- Confirmation of the newly voted prime minister somewhat clarified political instability. In a positive light, the mentioned event signaled that a new government would soon oversee the country. As such, investor confidence soared, at least in the short-term. Thailand’s stock market, the SET index, rose by 33.19 points during 2019 June 4th – 6th, partly from consecutive political progression – since the announcement of coalitions between Palang Pracharath and various other parties were made, until the PM voting date.

- The return of power to the former prime minister should facilitate policy continuity. Some government policies established during the former government would be beneficial for Thailand, both in the short and long term. Continuity of such projects, for example, mega infrastructure projects in roads, rails, ports, and airports in addition to the development of the Eastern Economic Corridor (EEC) would be detrimental to Thailand’s economy, going forward.

- Despite the power continuity, various political caveats lie ahead.

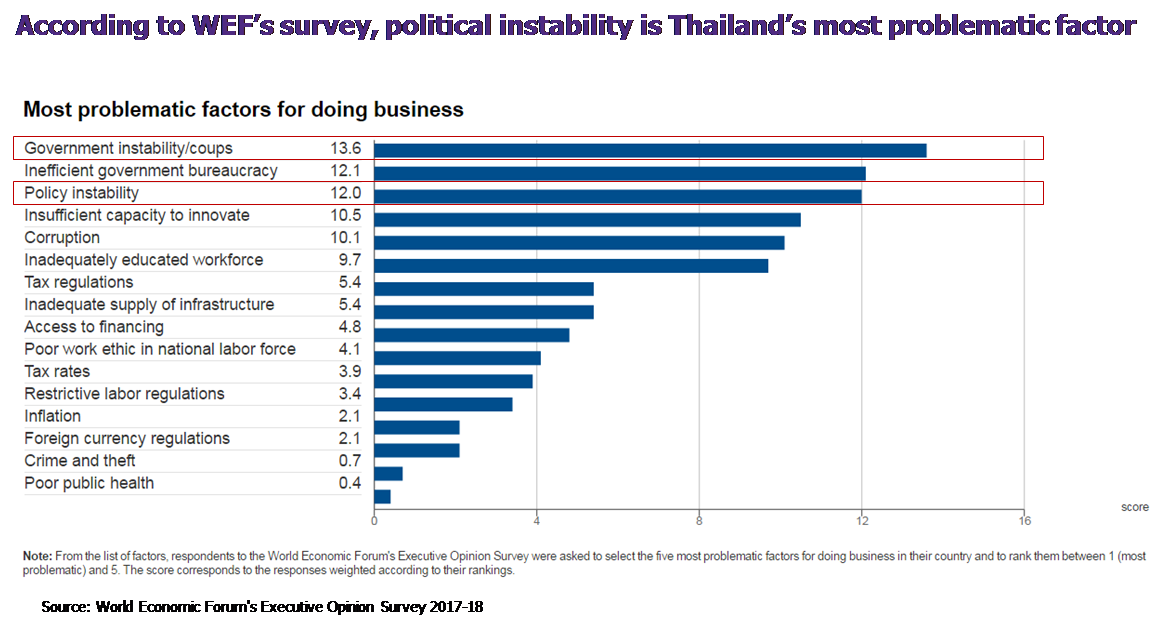

(1) The coalition party has only a slim majority of MP seats reflected by the vote on June 5, 2019, which could hinder the ruling party’s issuance of new policy or legislation. Balancing the interest of each coalition party within the ruling party itself would also be a challenge. Therefore, questions regarding the new government’s longevity surfaced. According to Suan Dusit Poll’s survey1 , over 73.65% of respondents doubt that the new government will complete its 4-years term, of that over 34.07% expect that the new government will not be in power for longer than 1 year. This concern will be a crucial risk factor of Thai economy going forward as political instability is ranked first of the main obstacles for doing business in Thailand, according to World Economic Forum (WEF) Executive Opinion Survey 2017-2018 (Figure 1).

(2) Compromising policies across coalition parties would be another challenge. During the election, the coalition parties campaigned on a range of policies. Many are different, while some aimed for similar goals, though with different deliverables. With such regards, policy selection will be a tough task. The issue is further challenged by budget allocation, as many of the policies require substantial expenditure with ongoing support, such as policies regarding price guarantees for agricultural products or farm income guarantee, allowance for pregnant women, allowance for children from firstborns until a specified age, and the one million house policy. While, other policies, such as promised wage hikes could have a significant impact on the overall economy. A leap wage hikes will directly increase the financial burden for businesses and cause those that cannot afford the hike to go out of business. SMEs are the main concern here, as their current proportion of wage to total cost is likely to be high. Accordingly, although the new government can be set up, policy uncertainty remains, which is the 3rd most problematic factor for doing business in Thailand, according to WEF’s Executive Opinion Survey 2017-2018 (Figure 1). Going forward, the new government should hastily provide clarity regarding economic policy direction in order to reduce instability, while carefully selecting and evaluating policies based on their impact to the economy.

