India’s GST, the biggest tax reform, opens new opportunities for Thai investors.

EIC Research Series: Opening doors to India

By: Yuwanee Ouinong

India is a country that brings to mind diversity and complexity in virtually all aspects. Its variety of culture, ways of living between social groups and large population size of over a billion has been key feature attracting the focus of investors all over the world. Yet doing business in India is no easy task. Trivial regulations and inconsistencies between states are only part of the problem that has led India’s to rank 130th in ease of doing business out of 190 countries. Until now, the current government under leadership of Prime Minister Narendra Modi is pursuing an ambitious economic reform in multiple areas. One of the top priorities is the biggest tax reform since the country’s independence in 1947. The new tax system called Goods and Services Tax (GST) is now rolling out across India.

Removing the complex tax system.

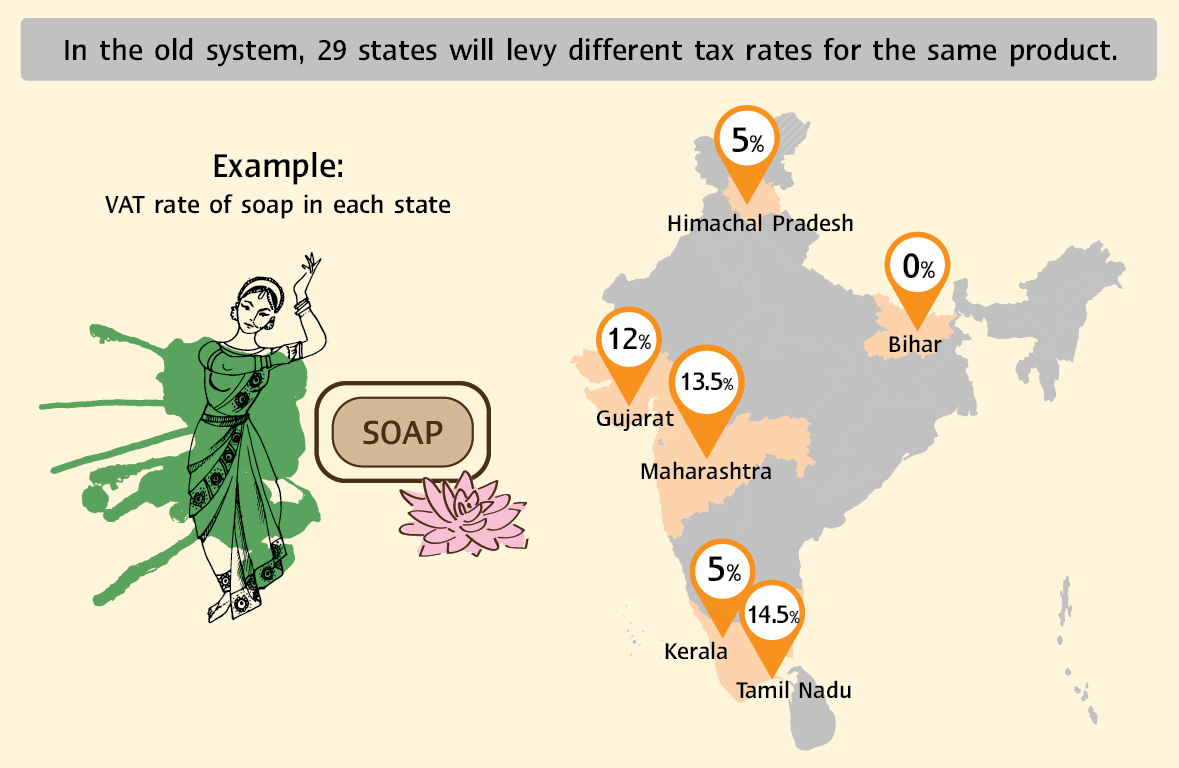

India, which is a large country, is administered under a decentralized system composing of one central government and 29 states. Each state would have their own administration and were previously allowed to levy different tax rates. As a result, India had among the most complex tax system in the world, of which has been deterring foreign investors from India.

