4 technologies that will disrupt the petrochemical industry

Author: Nattanan Apinunwattanakul

|

Highlight

|

As an extraction technology, fracking is capable of extracting a large quantity of natural gas, which can, in turn, be made into petrochemical raw materials. Fracking is an extraction technique that combines two technologies, hydraulic fracturing and horizontal drilling. The technique involves pressurized injection of chemicals and sand into the ground. The process causes fractures in the rock, through which shale gas and shale oil are released.

In the US, fracking technology has lowered the cost of shale gas among ethylene producers. This is because shale gas extracted through this method has become available in large supply and at a lower cost, leading to an expansion in ethylene and gas cracker production. The EIA estimates that ethane cracker production in the US will grow by 16.3% per annum between 2016 and 2018.

The Gas Cracker method can produce a proportion of 82% ethylene, whereas the Naphtha Cracker method can only produce 30% ethylene. Therefore, this new technology yields a higher ratio of ethylene. As for propylene, which is another important petrochemical precursor, the Gas Cracker method can produce a proportion of 13% propylene. By contrast, the Naphtha Cracker method can producer a higher proportion of 15% propylene. As a result of the lower proportion, the market’s demand for propylene currently does not meet supply.

On-purpose precursor-sourcing technology will help alleviate the problem of shortage in petrochemical precursors. While the US has shale gas as a main petrochemical precursor, China uses coal as a source of petrochemical production to meet domestic demand. On-purpose technology has been introduced to coal extraction to produce a petrochemical precursor called coal-to-olefin (CTO) and methanol-to-olefin (MTO). Moreover, On-purpose Technology can address the issue of low-proportion propylene that results from the Gas Cracker method. An on-purpose technology called propane dehydrogenation (PDH) uses propane to pull out hydrogen atoms in order to more effectively extract propylene as an important petrochemical precursor.

The aforementioned technologies will present challenges to the petrochemical industry in competitiveness between international players. Competitors in the US have advantage in the lower production costs of both ethylene and propylene as a result of fracking technologies for shale gas and PDH. In Asia, particularly in China, the CTO and MTO technologies remain expensive. However, if China succeeds in lowering their production costs in the future it will become a competitive player, thus presenting a challenge to other players in Asia, most of which are Naphtha-based producers, such as companies in South Korea, Japan, and Taiwan. Therefore, exports to China may not expand as fast as before. In this regard, previous exporters will face ruthless competition and will likely be forced to find new markets or to produce specialty products in order to remain competitive in the petrochemical market.

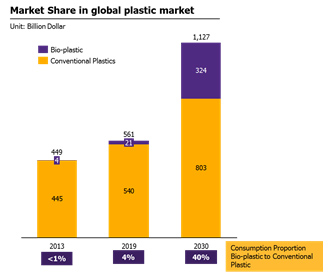

Bio-plastic Technologies can contribute to the development of new specialty products and can also satisfy the expectations of environmentally conscious customers.In a climate of heightened environmental awareness, producers have taken to producing a larger amount of bioplastic beads, most of which are used in the packaging industry. PLA, PHA, and PET are plastic beads that enjoy high growth rates in the bioplastic market, which is expected to grow by 30% between 2013 and 2030. By comparison, the conventional plastic market will only grow 3% per annum.

However, white the EIC sees bioplastic not fully replacing conventional plastic, its share will be larger in the future. In 2013 bioplastics accounted for only 1% of the global plastic market. However, the figure will increase to 4% and 40% in 2019 and 2030 respectively. Thailand has a distinct advantage in bioplastics, as the country produces cassava and sugar at a rate that sufficient for both domestic consumption and overseas exports. Therefore, Thailand will be a competitive player in the global bioplastic market.

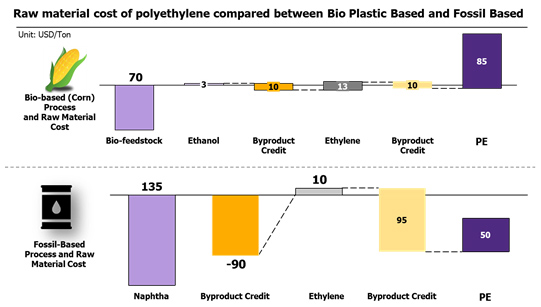

However, the main challenge of the bioplastic market is production costs. At present, the cost of bioplastic is 1.5-3 times that of conventional plastic beads, depending on the type. Although the cost of producing bioplastic is expensive, it is expected that manufacturing innovations in the near future will bring down the cost by introducing new raw materials, such as waste from rice straw, rice husk, and tree bark. In conjunction with other technologies, these materials can replace the current use of cassava, sugarcane, and corn as sources of bioplastic beads, thus lowering the cost of bioplastic production.

3D printing is another important technology to create new opportunities for plastic producers. 3D printing is a printing technology that converts digital data, such as letters and images, from a computer program into tangible final products. The two main types of plastic used in the process are acrylonitrile butadiene styrene (ABS) and polylactic acid (PLA).

In the process of 3D printing, the designer creates a 3D model using a CAD (computer aided design) program. Once the model is ready as a digital file, the file will be entered into the printer, which uses plastic as a material for three-dimensional modeling.

3D printing is useful because it can produce inexpensive prototypes in real time. Moreover, it can lower production costs as 3D printing reduces the time span in the supply chain, transportation costs, and material storage due to being lighter in weight than other products. This helps foster the efficiency and sustainability of production, and the flexibility of inventory management.

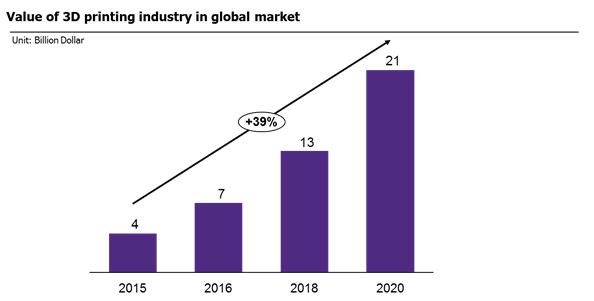

Today, 3D printing technology is widely used in various industries, particularly in the aviation industry. It is expected that in the future 3D printing will be introduced to a greater variety of factories and machinery. 3D printing is expected to grow five times between 2015 and 2020.

|

|

|

|

|

Figure 1: Cost of production lines for bioplastic is 30% higher than conventional plastic

Source: EIC analysis based on data from Project Mainstream analysis and expert interviews.

Figure 2: The proportion of bioplastic use will grow in the future, from less than 1% in 2013 to 4% in 2019 and 40% in 2030

Source: EIC analysis based on data from Grand View Research 2014, European and Bioplastic 2013, BCC Research 2014, Nexant Inc, 2012

Figure 3: Growth of 3D printing market, which is projected to expand by five times in 2020

Source: EIC analysis based on data from ‘The 3D boom continues’, Manufacturer’s Monthly, May 15, 2015