Rising opportunities for service stations from tumbling oil prices

Lowered global crude oil prices boost demand for oil and marketing margins from retail sales. Government policy has also eased inventory costs for business operators. Service stations are back in the spotlight as existing operators expand and new operators enter the marketplace. Fierce competition is forcing service station operators to rethink their strategies. EIC sees key success factors in this business as cost management, integration of oil and non-oil services, suitable business models and locations, and branding. Moreover, businesses should closely follow changes in government policy, movements in global oil prices, and changing consumer behavior, to quickly adapt to new dynamics and maintain their advantages over other players.

Author: Lertpong Larpchevasit

|

Highlight

|

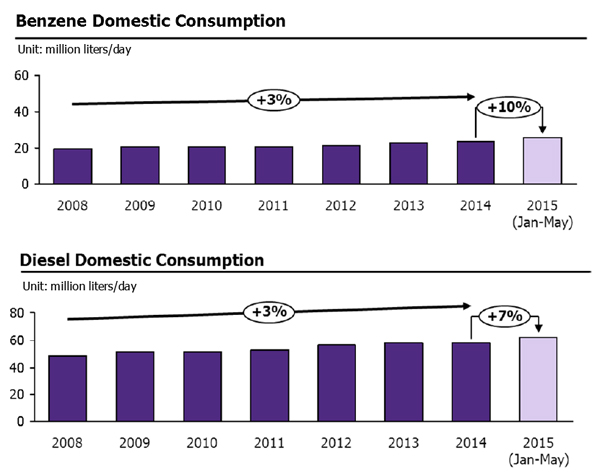

The drop in domestic retail prices of benzene and diesel following the slide in global crude oil prices has led to higher fuel demand. Global crude prices have dropped by more than 50% since the second half of 2014. Prices presently fluctuate around a band of 40 to 50 USD per barrel. As a result, domestic benzene and diesel retail prices have moved downward by an average of 30% and 23%, respectively, from the same time last year. The drop in retail prices sent daily demand for benzene and diesel in the first half of 2015 higher by 10% YOY and 7% YOY respectively in comparison to 2014. Public sector investment in road and rail infrastructure will also further spur fuel demand in the future.

The government policy to lower gasoline reserve levels has also reduced costs for service stations. The government lowered the required level of reserved gasoline from 6% to 1% (or from 21 to 4 days) as large reserves are no longer needed at the time when global crude supply exceeds demand, leaving crude oil available in cheap abundance. As a result, service station operators will benefit from lower inventory cost, thus increasing liquidity and business expansion opportunities and attracting more investment in service stations.

Service stations are once again an attractive investment opportunity offering higher revenues and profits. In the past 2-3 years, service stations only posted marketing margins of 1-1.5 baht per liter, or about 3-4% of retail prices, amid high investment cost and fierce competition from both domestic and foreign players. Steep global crude prices that surpassed USD100 per barrel also led to higher retail gas prices and slow demand growth. This drove Petronas, a leading Malaysian oil company, to sell its business to SUSCO citing unattractive return on investment. Now, however, plummeting oil prices drove gas prices at refineries down while retail prices move downward more slowly, thus lifting marketing margins higher to 2.5 to 3 baht per liter (or 8% of retail prices). Coupled with lower oil fund contribution requirements, the current situation has increased return prospects for service stations and made them a more attractive business proposition.

Nevertheless, high competition in terms of prices and services will force service station operators to focus on cost management as a key success factor. Not only do service stations offer similar products, but many of them are also located in proximity to one another hoping to service the same demand group. Therefore, cost management to keep expenses down will enhance efficiency and increase profits. Effective supply chain management is one method to help keep costs down and at the same time enhance efficiency. For instance, logistics and inventory management will reduce expenses on transport as well as control fuel shipment times.

Incorporating non-oil business into service stations will boost profit margins while maintaining oil services as a primary business to generate cash flows and attract customers. Operating auxiliary retail or automotive service businesses will increase profit margins as well as utilize service station space to its fullest. Owners can consider partnering with a leading retail company to generate income from rent, or develop their own retail services. One-stop service stations combining oil and non-oil businesses are also becoming a trend, boosting profit margins by increasing the proportion of income from non-oil businesses. Potential non-oil businesses include retail sales, automotive services, restaurants, coffee shops, and banking. In the future, gas stations could even become small community malls. Non-oil businesses could bring profit margins as high as 30-50% in rental income, while owner-operated retail operations could bring 10% in profit margins.

