Readiness check for car sharing businesses

Car sharing businesses provide short-term car rental services and have been growing globally at more than 39% per year. The strength of car-sharing services is their ability to fill in the gaps between public transportation networks in densely populated cities with extensive public parking facilities. The nature of car sharing is compatible with the lifestyles of Gen Y, a generation that will become major buyers in the future and that uses more public transportation than previous population cohorts. However, unlike in Europe and the US, car-sharing services in Thailand have a disadvantage in price competition compared to other travel options

Author: Nantapong Pantaweesak

|

Highlight

|

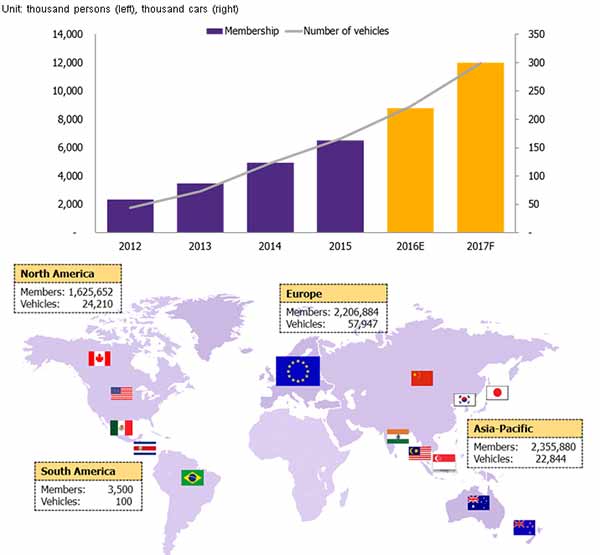

Car-sharing businesses that provide short-term car rental services have experienced continuous growth worldwide. The annual growth of the business-to-consumer type services is 39%. The objective of car sharing is to reduce the number of cars on the road. There are two types of car-sharing services: peer-to-peer (P2P) services and business-to-consumer (B2C) services. P2P services take advantage of the fact that cars are usually parked more than 80% of the day by matching car owners looking for additional income with members looking to rent a car during the same period. Developed after the P2P type is the B2C type of car sharing. B2C services provide short-term car rental services without requiring their members to own a car. The competitive advantage of the B2C business model is its ability to provide one-way-trip services, thanks to multiple parking spots that allow members to rent cars at convenient locations without needing to return the car to the same spot. Currently, the number of those engaging in car-sharing worldwide numbers about 6 million and is expected to increase to 26 million by 2020. Asia Pacific has the most car-sharing members at 2.3 million and enjoyed high annual growth of 65% between 2012-2015. Europe has the second highest number of car-sharing members at 2.2 million persons, while North America follows with 1.6 million members. The number of vehicles in car-sharing services have reached about 100,000 cars. Countries such as Australia and Singapore have adopted national car-sharing projects to help reduce CO2 emissions. Singapore even encourages bringing electric vehicles into car-sharing services.

Countries experiencing substantial growth in car-sharing services have four similar characteristics; 1) High population density is an important factor in a car-sharing project’s worthiness. Areas with low population density usually have weak investment in public transportation systems as residents still enjoy a high level of convenience using personal cars. EIC estimates that the population density appropriate for car sharing should be more than 500 people per square kilometer. Currently, central Bangkok has a population density of more than 3,000 people per square kilometer and its metropolitan area has a density of more than 1,000 people per square kilometer. 2) Extensive public transportation coverage helps reduce the need for personal cars. If a personal car is needed it is only to travel to or from public transportation access points for short periods of around 10-15 minutes. 3) Environmental-friendly policies and campaigns from both the public and private sectors target the reduction of CO2 emissions from land transportation, involving both the supply and demand sides of public transportation. And 4) Public parking spaces dispersed in many areas help provide parking spaces for car sharing, especially if the government assigns spots specifically for car-sharing vehicles.

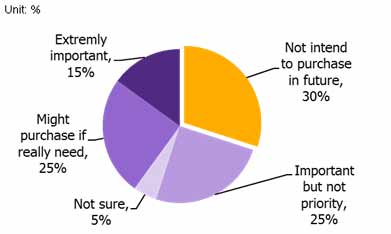

More Gen Y members in big cities are turning to public transportation and using fewer personal cars. Surveys show that only 15% of Gen Y members, a generation which comprises of 40% of the US population in 2015, see personal cars as a necessity. This correlates with Gen Y members purchasing only 50 cars per 1,000 persons compared to Gen X and Baby Boomers who buy 80 cars per 1,000 persons. In Bangkok, Gen Y makes up 30% of the population, and they have grown up at a time when public transportation like the BTS and the MRT are available (the BTS was opened in 1999 and the MRT in 2004) along with other transportation options like the ride hailing services that entered the market in 2015.

