Foreign REITs – The Model for REIT Market Development in Thailand

Global REIT market capitalization is on the rise, owing to the fact that many countries have established REIT regimes. Thailand can use foreign REIT practice as a model to develop our REIT market, especially issues related to REIT management fees, debt financing, and performance evaluation and comparison. - EIC believes that good corporate governance, including operating transparency and the prevention of conflicts of interest, will be important factors in enhancing investor confidence and driving the REIT market in Thailand to sustainable growth.

Author: Piyakorn Chonlaworn

|

|

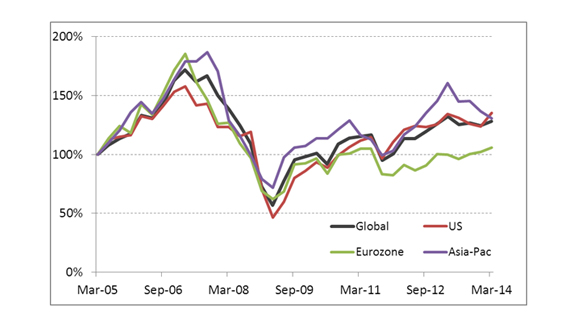

Global REIT value is on the rise, with many countries establishing REIT regimes. Real Estate Investment Trusts, or REITs, were first created in the United States in 1960. Since then, more than 30 countries around the world have established REIT regimes and formulated REIT legislation. Currently, total global REIT market capitalization is valued at more than USD 1 trillion, accounting for 2% of total global stock exchange market capitalization. The US has the largest REIT market, followed by Japan, Australia, UK, Singapore, and Hong Kong. When global REITs were affected by the subprime mortgage crisis and the economic crisis of 2007-2008, REIT values declined immensely in line with stock markets around the world. However, global REIT markets experienced a great recovery after 2009, especially in Asia, where they enjoyed a quicker comeback than in the US and Europe (Figure 1). In Thailand, REITs are covered by a set of regulations under The Trust for Transactions in Capital Market Act B.E. 2550. EIC believes that the Act and regulations implemented by the Securities and Exchange Commission (SEC) in Thailand are similar to regulations in Japan, Hong Kong, and Singapore, enabling Thailand to use those models as a framework in developing the market (Figure 2). According to further study of foreign REITs, EIC believes there are four important factors for successful REIT establishment and management. Areas that REIT founders and managers should consider thoroughly in order to formulate frameworks and communication to enhance investor confidence are outlined as follows: 1. Management Structure : Who will take the role of REIT manager and trustee? What are REIT manager and trustee responsibilities? What are the fees for REIT managers and related parties? 2. Capital Management : What are the leverage policy for REIT? Should it be for short-term debt financing in order to acquire new assets, or long-term debt as a source of capital? What is the debt-to-total-capital ratio? 3. Asset Portfolio Management : Does the REIT specialize in owning certain building types, such as retail, office, residential, or industrial? Or is it a diversified REIT? Will the manager consider investing in assets abroad? 4. Corporate Governance : This includes risk management for investment, preventing conflicts of interest, internal regulations, asset valuation, and complaint and dispute resolution. 1) Foreign REIT frameworks can be studied and used as a guideline for REITs in Thailand, especially in REIT manager's compensation. Foreign REITs use various methods for management compensation (Figure 3). For example, they can be paid based on asset value ratios, variations based on property income, or performance related fees. In some cases, management fees are also paid based on the REIT's acquisition or disposition value. The reason the management fee is paid in accordance with a REIT's actual operating income or performance is to encourage REIT managers to employ active management strategies. EIC believes that management fees that are paid based on performance fees - calculated from net profit by taking into account the cost of debt - should persuade REIT managers to focus more on protecting the benefits of unit holders and avoiding excessive interest expenses. 2) Capital management by means of debt financing for REITs must be carefully exercised. Debt can cause higher volatility of unit trust value. One of additional features when converting from a Property Fund to a REIT is that a REIT can have more borrowed capital. A Property Fund can borrow up to 10% of total assets, whereas REITs can borrow up to 35% of total assets or 60% if the REIT is investment grade. This change brings the important question of whether or not a REIT should borrow. There are three factors to consider in answering this question.