Key obstacles for doing business arose from the old tax system are as follows.

1. Understanding the tax system is too time consuming. Those doing business have difficulty in assessing cost or profit in each state. Furthermore, as some states require border inspection and entry tax collection, careful planning in terms distribution and tax calculations is therefore essential. In fact, trading between states in India can be just as difficult as trading with 29 different countries.

2. Inspection is difficult due to having multiple tax collecting agencies. The central government’s tax agencies work separately with their state counterparts, therefore making it troublesome to examine redundancy of tax collection or recording of tax credits. Generally, manufacturers that have already paid tax on a purchase for raw materials should be able to subtract the amount off tax amount required on sale of final product, known as tax credit. However, given that the tax collection data are not consolidated between agencies, it would be difficult to determine whether a manufacturer have appropriately paid for their tax on raw materials.

3. Huge incentive to bribe officers. Officer discretion is needed in certain tax assessment procedures due to lack standard tax rate enforcement. Furthermore, under the old system officers need to manually examine documents as the system is not yet online.

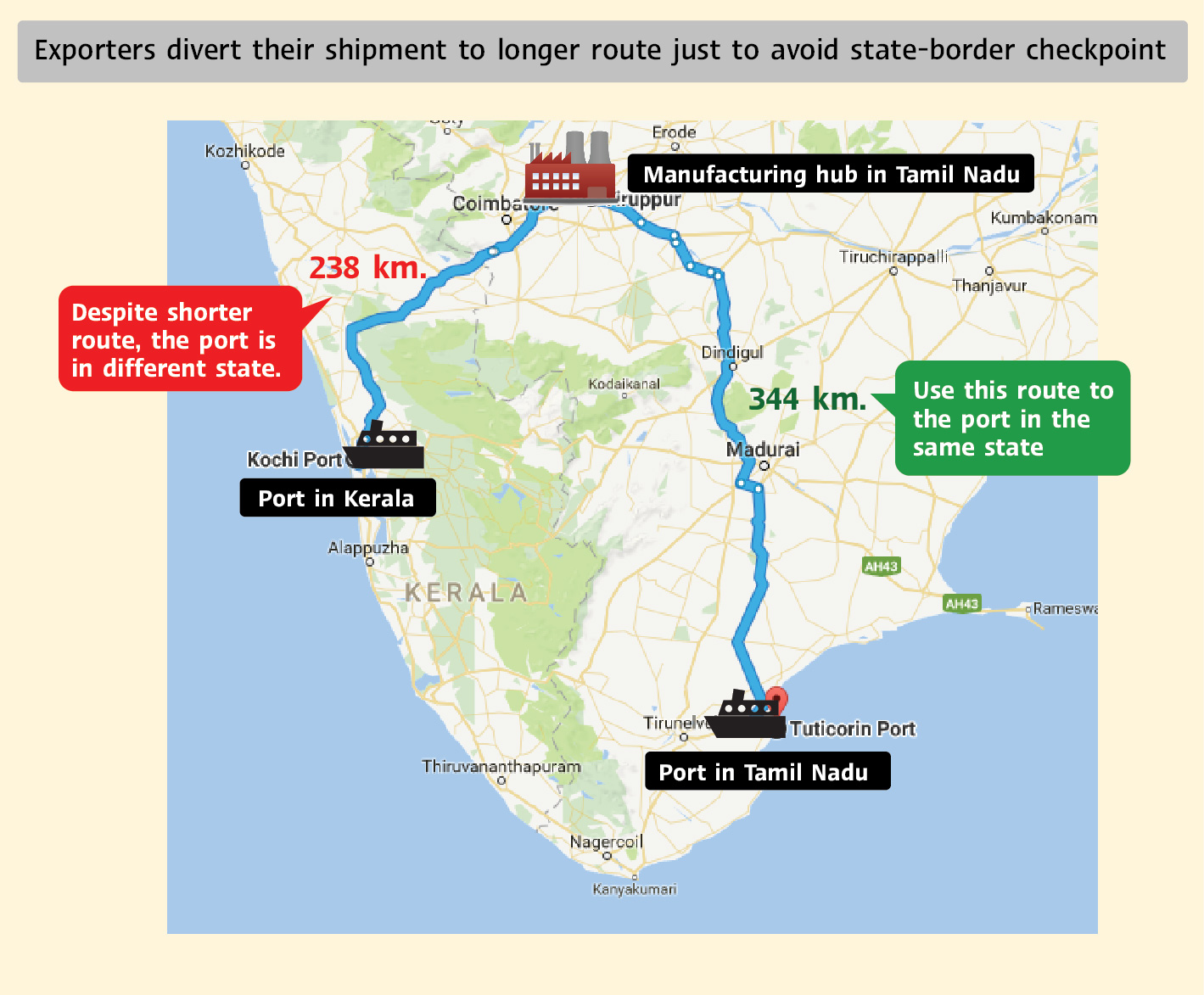

4. State-border trades have high cost in both terms of money and time. A World Bank report showed that for up to 60% of the time used in transporting goods within India, the truck is not moving at all. This is because trucks need to spend time at state-border checkpoints for tax assessment. Given such, businesses also have trouble approximating time of delivery.

5. Problems in exports and manufacturing, as manufacturers need to divert their shipments to avoid state-border checkpoint. For instance, an exporter in Tirupur, Tamil Nadu state would rather choose to transport its goods to a port within the same state than sending goods to a nearer port in Kerala state just to avoid crossing the border between Tamil Nadu and Kerala. Exporters in India have higher transportation cost than international standard by up to 2-3 folds. Moreover, in certain cases it is cheaper to import raw materials from overseas than buying them from another state. Such has led many firms in India to avoid using local material in their production.

Source: EIC analysis based on data from World bank, Apparel Resources, and Google maps.

