Thailand’s alternative TV outlook in the period of digital TV transition

Though the growth of households with cable and satellite TV installations has been aggressive throughout the past 5 years, consumers still prefer to watch free TV channels. TV consumption trends hence cause the advertisement revenues to be clustered in the existing free TV channels. Therefore, the creation of the digital TV is both a risk and an opportunity for alternative TV operators, whereby operators would need to adjust in order to prepare for changes that would occur. Adjustments that should be made are for example, developing on-air systems, improving content quality, adding new services to attract viewers, and finding other revenue sources to replace revenue that could be lost from fiercer competition in the future.

Author: Jaturon Umpai

The aggressive growth in cable and satellite TV installations is triggered by better quality signals, channel variety, and cheaper installation costs. During the past 5 years, Thailand's cable and satellite installations (including True vision) grew drastically from merely 20% of total households with installations in 2008 to 64% of total households in 2012, or an average growth of 40% per annum. There are 3 growth drivers for cable and satellite TV installations. The first trigger for high installation growth is that consumers are demanding for better viewing and sound quality, especially from consumers living in the provincial areas and those living in high-rise buildings, as terrestrial signals are constantly interrupted. The second driver is from demand for a variety of channels; the demand was especially high during the 2008 to 2011 period as viewers want to monitor the political situation. Moreover during 2008, NBTC had established regulations that enable TV businesses that do not rely on frequencies such as satellite and cable to receive revenue from advertisements. This event spurred alternative TV growth from only 358 channels in 2010 to 506 channels in 2013. The last growth catalyst for installations is cheaper installation costs, which is a result of technological development in addition to price competitions spurred by the entry of new players such as GMM and RS during the 2011 to 2012 period.

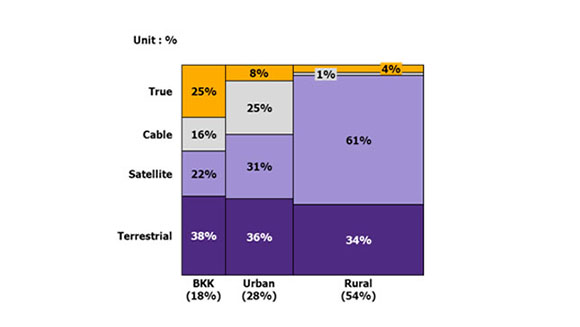

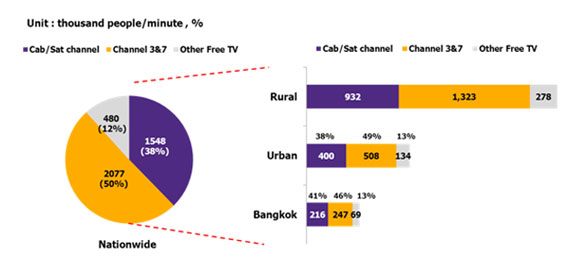

TV consumption trends of urban and rural viewers differ as urban viewers watch TV media via various platforms, whereas rural viewers watch TV media via satellite TV and prefer viewing free TV channels. Consumers in the Bangkok area watch TV media via various platforms such as terrestrial, cable, satellite, and True vision, whereby the portion of the installations of the different platforms are similar (Figure 1). EIC views that Bangkok residents demand for a variety of channels evident from a more fragmented viewing platform (Figure 2). The TV consumption trends of urban viewers are not much different from Bangkok viewers, though the portion with True vision installation is less, which could be due to lower affordability or unsuitable channel content. On the other hand, rural consumers view TV media mainly via the satellite TV platform and prefers to watch free TV channels, especially channel 3 and 7 which together gained market share of 52%. The high free TV market share suggests that rural consumers installed satellite TV in order to improve viewing quality.

