Basel III-compliant Instruments

The Basel III International Regulatory Framework requires worldwide banks to issue additional capital instruments in order to replenish their regulatory capital. The interesting questions are – What is Basel III? Why are commercial banks set to offer Basel III-compliant capital instruments? What are the risks and returns for these instruments? Are Basel III securities worth investing in? EIC views that Basel III-compliant instruments can be a fruitful option for Thai investors as offering higher yields than other debt securities. However, the Basel III-compliant instruments’ complexity and associated risks are different from other debt securities. Therefore, the investors should take these matters into their consideration prior to deciding to invest in these instruments. The major risks consist of deferrable coupons, none coupon-payment and loss absorption at the point of non-viability.

Author: Piyakorn Chonlaworn and Pakanee Pongpirodom

|

|

Basel III-compliant instruments, also known as subordinated debt, will be drawn more interest of investors. On September 5, 2014 - The Securities and Exchange Commission (SEC) approved of regulations allowing commercial banks to offer Basel III Tier 2 instruments to retail investors. Previously, the banks could only offer these instruments to institutional investors or high net worth investors. Furthermore, SEC has also permitted mutual funds, excluding money market funds, to invest in Basel III instruments offered domestically or overseas, under certain their investment limits. Some interesting questions with regard to these regulations are: What is Basel III? Why are commercial banks set to offer Basel III-compliant instruments? What are the risks and returns for these securities? Are Basel III-compliant securities worth investing in? Changing from Basel II to Basel III means global financial institutions need to strengthen their capital adequacy . Basel is an international regulatory framework designed to monitor and promote financial system stability (Figure 1), especially to strengthen banks' capital requirement in order to improve the banking sector's ability to deal with financial and economic stress. The Basel Committee on Banking Supervision (BCBS) has made continuous efforts to improve the quality of banking supervision worldwide by developing the Basel Accords since 1998 when Basel I was first introduced. Later, Basel II was introduced in 2004 and Basel III was introduced in 2013. In Thailand, The Bank of Thailand (BOT) has also implemented Basel III framework for monitoring Thai banking sector. Under Basel III, moreover, the bank' capital requirement is stricter than Basel II (Figure 2). Total regulatory capital under Basel III consists of the sum of the following elements;