The new, unified tax regime

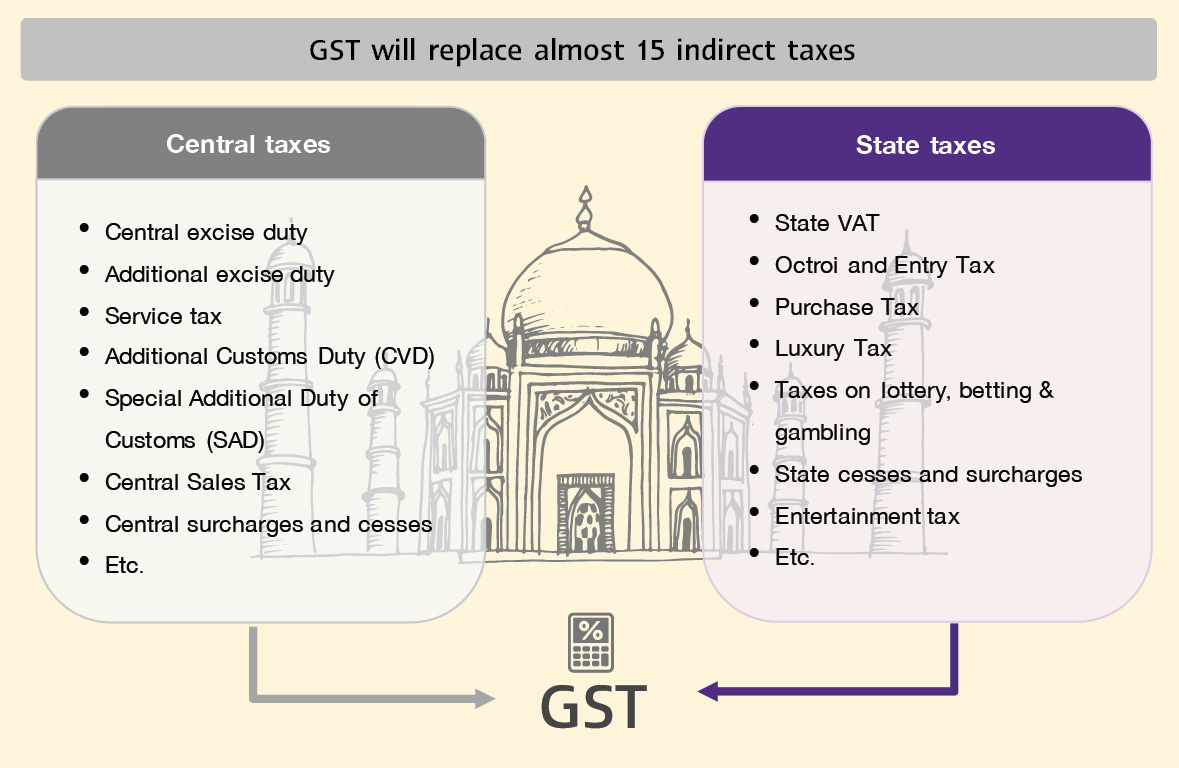

GST (Goods and Services Tax) is a system that will unify tax rate on goods and services within the country. The system is a change from the previous that allowed each state set their own tax rate. The new system would replace approximately 15 categories of indirect tax such as central sale tax, entry tax, Octori, VAT, Excise tax, etc. Each product will be imposed the same rate throughout the country. Furthermore, tax procedures will be required to conduct online in order to avoid contact between tax payers and government officers. For intra-state trading, tax on goods or services will be collected by between the state government (State GST: SGST) and central government (Central GST: CGST) equally. Therefore, assessment procedures is expected to be strictly complied on both governments. For inter-state trading, the tax, called integrated GST (IGST), will be levied solely by central government.

Source: EIC analysis based on data from thegstindia.com

EIC believes the most obvious gain from the transition towards the GST system is lower logistic cost and removing cascading tax effects. The GST system will transform India into a unified common market by eliminating various taxes in different states and allowing manufacturers to get full tax credits for input. Such would significantly lower tax burden and cost of production in India, and in turn raising consumption. The GST system will also improve ease doing of business, promote transparency and efficiency in tax collection, and quicken transportation of goods. The World Bank estimated that logistics cost in India could fall by 30-40% if transportation time is cut by half. Spillover benefits into other sectors include promotion of export and import sector, of which in the whole the government of India expects the GST to boost GDP by another 2%.

Source EIC analysis