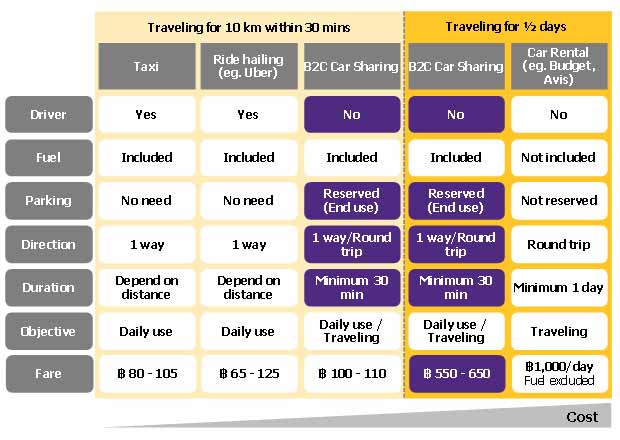

However, car sharing in Thailand has limitations, including insufficient public transportation coverage, scarce parking spots, and its inability to answer to the needs of Thai consumers In Thailand, high population density and extensive public transportation are still limited to big cities like Bangkok and its metropolitan areas. Such public transportation systems include rail transportation like the BTS, MRT, and express boats on the Saen Saep canal and the Chao Phraya river, and buses. Although prevalent, these public transportation networks do not cover every area of the city and are not well-connected enough for consumers to consider reducing their use of personal cars. In addition, there are insufficient parking spots in Bangkok, especially park-and-ride spaces, and they have not spread into suburban areas. Moreover, there are no designated public parking spaces in populated or commercial areas. This shortcoming thus deters B2C car-sharing businesses from providing the one-way rental services that are its business strength. When considering the aspect of last mile transportation, we found that options such as taxis, motorcycle taxis, and ride hailing services are currently more competitive due to higher flexibility in both the processes of acquiring a ride and parking since the services come with a driver. In addition, the fees for these options can be as low as THB 30 when traveling less than 10 kilometers. Another factor working against car-sharing businesses are two types of fees that could be unfamiliar to Thai customers used to only the pay-per-usage model: monthly membership fees and pay-per-usage fees. For example, in the digital music industry that provide the customers as both pay-per-song music download and music streaming services with monthly fees, we found that music streaming businesses could captured only 2% of the digital song market in 2015.

The government’s taxi price regulation works against car-sharing businesses and is not conducive to competition in the transportation market, contrary to countries with strong car-sharing businesses as in Europe and the US. A car-sharing business offering car-rental services does not involve the use of private cars to transport passengers in return for a fee and thus is not against the Vehicle Act 1. However, when competing with other transportation options like taxis having their fees controlled by the Ministry of Transport, car-sharing fees for traveling less than 10 kilometers and within 30 minutes are THB 10-20 higher than those of taxis. In Europe and the US taxi fees are much higher. Their governments provide incentives for people to use car-sharing services instead of personal cars to support their environmental policy goals. For example, in the US the state of Washington gives tax reductions of USD 60 per person per year to organizations that encourage their employees to travel to work by car sharing or other types of public transportation. In Italy, there is a policy scheme to reduce the number of personal cars that exempts car-sharing membership fees in the first year and offers a 50% discount in the second year. The UK and German governments provide special public parking spaces or parking fee discounts for car-sharing vehicles.

1 The Vehicle Act B.E. 2522 (1979) defines a “service vehicle for rent” as a vehicle provided for rent, but while rented not to be employed in transporting passengers or goods.

|

|

|

|

|

Figure 1: Numbers of B2C car-sharing members and vehicles in service during 2012-2015

Source: EIC analysis based on data from the Car sharing Association and TSRC

Figure 2: Survey results on the importance of owning a car perceived by Gen Y members in the US

Source: Goldman Sachs

Figure 3: Cost comparison between car sharing and alternatives

Source: EIC analysis based on data from the Department of Land Transport, Uber, Haupcar, and Budget

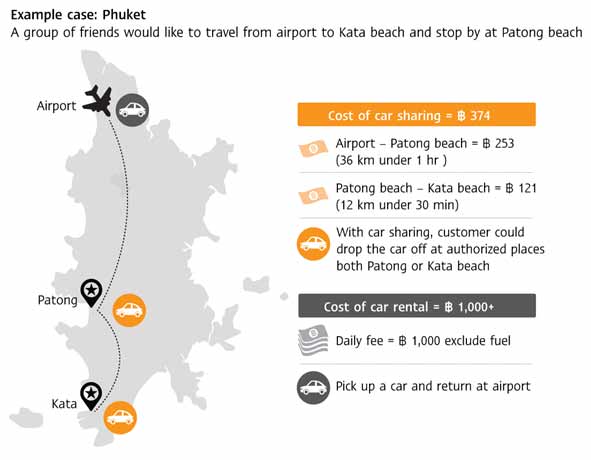

Figure 4: Bringing car-sharing services to support the tourism sector

Source: EIC analysis based on data from Haupcar and Budget