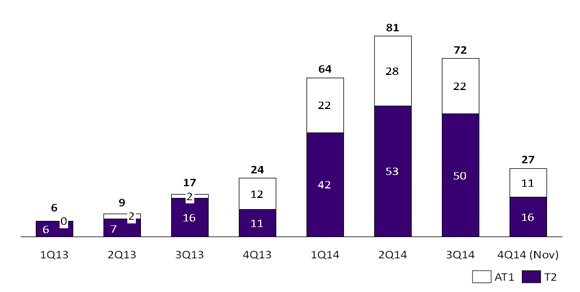

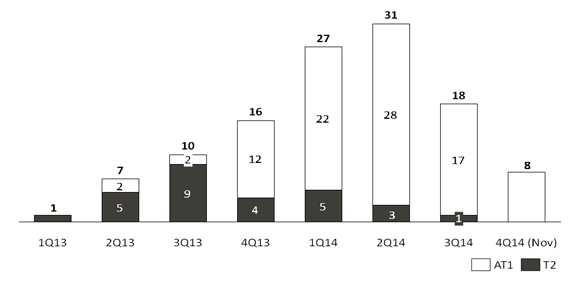

Moreover, in order to raise greater resilience of banks during crises, Basel III framework also requires banks to hold additional capital buffers from CET1 ratio which are; 1) Capital conservation buffer of 2.5% - the buffer will be phased in beginning on January 2016 at a rate of 0.625% each year and will become fully implemented in 2019. 2) Countercyclical buffer with a range from zero to 2.5% above CET1 ratio. Therefore, when the complete package is implemented in 2019, banks will be required to hold minimum CET1 ratio between 7% and 9.5% of risk-weighted assets, or to hold minimum total capital ratio between 10.5% and 13% of risk-weighted assets. In addition, Global Systemically Important Financial Institutions (G-SIFIs) are expected to have higher loss absorbency capacity in order to reflect the greater risks that they pose to the financial system and they have to follow other supervisory measures. The additional loss absorbency requirements are to be met with a progressive CET1 capital requirement ranging from 1% to 2.5%, depending on a bank's systemic importance. According to the Financial Stability Board (FSB), there are currently 33 G-SIFIs. From investors' perspective, Basel III-compliant instruments carry higher risks, yet offering greater returns than other debt securities. Basel III-compliant instruments are classified as subordinated debt because the holder will be repaid after preferential creditors, depositors, and general creditors, but before shareholders. Moreover, some features of Basel III-compliant instruments display the characteristics of equity. They, therefore, can be called "Hybrid securities". The relevant features are; 1) The issuing bank must have full discretion at all times to defer or cancel coupon payments and deferred coupons are non-cumulative. 2) The holder of Basel III-compliant instruments does not have the right to redeem prior to maturity date. However, the issuing bank may have the right to call before the maturity date of instruments. 3) The holder of Basel III-compliant instruments must be absorbed loss at the point of non-viability. Loss absorbency is to be achieved by way of common equity conversion or a principal write-down or both. Because subordinated debt carries higher risks than senior debt, the issuing bank has to offer greater returns to draw investors' attention by paying additional coupons in a range between 1% and 4% above the coupon payments on senior debt. This depends on the risk levels carried by the issued subordinated instruments. Subordinated debts comprise Additional Tier 1 instruments (AT1) and Tier 2 instruments (T2). As AT1 instruments always carry more risks than T2 instruments, they give investors higher returns. Some different subordination risks between AT1 instruments and T2 instruments are (Figure 3); 1) The holder of AT1 instruments will be paid after the holder of T2 instruments. 2) In case of AT1 instruments, coupon cancellation is not considered as default on investors' payment. 3) The holder of AT1 instruments is supposed to absorb loss on a going-concern basis. In other words, if the CET1 ratio is lower than the trigger point of 5.125%, AT1 instruments will be forced to convert into common equity or to write down a principal. If issuing banks become non-viable, T2 instruments will also be required to convert into common equity or to write down a principal, but after AT1 instruments. 4) AT1 instruments are perpetual, whereas the maturity date of T2 instruments is a minimum of five years. Therefore, because of longer maturity, holders of AT1 instruments tend to face more interest rate risk than holders of T2 instruments. Due to the fact that the holder of AT1 instruments carries higher risks than the holder of Tier 2 instruments, AT1 instruments have a high tendency to offer greater returns than T2 instruments (see the example of yield/coupon comparison on Figure 4). Many commercial banks have issued Basel III-compliant instruments, aiming to increase their regulatory capital. According to Bloomberg, since Basel III became active, global Basel III-compliant instruments have continually increased. At the end of November 2014, there was USD 300 billion in Basel III subordinated debts, including a contribution of USD 100 billion from AT1 instruments and USD 200 billion from T2 instruments (Figure 5). In Thailand, commercial banks have begun offering Basel III-compliant instruments since early 2014, but there was only the issuance of Basel III T2 instruments with a total value of baht 71 billion (Figure 6). In 2015, Fitch's ratings expects that Thailand's commercial banks will need to raise more capital around baht 50 billion to baht 60 billion. In foreign countries, Basel III-compliant instruments issued by financial institutions are commonly known as Contingent convertible capital instruments or so-called "CoCos". CoCo bonds are hybrid capital securities that have a capacity to absorb losses by conversion to common equity or a principal write-down in accordance with their contractual terms when the capital of the issuing bank falls below a certain level, prior to the point of non-viability. For example, if the CET1 ratio falls below 7%, the holder will have to absorb loss by either conversion to common equity or a principal write-down. In case of the latter, the principal amount is written down either on a permanent or temporary basis. According to Bloomberg, there was USD 118 billion worth of CoCos issued at the end of November 2014, including a major contribution from AT1 instruments of USD 90 billion and USD 28 billion from T2 instruments (Figure 7). Investors should understand how credit ratings are assigned to AT1 and T2 instruments before making their investment decisions. AT1 and T2 instruments are assigned credit ratings by "notching down" from the issuer's anchor rating. The amount of this notching depends on the bond's terms and conditions, such as subordination risk, the issuer's deferrable coupons or coupon non-payment, and the loss absorption at the point of non-viability (Figure 8). The degrees of repayment risk depend on terms of instruments' conditions. |