Allowing to claim input tax credit credits will encourage more businesses to register for the new tax system. This is because businesses will be able to claim input tax credits only if they purchase from suppliers that are registered under the GST system. Therefore, producers will be less likely to buy inputs from unregistered suppliers. Moreover, unregistered producers who do not get tax credit will carry higher cost of inputs and thus have lower price competitiveness. Given such incentive to register, the government believes greater number registered businesses should be able to compensate for certain tax revenue that will be loss under the reform.

Although India’s GST is not actually ‘one nation, one tax, one rate’ as the government once said, the reform is a great step forward for India. The GST system consists of 4 tax rates, which are 5%, 12%, 18% and 28%. Commodities likes rice, grain or milk, however will be exempt from tax under the new system. Meanwhile, the highest tax rate of 28% will be imposed on luxury items such as air conditioner and movie tickets. Nevertheless, products such as petroleum and alcoholic drinks that are significant income source to the government will be excluded from the GST system. The general view is that a single tax rate would be difficult to impose as the same product as its necessity may vary depending on the group of people. Enforcing the same tax rate on each product throughout the country is already considered a significant achievement for the Indian economy.

It’s time for Thai investors to find opportunities in India.

Thai investors should turn their attention towards India as they are already steps behind foreign investors. Since the government under Modi’s administration began in 2014, firms all over the world saw the potential for growth and have since rushed for opportunities. The value of foreign investments has since been increasing at average rate 28%YOY with major investments coming from Singapore, Japan and the U.S.. On the contrary only 20 Thai companies1 currently have investments in India. Total investment value of Thai firms in India at the end of 2016 stood at USD 906 million, or only equates to 7.8% of the total investment of Thai firms in CLMV even though India has a population size 8 times greater than CLMV.

Thai businesses that have potential to benefit from this tax reform are businesses related to logistics and consumer goods.