According to these three findings, EIC believes that although leveraging is a financing method that can result in higher dividend yields and attract investors, it also means greater price risks for REITs. Therefore, debt financing for REITs must be implemented wisely to avoid higher price volatility, which could lead to losing investors who have low tolerance for investment risks. REIT managers who wish to raise capital through debt financing instead of equity might do it with appropriate market timing. Debt should be created when the cost of debt is low or during times when the stock market is weakening and the cost of equity therefore high2. Due to the fact that REITs are able to borrow, it is best to rely on a REIT's asset yield ratio when examining its performance. Property Fund regulations allow only up to 10% in total asset borrowing, which is not a very high loan percentage. As a result, dividend yields are similar to asset yield ratios. Comparison of Property Funds that have similar assets based on dividend yield is fairly acceptable, however, this is not the case for REITs. REITs with high leverage usually have a high dividend yield but also higher price fluctuation. Thus, REITs should be examined based on asset yield ratio. The method widely used internationally is to consider Funds from Operations: (FFO)3, which measures how much cash is generated by a REIT's asset portfolio. Investors are advised to analyse REITs by examining the FFO to total asset ratio and then considering the capital structure, such as the debt-to-capital ratio. REITs with a high debt-to-capital ratio are suitable for yield-oriented investors who are able to handle greater risks. 3) REIT managers can exercise good asset portfolio management to create more value for REITs.Acquiring additional assets is not very common for Property Funds, however, a REIT manager will play a more fruitful role in implementing strategies and acquiring high yielding assets for REITs. Large REITs, mostly in Japan, Hong Kong, and Singapore, usually have a higher number of projects (Figure 6). Investors often expect the REIT manager to implement effective asset management by means of acquisition, divestment, or development, or to enhance the value of assets to maximize REIT value. Cross-border acquisition of REIT markets in Asia is expected to rise. It is interesting to note that Singaporean REITs are rather large, despite domestic assets being limited and too costly to be acquired by REITs. Some Singaporean REITs are investing in assets in other countries, especially in China, increasing the diversification of Singaporean REITs' portfolio (Figure 7). EIC holds the view that there are signs that cross-border acquisition of REIT markets in Asia are on the rise, owing to the fact that assets in some countries, such as Singapore and Hong Kong, are very expensive. 4) Good corporate governance is an important driver that will help drive REIT markets in Thailand towards sustainable growth. Several case studies of Asian REITs reveal that potential conflicts of interest usually arise from weaknesses in governance practices. This is because in Asian markets, REIT managers, sponsors, and major shareholders are sometimes related, or often have different and occasionally conflicting interests. For example, when REIT sponsors are also major shareholders or when a sponsor's subsidiaries take roles as REIT managers. Conflicts of interest can lead to unfavorable impacts for minority shareholders if REIT managers acquire overpriced assets from sponsors or divest underpriced assets to sponsors. This relationship between REIT managers and sponsors can affect investor confidence. In addition, some studies show that strong corporate governance has a positive correlation to REIT performance4. In the past, there were not many property fund acquisition and divestment transactions, hence corporate governance structures were often neglected. This should not be the case for REITs, as they are likely to face more acquisition and divestment transactions. EIC is of the opinion that initiating good corporate governance at an early stage will be essential for successful REIT markets in Thailand, especially in safeguarding the benefits of minority shareholders. Important practices include creating a strict set of rules regarding trustee roles and responsibilities in preventing conflicts of interest, formulating fair practices that allow minority shareholders to raise issues against transactions that are not beneficial for a REIT, and enforcing transparent and fair valuations when high value assets are being priced for the purpose of REIT acquisition or divestment. Although these practices are not legal requirements, both regulators and relevant parties should encourage the following of these practices for their mutual benefit. |

|

|||

Figure 1: Performance of REITs by region

Remark: Base date = March 2005

Source: EIC analysis based on data from Bloomberg

Figure 2: Comparison of REIT regulations in Thailand, Japan, Hong Kong, and Singapore

|

Source: EIC analysis based on data from CFA Institute and European Public Real Estate Association

