Robo advisors, the business opportunity that will transform the financial sector

- Robo advisors are Fintech applications designed to provide personal wealth management services online to general investors. Their selling point is their low cost as well as their capacity to develop into a provider of more comprehensive services similar to those offered by financial institutions. - EIC see Robo advisors as an opportunity for financial institutions to enhance the quality of their personal wealth management services. This technology will improve service efficiency, which in turn will help financial institutions maintain and expand market share.

Author: Sirada Siribenchapruek

|

Highlight

|

Robo advisors offer personal investment advice to ordinary investors by combining investment management, financial advisory and financial planning into a single wealth management service package. Such services previously targeted high net worth customers, making access difficult for those of more modest means. To cater to this under-served market, start-up businesses began developing robotic technology that used algorithms, big data management, and artificial intelligence integrated with financial advisory to formulate financial investment plans. These types of innovations in personal financial advisory are known as Robo advisors.

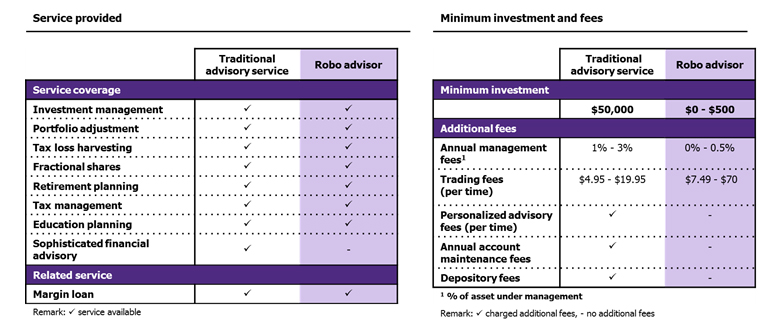

Robo advisors, which will tap the majority of diversified investors, are a Fintech closely watched by the finance industry around the world. Robo advisors were developed to replace face-to-face advisory in order to lower investment and wealth management advisory services costs for ordinary investors. The investment advice they provide is formulated on; 1) investment objectives, such as financial retirement planning or investment to raise wealth, and 2) investor risk appetites. Additionally, Robo advisors can adjust portfolios automatically to mitigate risk as well as provide other more comprehensive service functions such as tax loss harvesting, trading of fraction shares and margin loans to customers in the US (Figure 1). More premium services are also being provided by firms like Betterment and Schwab IP, offering personal investment advisory targeting high net worth individuals wanting to use this technology.

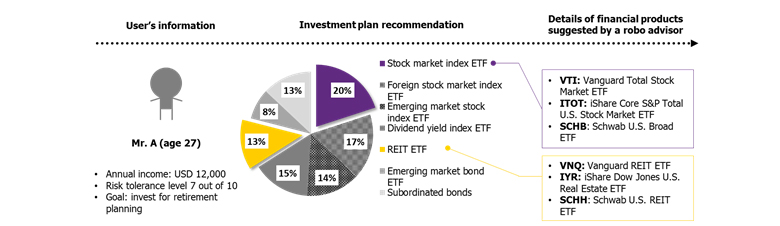

There are three key factors driving the widespread success of Robo advisors overseas. 1) Smaller initial investment requirement. Most investors previously did not have access to traditional advisory due a minimum investment barrier requiring 50,000 US dollars or more. However, some Robo advisor services, such as those provided by Betterment and Acom, have no set minimum balance. 2) Cheaper annual service fees. Robo advisors bring the average charge down to 0.0.5% of the asset under management compared to traditional service providers that charge a fee of 1-3% with other add-ons (Figure 1). 3) Investment advice can be accessed efficiently and personally online (Figure 2). In fact, Robo advisor providers like Wealthfront and Asset builder recommend a specific investment proportion of various financial products (Figure 3), factors that have led Robo advisors to becoming a prevalent solution in financial advisory to investors abroad.

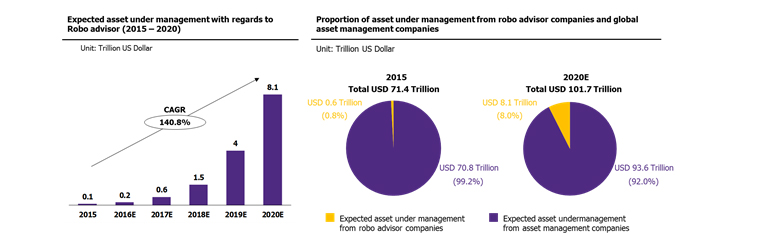

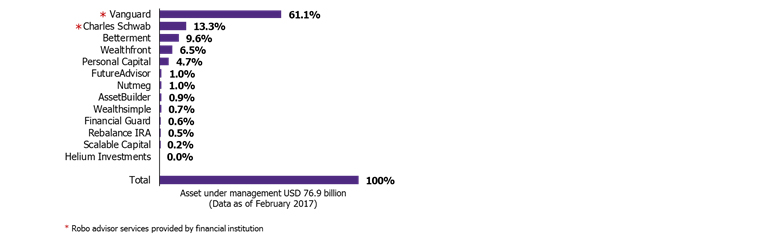

Large financial institutions in the global market will maintain their major holding of the investment and wealth management advisory market share despite an expanding market for Robo advisors among startup businesses. Business Insider Intelligence, a business research unit, estimates that the value of Robo advisor businesses around the world will grow to 8 trillion US dollar by the year 2020, equivalent to 8% of the value of assets under management by financial institutions around the world (Figure 4). This shows that Robo advisors will have greater influence over the financial sector going forward. The top two leaders in Robo advisory, Vanguard PA and Charles Schwab, account for 74% of total assets under management among the top 10 firms (Figure 5), demonstrating that Robo advisors rely on firms that have the substantial capital necessary to develop the technology, a large customer base, a good reputation, and offering access to a broad selection of investment products.

