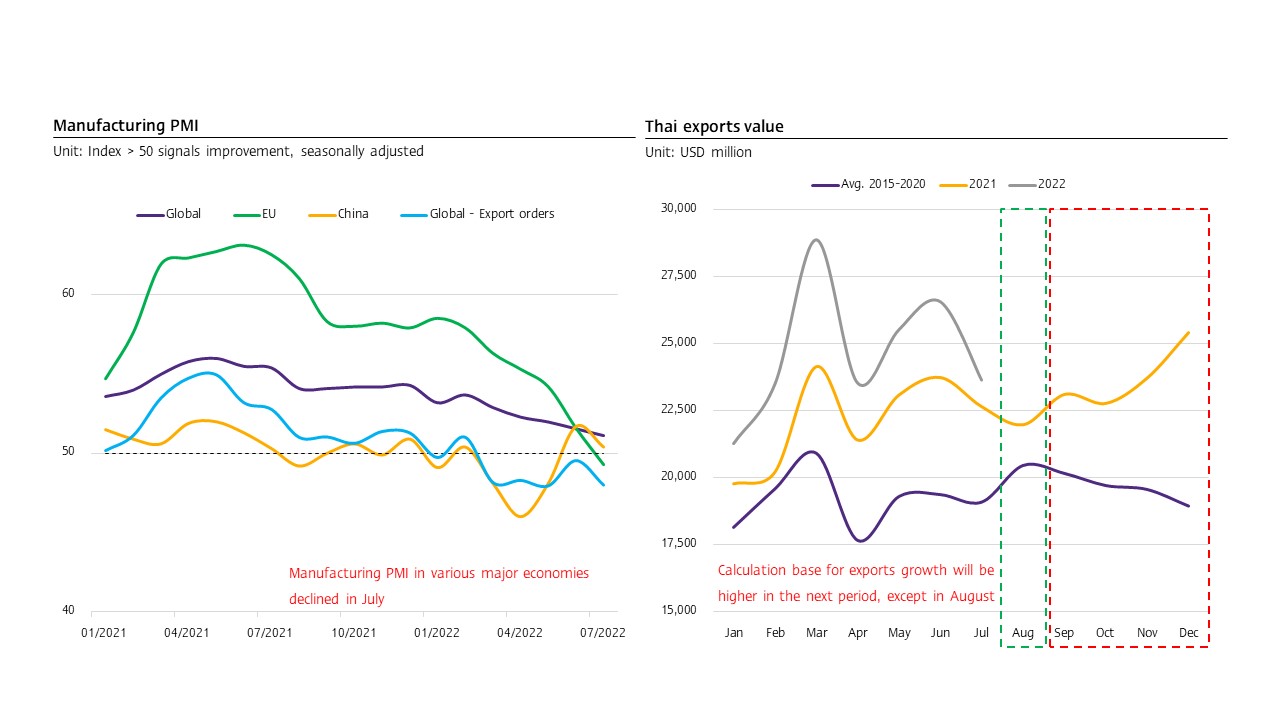

Thai exports grew robustly in H1/22 at 11.5%, though such growth stalled significantly in July. EIC views that the slowing momentum should continue throughout the remainder of the year. Furthermore, the slowdown should be more pronounced from September onwards due to risks and economic vulnerabilities of key trading partners, particularly the US and Europe, with clearer signs of economic slowdowns following inflation levels and tight monetary policy implementations. Meanwhile, strong tourism recovery in Thailand should strengthen Thailand’s current account and may prompt a slight baht appreciation in the periods ahead. However, Thailand’s %YOY export performance in August may temporarily improve due to the low-base effect from August 2021. EIC will closely monitor and revise the export forecast for 2022 from the previous estimate of 5.8% and will publish the updated projection again in September.

Figure 1: Exports signaled clearer slowdowns. Exports to China already plummeted.

Source: EIC analysis based on data from the Ministry of Commerce

Figure 2: A greater number of export products saw weakened growth from the prior month. Particularly, exports of computers reverted to a contraction.

Source: EIC analysis based on data from the Ministry of Commerce

Figure 3: Exports to China contracted considerably. Products that dragged growth were chemicals, fruits, motor cars, cassava products, and plastic beads. Meanwhile, exports of rubber, chicken, and copper supported growth.

Source: EIC analysis based on data from the Ministry of Commerce

Figure 4: In the case of status quo, implications on the global economic and trade conditions will be limited. However, if a war breaks out, global trade will drastically weaken, hence pushing many economies to enter a recession. Note: *Only products Taiwan imported from China with value above USD 100 million, ** only products China imported from Taiwan with value above USD 100 million

Note: *Only products Taiwan imported from China with value above USD 100 million, ** only products China imported from Taiwan with value above USD 100 million

Source: EIC analysis based on data from Trademap, IMF, WTO, and CEIC

Figure 5: EIC expects that merchandise exports will slow in the periods ahead following slowing economic conditions in key importing countries and the high base effect. However, exports in August may accelerate due to the support from the low base factor.