1. Logistic businesses will have an obvious gain from this reform. Although currently several global logistics firms have already entered the Indian market, the majority of the market share is still accounted by local logistics companies1. The complexity of India’s tax system has been an important hurdle for foreign firms, leading local businesses to have the advantage. This tax reform will be key to unlocking the logistic sector in India. A summary of expected changes to the Indian market and significant opportunities for Thai investors are as follows.

- More logistic service outsourcing. Previously manufacturers would transport their own goods or hire local logistics firms as most delivery destinations are close by and within the same state. Even for inter-state transportation local firms still have an advantage over foreign firms as multiple inspection procedures at the border can be too burdensome for an outsider. The GST system would, however, remove this barrier, and in turn boosting trade between states and leading manufacturers distributing goods to various states. Manufacturers thus require more full-service logistics for both transportation and warehouse management. Furthermore, as the new system will allow for tax credit claim on services offered by firms under the system, thus manufacturers are likely to move away from local logistics firms that are not registered with GST. Given such, this presents an opportunity for foreign firms with logistics expertise to expand their market into India.

- Lower logistics cost. Manufacturers will need to spend less time and money on petrol when lining for cross border inspection. Furthermore, time of delivery can be more accurately forecasted.

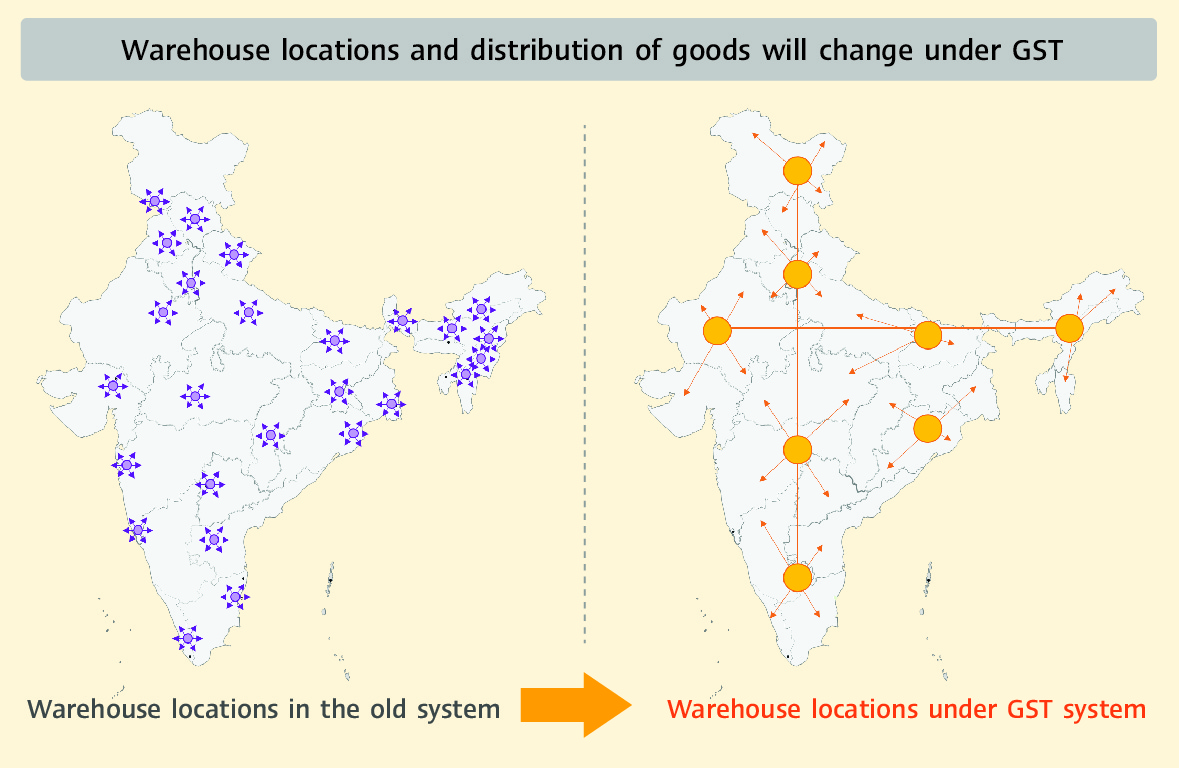

- Drawing up plans for warehouse construction and product distribution will be easier. Previously businesses built small warehouses in multiple states in order to be closer to point of distribution and to avoid cross-border tax. Such business model may have seem too troublesome for foreign firms. However, under the GST system businesses can invest in constructing a centralized warehouse and management technology that was previously deemed unsuitable for smaller warehouses. As a result, businesses will be able to reduce the number of warehouses by creating hub, whilst maintaining its distribution capacity within the country.

