Low cost airline business … competition in the Thai skies

Competition among Thai airlines, especially in the low cost airline segment, has become more aggressive. During the past five years, low cost airlines drastically increased their competitive capacities as seen from the significant market share they have gained at the expense of full service players. During 2009-2013, revenues for low cost players grew at a higher pace, with average EBITDAR growth of 42%. The coming into force of the ASEAN Open Sky Policy in 2015 will increase regional competition and investment in Thailand’s airline industry, as it is a growing tourism destination with high potential as a South East Asian air transport hub. To cope with this anticipated competition, Thai airline players should constantly monitor the business landscape and adjust their strategies accordingly.

Author: Supree Srisamran and Sintawat Sintanabodee

|

|

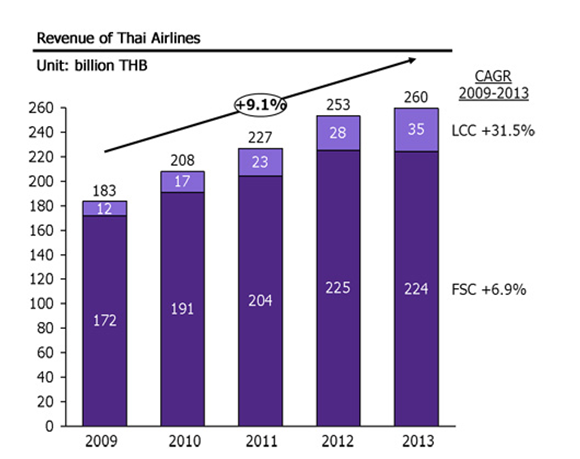

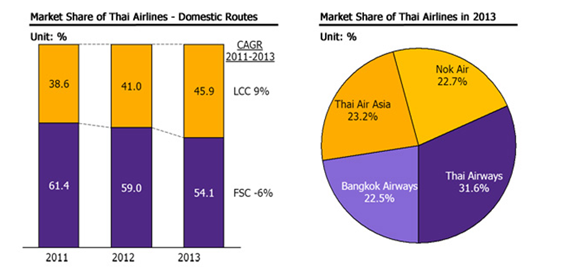

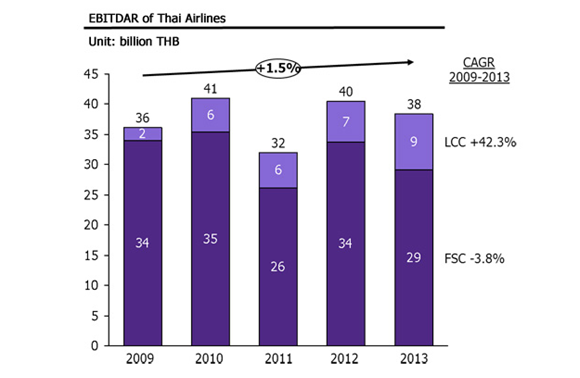

During the past five years, low cost airlines drastically increased their competitive capacities, gaining significant market share at the expense of full service players. According to the International Air Transport Association (IATA), Thai airlines have been competitive during the past five years (2009-2013), in line with global trends. Overall revenue growth for Thai airline players was 9%1, however most of the growth was from low cost airlines, whose average revenue growth was 31.5% compared to low 6.9% growth for full service players (Figure 1). Though full service airlines currently dominate the market, low cost airlines are growing rapidly and reaping market share from conventional players. In 2013, low cost airlines held 46%2 of Thai airline market share (calculated from revenue received from domestic routes), while full service airlines held 54%. Thai Airways, a full service airline, still leads the market with the highest domestic market share at 31.6%, followed by Thai AirAsia, Nok Air, and Bangkok Airways at 23.2%, 22.7%, and 22.5%, respectively. From a market share growth perspective, during 2011-2013 low cost airlines' market share growth was 9%, while full service airlines' market share growth dropped by 6%. The player with the highest market share growth was Nok Air at 16.5% (Figure 2). Low cost airlines outperformed full service airlines with higher EBITDAR growth of 42%. During 2009-2013, the average EBITDAR growth of low cost airlines was 42%, while for full service airlines the rate dropped by 4%. Low cost airlines' EBITDAR growth was higher than revenue growth due to efficient cost management, especially regarding fuel, airplane O&M, and staff related expenditures. Hence, low cost airlines were able to cut expenditures by more than 10%, resulting in better business results than full service airlines (Figure 3). The Open Sky Policy will bring fiercer competition in the Thai airline industry in 2015, as various ASEAN airlines are interested in joining the Thai battlefield. In the past, strict regulations in Thailand prevented others from serving routes already operated by national airline Thai Airways. However, these regulations were eased in 2002, increasing competition in the Thai airline industry. Thailand will become part of the ASEAN Economic Community (AEC) in 2015, under which member countries have agreed to a more liberalized Open Sky Policy in order to facilitate air transport. Under the Open Sky Policies, the third, fourth, and fifth freedom of the air3 allow unlimited rights for air transportation of passengers and goods among ASEAN cities. In other words, airlines can provide passenger and cargo services to cities throughout the region. This liberalization will lure ASEAN airline players into Thai skies, as already evident from Indonesia's low cost Lion Air Group establishing Thai-Lion Air in Thailand in late 2013. Moreover,this year Kan Air will form a joint venture with VietJet to service low cost airlines in Thailand. As such, the Open Sky Policy will immediately allow ASEAN airlines to serve Thailand, resulting in fiercer competition. Airline operation in Thailand is attractive because Thailand is a growing tourist destination and a potential South East Asian air transport hub. Outbound airline activities in Thailand were stimulated by tourism promotions in other Asian countries, such as visa exemptions in Japan and Korea or concerts and food festival tours in South Korea, prompting various Thai airlines to start servicing new routes. For example, Thai AirAsia launched Thai AirAsia X to provide long haul trips to Japan, Korea, and Australia, while Nok Air launched NokScoot to provide services to Japan and Korea. Meanwhile, inbound airline activities in Thailand are promoted via the Tourism Authority of Thailand's 2014 campaign, which seeks to attract tourists with Thai charm. Air transport activities in Thailand are further boosted by Thailand's strategic location at the center of South East Asia, making it ideal as an air transport hub facilitating trips within ASEAN. The various attractive factors should increase the number of flights and passengers Thai airline players will service. Airports of Thailand (AOT) forecasts that in 2015 Suvarnabhumi airport will serve more than 56 million passengers and over 300,000 flights. All in all, the factors we have mentioned will increase travel demand in Thailand and hence should persuade other ASEAN airline companies to take advantage of the opportunities, bringing fiercer competition to the Thai airline industry. 1 Revenue, EBITDAR, and market share calculation is based on information from Thai Airways, Bangkok Airways, Thai AirAsia, and Nok Air.

Figure 1: Low cost airline revenue growth was approximately 24.5% higher than full service airlines.

Remarks: LCC = Low Cost Carrier and FSC = Full Service Carrier Figure 2: Low cost airlines were reaping market share from full service players, indicating higher competitive capacity. Remarks: LCC = Low Cost Carrier and FSC = Full Service Carrier

Figure 3: Low cost players outperformed full service players with EBITDAR growth of 42%. Remarks: LCC = Low Cost Carrier and FSC = Full Service Carrier |

|

|||