Choosing the right business model for sustainable expansion is also an important strategy. In Thailand, management of gas stations usually falls under the Company Owned Company Operated (COCO) or Dealer Owned Dealer Operated (DODO) models. COCO is when the owner is also in charge of running the station. This is suitable for small to medium businesses with a small number of stations to which similar quality controls and business plans can be easily applied. For this model, entrepreneurs must bear all investment and management risks as they expand their business. Without a recognized brand, businesses may be disadvantaged. On the other hand, DODO is a franchise right given to small entrepreneurs or “dealers” to manage stations under the owner’s brand and purchase fuel only from the franchise owner. This model suits those with a well-known brand wishing to rapidly expand at a low investment cost. Franchise owners thus realize income from franchise rights and wholesale margins from selling fuel to station operators. There are risks associated with quality control that may hamper brand credibility. Other less popular business models are Company Owned Dealer Operated (CODO), JV, and CO-OP. A CODO operation is when the main operator owns gas stations managed by small operators. This often occurs when one brand acquires stations from another. JV are joint ventures with at least two main operators. CO-OP are co-operative service stations in community areas.

Location and brand building are key selling points that must not be forgotten. Service stations located in a capital or large city and on major inter-city roads should benefit from higher demand and should be able to easily add value to their stations with non-oil services. On the other hand, to avoid competition with large operators, small- and medium-sized operators can focus on smaller cities and minor inter-city roads. They should also emphasize diesel to serve large passenger buses, trucks, and vehicles used in agriculture, whereas non-oil services can be downplayed. Branding also plays an important role in directly attracting customers. Brand building can be based on technology that improves gasoline efficiency and promote longer vehicle usage due to increased engine longevity. Brand building can also be based on attractive promotional offers that meet customer needs. For example, for service stations up-country, membership points to gain entry to lucky draws for gold or electrical appliances can be attractive, while for big cities, promotions can instead be linked to credit cards, such as offering cash back.

|

|

|

|

|

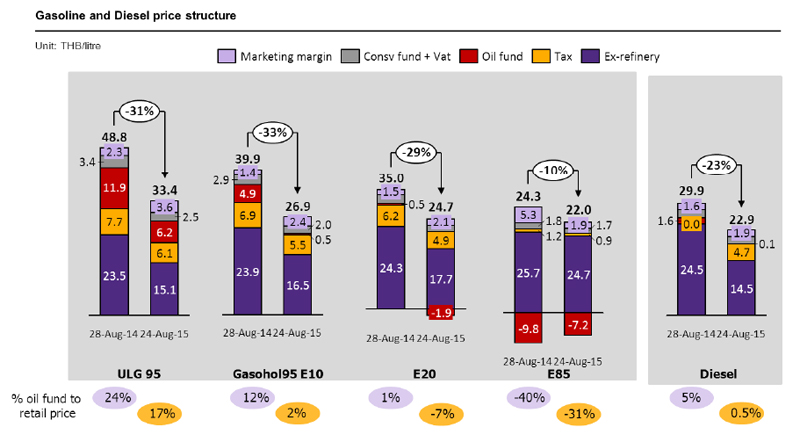

Figure 1: Retail benzene and diesel prices have fallen 25-30% compared to the same time last year following tumbling global crude oil prices.

Source: EIC analysis based on data from EPPO

Figure 2: Domestic consumption of benzene and diesel has clearly increased in comparison to the past 5 years following tumbling global crude oil prices.

Source: EIC analysis based on data from EPPO

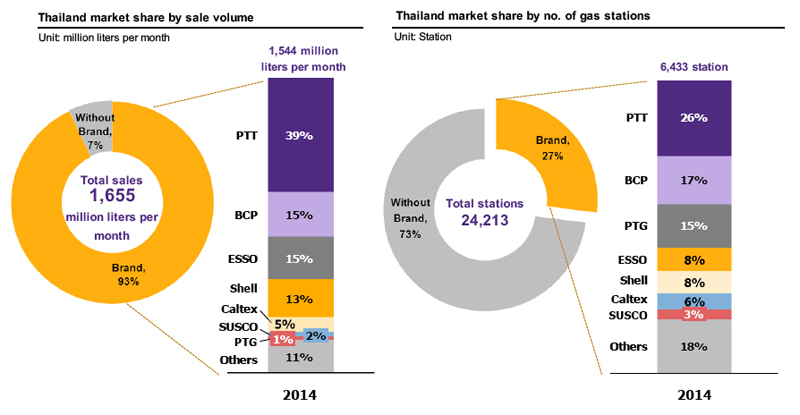

Figure 3: Business operators with their own brands outsell independent operators despite comprising a smaller share of total gas service stations (27%).

Source: EIC analysis based on data from DOEB