Source: EIC analysis

2. Consumer products business such as processed food, drinks, soap, shampoo, clothes and household products have immense growth potential given the size of consumer population in India. This business also stands to benefit clearly from this tax reform. The key impacts on this business group are as follows.

- More efficient distribution. Businesses related to consumer products require good distribution coverage of their end-user; therefore, lower logistic cost will thus obviously benefit this business group. In fact, once India becomes a single market, these businesses can build central warehouses to better manage stocks and move away from the previous model of having multiple small warehouses in various states, which was difficult to forecast demand and to manage inventory. From such factors, the GST system should in part support foreign firms to be able to compete with local firms.

- Several consumer products will be levied a lower tax rate than previously. Under the new system grains or milk, which were previously being charged a tax rate of 5%, will now be exempted from tax. As for soap and toothpaste, they will be subject to a tax rate of 18%, which is lower from its previously level of 22-24%. The new tax system will therefore cut prices of a range of consumer products and in turn encourage more household spending on these goods.

- Processed food and beverage is a product that Thai businesses have expertise making it a potential product for Thai businesses. Although several large foreign companies have already entered the Indian market, there is still a window of opportunity given its large and fast growing consumer market and that up to 50% of the market share of the processed food market is currently occupied by small, local players1. The new GST system will ease entry of Thai business to into the market, allowing them to distribute products to various cities in India as a trial run, for instance. Thai firms may previously had been at a disadvantage compared to local firms as expensive logistic cost may have caused Thai imports to cost more than local products. Moreover, Thai firms did not have as good an understanding of the different regulations in each local state as their local competitors. This caused Thai firms deciding to invest in a manufacturing plant in India to struggle in finding optimal location taking in to account cost in distributing products to various cities. Under the new GST system such obstacles are now removed and therefore bringing about new opportunities to Thai firms.

- It is necessary to adjust products to fit with Indian consumer preference, a requirement Thai firms can easily meet. Dutchmill, for instance, is a Thai firms that has for some time entered the Indian market and has been working with local firms in building a manufacturing plant. The company launched a new yoghurt drink brand called “Mista Twista”, factoring in local language and culture in the name. The taste was also adjusted by lowering sourness that is more preferred by the local consumers. When Charoen Pokphand opened its Five Star Chicken branch in India, the company added fried chicken masala to its menu and advertised in Bollywood-style MVs to build its presence among the younger Indian consumer group. Srithai also changed its design to better meet with the local preferences and was well received, becoming a popular household item among Indian families4. Furthermore, ethnic food preferences of Thais and Indians are similar therefore adjusting recipes is easily achieved. Products made from beans and snacks, herbal products, dried fruits, frozen food and spices are some example products that can exported to India. Also many Thai firms are already compliant to Halal standards. Although many of the aforementioned products are already being exported to India, their share only account for less than 1% of Thailand’s food exports.

Undeniably, India will become a key driver of global growth in the decades to come. Business involved with logistics and consumer products are mere examples of businesses that can profit from this tax reform in India. Thus, other business groups should also keep close watch for opportunities in India. It is now the time Thai investors need to build a better understanding of this market so to not miss timely opportunities for investment.

1 Data from the Royal Thai Embassy, New Delhi, Republic of India

2 Mitra S. (2008), Logistics Industry: Global and Indian Perspectives.

3 Data from the India Brand Equity Foundation (IBEF)

4 Data from Thai-India Business Information Center, Royal Thai Embassy, New Delhi, Republic of India and Prachachat.