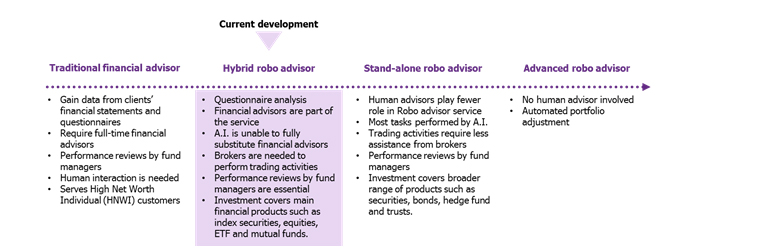

Although Robo advisors are currently still under development, their service quality can be improved with the collaboration of involved businesses. Robo advisors manage a large pool of information and process data from multiple sources simultaneously in order to configure optimal investment choices. Nevertheless, Robo advisors still depend on human intervention, such as when trading financial assets that need to go through an agent, fund manager assessment of system performance (Figure 7), or when providing analysis and providing investment advice in complicated scenarios involving financial status, employment, and financial stability. Furthermore, given their limitation in helping firms build personal relationships with clients, which requires psychological and persuasive skills, Robo advisors should be used in conjunction with investment advisors or businesses related to wealth management and investment advisory to improve service quality.

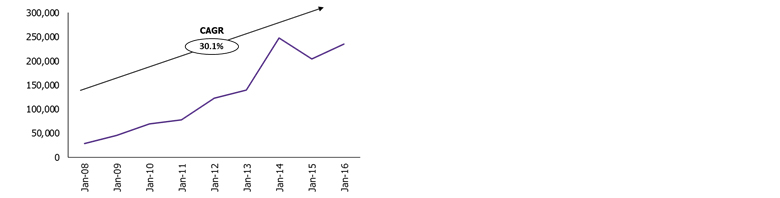

General investors in Thailand are keen to invest with Robo advisors. Individual investors are more likely to rely on online services for their investment transactions going forward, in particular the online trading of assets, which has already risen by 30% (Figure 6). A survey by management consulting firm Accenture found that up to 94% of Thais surveyed are using online banking and are ready to use a Robo advisor to manage their investments. However, the technology is still largely unknown or is still limited to high net worth individuals.

Robo advisor providers in Thailand will need to pass the regulatory sandbox before starting business. Financial institutions and Fintech start-ups registered in Thailand will need to pass the financial innovation safety test of the Bank of Thailand starting from the first quarter in 2017, for a duration of one year. The safety framework not only supports financial innovations and helps form an understanding of their impact on the country's financial sector, it also ensures safety to users by allowing time for investors to learn about new financial service technology like Robo advisors before using the service.

1 Tax loss harvesting implies selling securities that has experienced losses to offset taxes on capital gains at the end of the year

2 Fractional shares is the practice of purchasing less than full shares from companies that have high price per share.

|

|

|

|

|

Figure 1: Comparison of provided services and fees between traditional advisory services and Robo Advisor.

Source: EIC analysis based on data from Investment Zen, Advisory HQ, Investopedia, Value Penguin, Money Smart and Business Insider.

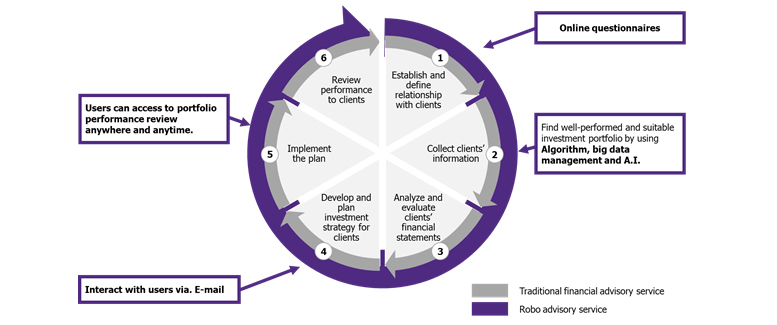

Figure 2: Comparison of the processes involved in providing investment advisory between traditional advisory services and Robo Advisors.

Source: EIC analysis based on data from FSB, Investment Zen, and Investor Junkie

Figure 3: An example of an investment plan recommended by a Robo advisor.

Source: EIC analysis based on data from Wealthfront.

Figure 4: Estimated value of assets under management of firms providing Robo advisors and financial institutions around the world.

Source: EIC analysis based on data from Business Intelligence and PWC asset management 2020.

Figure 5: Top 10 providers of Robo advisors in the World (as of February,2017)

Unit: % of total asset under management

Source: EIC analysis based on data from Statista.

Figure 6: Number of online asset trading accounts in Thailand.

Unit: accounts

Source: EIC analysis based on data from Stock Exchange of Thailand.

Figure 7: Development of Robo advisors

Source: EIC analysis based on data from Accenture and Deloitte.