|

|||

Figure 1: The Basel III International Regulatory Framework

|

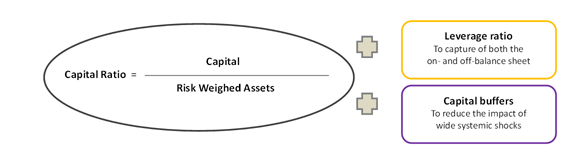

Pillar 1: Maintenance of minimum capital requirement for credit risk, market risk, and operational risk - Financial institutions are subject to maintain minimum capital requirement and capital buffers. The Capital adequacy ratio (Capital ratio or BIS ratio) must be at least 8% of risk-weighted assets, including a common equity ratio (CET1 ratio) at least 4.5% of risk-weighted assets, and a Tier 1 ratio at least 6% of risk-weighted assets. In addition, banks are required to hold additional capital buffers from CET1 which are 1) a capital conservation buffer of 2.5% and 2) a countercyclical buffer with a range from zero to 2.5%. As regards Global Systemically Important Financial Institutions (G-SIFIs), G-SIFIs are expected to have higher loss absorbency capacity in order to reflect the greater risks that they pose to the financial system. The additional loss absorbency requirements are to be met with a progressive CET1 capital requirement ranging from 1% to 2.5%, depending on a bank's systemic importance. Moreover, Basel Committee introduces a leverage ratio to act as a credible supplementary measure together with a capital ratio to ensure broad and adequate capture of both the on- and off-balance sheet leverage of banks. The minimum leverage ratio is currently 3% and can be calculated by dividing Tier 1 capital by total exposure. Overall capital adequacy measures

Although financial institutions have high levels of capital adequacy, they still have a chance to face liquidity problem, which causes them confronting instability and need to receive the government bailout. Therefore, Basel Committee introduces a liquidity coverage ratio (LCR) to ensure that financial institutions have sufficient high-quality liquid assets on hand during financial stress. Under Basel III, banks are required to have LCR at least 100%. In other words, the LCR is supposed to require a bank to have sufficient unencumbered high-quality liquid assets to cover its total net cash outflows over 30 days as well as a net stable funding ratio (NSFR) at least 100% to reduce liquidity disruption from the risk of borrowing short term to finance long term investments (funding mismatch). |

|

Pillar 2: Supervisory Review Process - This process helps to ensure not only the bank has adequate capital to support the risk in their business, but it also encourages banks to develop and use a better risk management technique in monitoring and managing risks, which are not included in Pillar 1. Supervisors will review and evaluate banks' internal capital adequacy assessment process (ICAAP) and conduct a proper stress test. Moreover, supervisors have to monitor and assess the risk management process and the capital adequacy of the financial institution. |

| Pillar 3: Market Discipline - It is a supplemental measure to support the implementation of Pillar 1 and Pillar 2. Banks are required to disclose the details of capital adequacy and risk exposures of the institution in order to allow market participants such as investors, partners or depositors to assess and evaluate the institutions' risk profile. |

Source: EIC analysis based on data from BOT

Figure 2: Capital ratios under Basel III compared with Basel II

|

|||||||||||||||||||||||||||||||||

Source: EIC analysis based on data from BIS

Figure 3: The Content of instruments being eligible for CET1, AT1 and T2 under Basel III

|

||||||||||||||||||||||||||||||||||||||||

Source: EIC analysis based on data from BIS and BOT

Figure 4: Coupon/Yield comparison of AT1 instruments, T2 instruments, and Senior debts

|

Source: EIC analysis based on data from Bloomberg

Figure 5: Value of global Basel III AT1 and T2 instruments

Source: EIC analysis based on data from Bloomberg

Figure 6: Basel III-compliant instruments issued by commercial banks in Thailand

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Source: EIC analysis based on data from Bloomberg

Figure 7: Value of CoCos issuance

Source: EIC analysis based on data from Bloomberg

Figure 8: Assessing credit ratings for AT1 and T2 instruments

|

Standard and Poor's (S&P) ratings approach for AT1 and T2 instruments The methodology for assigning an issuer credit rating to bank's AT1 and T2 instruments is to notch down from the bank stand-alone credit profile (SACP), or in certain situations, from the issuer credit rating (ICR) if the bank gains extraordinary support from the government.

In summary, S&P's base case notching will be at least five notches and two notches below SACP or ICR for AT1 and T2 instruments respectively. |

|

Fitch's ratings approach for AT1 and T2 instruments The methodology for assigning an issuer credit rating to bank's AT1 and T2 instruments is to notch down from the bank viability rating (VR), or in certain situations, from the issuer default rating (IDR) to reflect loss severity risk and non-performance risk. An issuer credit rating will be deducted one or two notches for loss severity risk and non-performance risk. Moreover, securities which are supposed to absorb loss on a going-concern basis will be additionally deducted two to five notches below an anchor rating while securities which have loss absorption on a gone-concern basis will be additionally deducted zero to one notch. In summary, Fitch's base case notching will be at least five notches and one to three notches below VR or IDR for AT1 and T2 instruments respectively. |

Source: EIC analysis based on data from S&P and FitchRatings