Figure 3: Examples of REIT management compensation in foreign markets

|

Source: EIC analysis based on data from CFA Institute

Figure 4: Comparison of REITs in Japan, Hong Kong, and Singapore

|

Remark: Cap Rate = Operating Income / Total Capital

Cap Rate, Dividend Yield and Debt-to-Total-Capital ratio is as of 06/06/2014

Monthly return Standard Deviation are calculated from TSE REIT Index, FTSE Strait Times Real Estate Index and Hang Seng REIT Index during 01/2009 - 05/2014

Source: EIC analysis based on data from Bloomberg

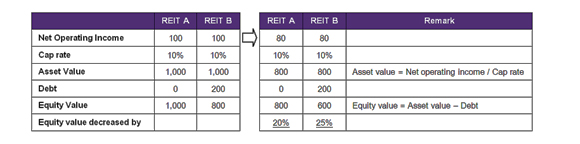

Figure 5: Explanation of how higher leveraged REIT will have higher price volatility

- Compare REIT A and REIT B. Assume both REITs have annual net operating income of Bt 100 mn. REIT A has no debt, while REIT B has Bt 200 mn debt.

- Both REITs have similar asset quality and income growth rate. Assume the same cap rate for both REITS at 10%.6

- Asset value of each REIT can be computed as net operating income divided by cap rate or = Bt 100 mn / 10% = Bt 1 bn.

- As REIT A has no debt, equity value of REIT A should be Bt 1 bn. Since REIT B has Bt 200 mn debt, its equity value should be Bt 800 mn.

- Suppose both REITs' incomes are lower. Assume net operating income decrease by 20% from Bt 100 mn to Bt 80 mn. Fair asset value of each REIT should decrease to Bt 80 mn / 10% = Bt 800 mn.

- As REIT A has no debt, new equity value should be Bt 800 mn or decrease by 20%. For REIT B, which has Bt 200 mn debt, new equity value should be Bt 600 mn or decrease by 25%.

- This scenario analysis shows that when two similar REITs experience the same percentage of lower net operating income, REIT with higher debt-to-capital will have larger decline in equity value. In other words, for REITs that have similar assets, the one with higher leverage will have higher price volatility.

Source: EIC analysis based on data from Alpen Capital and Pew Research Center

Figure 6: Type, quantity, and size of REITs in Japan, Hong Kong, and Singapore

|

Remark: Market Cap is as of 06/06/2014

Source: EIC analysis based on data from Bloomberg

Figure 7: The 5 largest REITs in Japan, Hong Kong, and Singapore by Market Cap

|

Source: EIC analysis based on data from Bloomberg

1 Sun, L., Titman, S. D. and Tw2ite, G. J. (2014), REIT and Commercial Real Estate Returns: A Postmortem of the Financial Crisis. Real Estate Economics.

2 Sun, L., Titman, S. D. and Twite, G. J. (2014), REIT and Commercial Real Estate Returns: A Postmortem of the Financial Crisis. Real Estate Economics.

3 Cost of equity is the summation of risk-free rate and equity risk premium. During times when the stock market is weakening, the cost of equity is high because general investors become more risk averse and demand higher equity risk premium to compensate for taking higher risk in equity investment.

4 According to the accounting standard, firms may not be required to disclose Funds from Operations. Still, practitioners can calculate Funds from Operations using the formula: Funds from Operations = Net Income + Depreciation + Amortization - Gains on Sales of Property

5 Sing, Tien Foo (2013), Does Corporate Governance Matter for REITs? - Re-Examining 'The REIT Effect'

6 Atchison, Yeung (2014), The Impact of REITs on Asian Economies. Asia Pacific Real Estate Association

7 Cap rate can be implied as the cost of capital less income growth rate. According to Modigliani-Miller Proposition 1, for non-taxable entity like REIT, the cost of capital cannot be reduced by debt financing. Therefore, for two REITs that have similar asset type and income growth rate, cap rate should be the same.