Due to Thailand’s current economic structure and circumstance, EIC believes that the new government could implement the following policies:

(1) If the new government wants to further stimulate the economy, the selected policies should balance between providing aid to those in need and country-wide spending stimulus. There is a high probability that the new government will put economic-stimulus measures as a top priority as Thailand’s economic growth is seen to be slowing due to the trade war impact on the export sector. As such, policies should be targeted to help sectors with poor performance, for example, the business sectors impacted by dwindling exports, the tourism sector impacted by declining tourist receipt, and the agricultural sector impacted by continually dropping product prices. Moreover, country-wide spending catalysts are recommended in order to drive Thailand’s growth with domestic demand, whilst reducing subjected risks from external factors. Policies that can inject money into the economy in a timely manner with a high multiplier effect on the overall economy are advised. However, the policies should not have long-term commitments that might create future fiscal burden and should not overly distort the market till creating a risk that businesses stop developing themselves to increase their competitiveness in the future.

(2) The government should expedite mega infrastructure project construction budget disbursement as per schedule. In the short term, mega project investments, both ones already under construction and ones pending bidding, will heighten Thailand’s investment confidence and help stabilize the economy against global economic slowdown and trade wars. In the long term, the projects will uplift Thailand’s competitiveness via providing quality infrastructure advantage and dispersed prosperity to secondary cities. Infrastructure investments in the EEC should also operate according to planned timeline. Strategies to attract additional private sector investment, especially those in Thailand’s 10 targeted industries, to the area will be beneficial. Also, Thailand could use the current trade war as an opportunity to invite global companies with supply chain investments in China to relocate to Thailand in order to evade trade war tariffs.

(3) Policies to reform the education system and increase existing labor force productivity are advised. Thailand is entering an aging economy, a sustainable solution that will yield continual economic development is hence to increase labor productivity. According to a study by EIC 2 , one way to increase productivity is to improve the quality of education, but with an increasing focus on practicality. The government and universities should cooperate and produce demand-driven labor in order to eliminate the problem of skill-labor mismatch in the market. Moreover, the government should support capability building via a lifelong learning system. In the present, technological development comes at a fast pace, labor needs to be continually trained to stay on top. The government could support by providing incentives to companies that host training or to citizens directly.

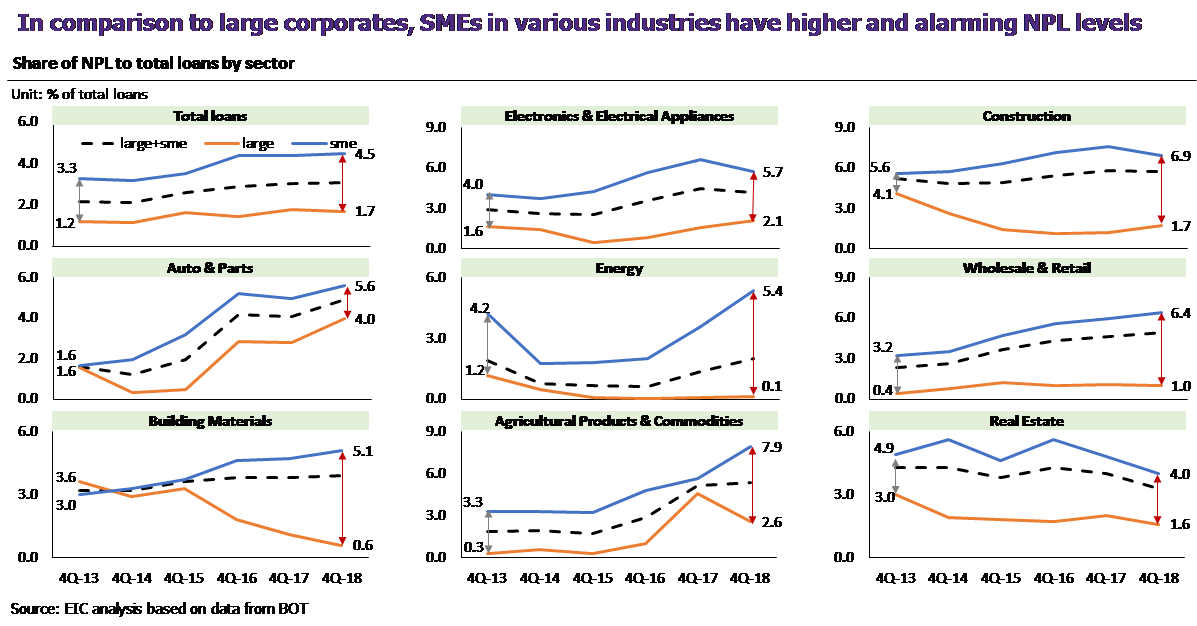

(4) Increase SMEs competitiveness. Data from Figure 2, below, reveal that the nonperforming loans (NPL) gap between SMEs and large corporates grew larger than in the past, signifying lower SMEs competitiveness in comparison to large corporates. In order to help SMEs, a sector employing a large portion of labor, policies that help foster competitiveness, such as technology promotion to reduce costs and increase business opportunities will be beneficial. Other SME specific policy considerations are, for instance, promotion of fair competition, decluttering market concentration, especially those relating to the government, and providing financial knowledge to facilitate business operations.

1 Poll topic “Citizens’ perception on the debate to vote for prime minister” dated Sunday, June 9, 2019

2 For more information regarding Thailand’s labor productivity, read more at In Focus: Assessing Thailand’s labor productivity: “Manageable, yet inadequate and concerning.” https://www.scbeic.com/en/detail/product/5988

|

Figure 2

Figure 2