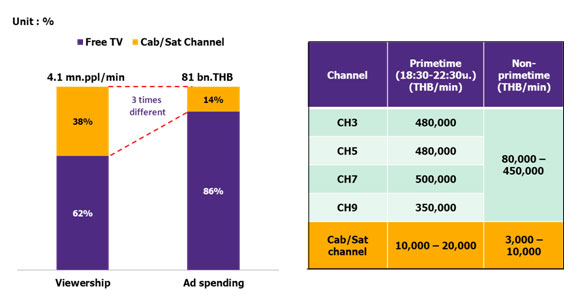

Consumers prefer to view free TV channels over alternative TV channels, causing advertisement revenue to cluster in free TV channels. There are 6 free TV channels, in which the channels occupy 62% of the total market share causing products and services that needs advertisement to still advertise via free TV. Consumer consumption trends hence give free TV operators higher bargaining power for advertisement fees, whereby the current advertisement fee free TV channels are charging is 20 to 30 times higher than that of the alternative channels. Therefore, most of the advertisement revenue is clustered with free TV operators. When considering the amount of viewership during non-prime time, the viewership for free TV and alternative TV channels are similar, some alternative TV channels even have higher viewership for instance music or movie channels such as NBT and TPBS. Although, during prime-time from 6.30 - 10.30 pm, the viewership for alternative channels will usually be 2 times lower than free TV channels but still gains a high market share of 38% which is not in line with their revenue market share that is only at 14%, or 3 times lower than the viewership market share (Figure 3).

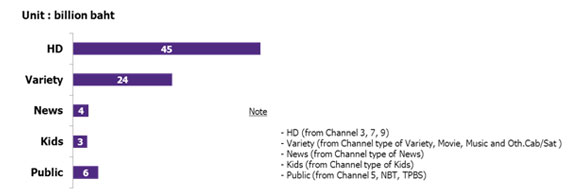

Various alternative TV operators need to join the digital TV race in order to reap advertisement revenues, which should be more equally distributed from higher viewership base. The auction for digital TV channels in December 2013 will change the competitive landscape of TV media, from being monopolized by the existing 6 free TV operators to a more liberalized market. Advertisement revenues are expected to be more equally distributed in the digital TV system from a larger viewership base which is pushed by a more precise rating system creating more reliability for advertisers. Furthermore, there will be 48 digital TV channels to choose from which will be clearly categorized, allowing advertisers to more accurately choose advertisement times and channels, which fits their target group. EIC predicts that if the future viewership and advertisement revenue portion is equally distributed based on current statistics, the HD and variety SD channels will receive the highest advertisement revenues, respectively (Figure 4). The aforementioned reasons cause various alternative TV operators, especially the variety, music, movie, and news operators such as RS, GMM, True, Work point, Amarin, Nation, Voice TV, and others, to want to be a part of the digital TV auction. The digital TV participation will allow alternative TV operators to be incorporated into the mainstream media platform that would potentially increase their advertisement revenue market share when compared to being in the alternative TV platform.

Case studies from foreign countries revealed that cable and satellite TV could still grow simultaneously with digital TV due to various factors, if the right business adjustments are made. Case studies of transitioning into a digital TV era in foreign countries such as England and France indicates that the viewership base of cable and satellite TV would still be the same even though the digital TV scheme is more popular. EIC views that the future of Thailand's TV landscape should be similar to the case studies in foreign countries because of 3 factors. The first factor is that 60% of viewers has cable and satellite TV installations, which can view digital TV channels as obligated by the must carry regulation. Cable and satellite TV operators has the opportunity to increase its viewership base during the period where digital TV coverage is still expanding in addition to the long period of digital TV network development. The second factor is that the alternative TV platforms have more variety and already have a niche customer base such as the political channels. The last factor is that viewers can watch the different TV platforms simultaneously as each household could have more than 1 receiver, though TV operators still needs to make appropriate business adjustments such as content quality development, on-air system development, and incorporate other services in order to retain their viewership base.

Picture 1: Proportion of TV platforms households accessed in 2012 classified by viewing area

Source: EIC analysis based on data from AGB Nielsen Media Research.

Picture 2: Volume and proportion of viewership of different types of channels during a 1 day period classified by area (data retrieved: 9-15 September 2013)

Source: EIC analysis based on data from AGB Nielsen Media Research.

Picture 3: Unequal distribution of advertisement revenue when comparing viewership portion and advertisement fee of free TV and alternative TV channels

Source: EIC analysis based on data from AGB Nielsen Media Research.

Picture 4: Advertisement revenue distribution assumption based on viewership portion classified by types of channels on the digital TV program (data retrieved: 9-15 September 2013)

Source: EIC analysis based on data from AGB Nielsen Media Research.

|

|