Focus on home improvement stores: High growth, fierce competition

Higher consumer purchasing power and rapid expansion in residential property developments trigger the strong growth potential for home improvement retailers. However, competition is high and rising as big players continue to roll out new stores, especially in upcountry, and to tailor their business models to meet local demand.

Author: Pranida Syamananda and Nutchaya Arakvichanun

Higher consumer purchasing power and rapid expansion in residential property developments trigger the strong growth potential for home improvement retailers. However, competition is high and rising as big players continue to roll out new stores, especially in upcountry, and to tailor their business models to meet local demand.

Home improvement retailing, which focuses on sales of building materials and interior decorative goods, is growing significantly thanks to higher household purchasing power and a growing consumer preference for modern trade stores. During the past three years, starting before the floods of late 2011, demand for these products has grown steadily. The sector's major players have enjoyed growth in sales by up to 16% each year from 2009 to 2012, far above the average 3% growth rate for non-grocery retail sales in general. One reason is higher incomes both in Bangkok and the provinces. Bangkok's population having middle income and above (over 15,000 Baht per month) has increased from 37% of the total in 2007 to 46% in 2011, while in the outer provinces the share has risen from 14% to 19%. By 2020 the middle-income-and-up share of the national population is expected to grow to 40%, from 20% today. The rise in purchasing power will propel this sector, as seen in well-established trends. During 2007 to 2011, for example, the housing expenditure has increased by 33% per year among consumers in Bangkok and 10% per year in other provinces. Another factor supporting growth is a rising consumer preference for convenience and product varieties, which favors modern trade retailers. And consumers are increasingly adopting a do-it-yourself approach to home improvement, boosting demand.

The other big supporting factor is growth of the real estate sector in Bangkok and other major provinces. Housing projects in these areas have shown obvious growth during the past three years. In 2013, the large developers plan to continue their expansions, especially in major provinces. Sansiri PCL, for example, is planning 60 billion Baht in project investments, 73% of it in Bangkok and 23% in major provinces. Land and Houses PCL plans to invest 43 billion Baht, 80% for Bangkok and 20% elsewhere. The provinces outside Bangkok that have drawn the most attention from developers include Phuket, Chonburi, Hua Hin, Chiang Mai, Khon Kaen and Udon Thani. This will boost demand for home improvement products as well.

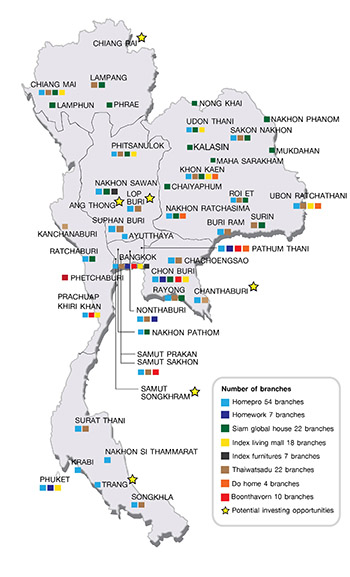

Beyond these major provincial areas, other provinces will also generate opportunities for these retailers. Among these are Chanthaburi, Trang, Lopburi, Chachoengsao, Chiang Rai, Samut Songkhram, and Ang Thong. These provinces have few home improvement retailers despite their population density. Moreover, many of the provinces mentioned above also have higher rates of electricity usage per household compared to the national average of 1,600 Kilowatts per hour per user, which reflects higher spending on household and electrical goods. Not only that, some provinces like Chiang Rai and Chanthaburi are located in the border areas and could attract customers from neighboring countries as well.

Major players, especially Big-box model, are rapidly adding branches to conquer prime locations. Possessing the prime location is extremely advantageous because good sites near cities and residential areas are hard to find and rising in price. Building a branch requires approximately 6-9 months of construction, so faster expansion means faster access to consumers nearby, especially in locations without modern trade competition. The 'first mover' advantage is especially significant for companies operating home centers or big-box stores, which have more than 50,000 SKUs. All of these players are competing for locations nationwide. Home Pro plans to expand by at least eight branches, Siam Global House will add 10-12 branches and Thai Watsadu plans 10 new branches. Furthermore, specialty retail stores, like Boonthavorn and Index Living Mall, are also expanding in 2013. Boonthavorn plans two new branches in Chiang Mai and Phuket, while Index Living Mall will add three stores.

Home improvement chains are now competing to reach consumers in segments where they lack market share. Purchasers of home improvement products can be split into two types, namely consumers and contractors or developers. Consumer turn to specialty stores when they have specific needs, such as buying tiles at Boonthavorn or furniture at Index Living Mall. However, if they seek convenience, they will go to one store where they can get many products, like Home Center format. However, operators have begun to diversify in response to demands from another segment. One successful model addresses market segmentation, such as the Central Retail group investing in construction materials store in order to expand their customer base into all segments, including contractors, rather than their original model of Homeworks, which focused on retail consumers. Recently, Home Pro, which deploys the big-box format, has planned to target the builder and contractor market by opening a new store format under a brand called Mega Home, which focuses on bricks, cement, sand and other basic construction materials. At the same time, Home Pro will continue to add branches to further penetrate the retail consumer segment.

Retailers can differentiate by developing new and better services and loyalty programs. Relevant services include design, installation and repairs/renovation. Repair and renovation services are significant because independent workers and contractors are increasingly hard to find. Some operators are developing more on-site home services to attract consumers, such as monitoring, cleaning and replacing products as well as painting and renovations. Even though this income is not a main part of total revenue generated by the retailers, it is a selling point that can attract new customers and develop loyalty through customer satisfaction. Another strategy that should not be overlooked is a good loyalty program. Because purchases of home improvement products are not as frequent as for other consumer goods, a loyalty program or membership card can help attract customers to return to the same store.

Figure 1: Branches of home improvement stores in provinces with high potential

Source: EIC analysis

Figure 2: Strategies and performance figures among big-box retailers

Source: EIC analysis based on data from company reports and media

Figure 3: Strategies and performance figures among specialty retailers

Source: EIC analysis based on data from company reports and media

|

|

|

|

|