Automotive parts manufacturers gearing up to become global leaders

Automotive parts manufacturers will need to rethink business strategies and consider expanding their customer base to prepare for changing trends in the global automotive industry. Despite contributions from exports, the domestic car industry has yet to recover. The future of this industry will therefore depend heavily on decisions by global car manufacturers regarding where to base production. Thai auto parts manufacturers should focus on the major markets in China, Vietnam, Mexico, Poland, the Czech Republic, Columbia, Israel, Egypt, Bahrain, Kuwait, the U.S., the U.K., and Spain. These markets are sufficiently large, and their demand for cars and car parts is fast expanding. It will be beneficial for Thai firms to focus on improving product technology in order to compete successfully in these markets, which are dominated by top-tier auto-parts suppliers.

Author: Kaweepol Panpheng

|

Highlight

|

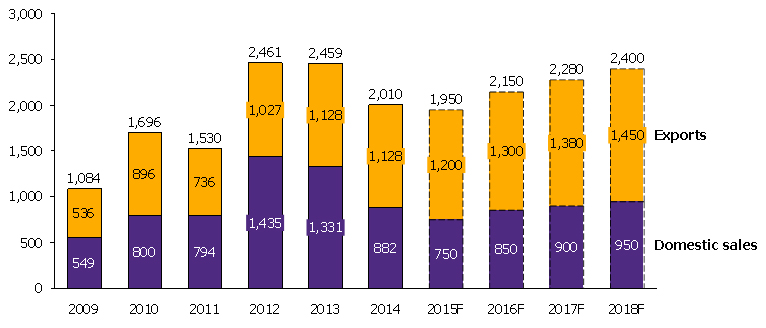

Despite contributions from exports, Thailand’s automotive industry remains subdued as a result of a sluggish domestic economy and adjustments following the First Car tax rebate policy. EIC forecasts that domestic car production in 2015 will total 1.95 million units (Figure 1), of which 750,000 will be sold domestically and 1.2 million exported. In addition, the domestic market for cars is expected to stagnate until 2016 due to persistent headwinds diminishing consumer purchasing power. Among such factors are high levels of household debt and depressed agricultural prices.

The decisions of global car manufacturers regarding where to base their production are key growth determinants for the domestic automotive industry. Yet another challenge for Thai firms is the small domestic market.Car manufacturers’ decisions on where to base their production are outside the control of Thai auto-parts manufacturers. Competing with Thailand are countries such as Indonesia and Turkey, both of which aspire to become major car manufacturing bases following Thailand’s example. These countries can appear more attractive, since the Thai domestic market is small relative to those in China, Brazil, India, or Indonesia. Moreover, the Vehicle Ownership Ratio suggests that Thailand's demand for cars is halfway to saturation. In developed countries the demand for cars is expanding by only 1-3% annually, with a vehicle ownership ratio of 450 cars per 1000 people. In Thailand the ratio is 240 cars per 1,000 people, suggesting that the market will soon approach saturation. As a result the 15-25% annual growth that Thailand enjoyed in the past will be difficult to attain, and the automotive industry will have to depend increasingly on exports.

Given the outlook for the Thai automotive industry, what is the way forward for auto-parts manufacturers? The answer is to consider exporting in addition to the usual OEM business. Currently, the auto-parts industry merely exports 15% of production. But as the domestic automotive industry continues to stall, auto-parts suppliers should steer more towards exports and rely less on supplying the OEM1 market. Such a strategy will help diversify risks and expand their customer base.

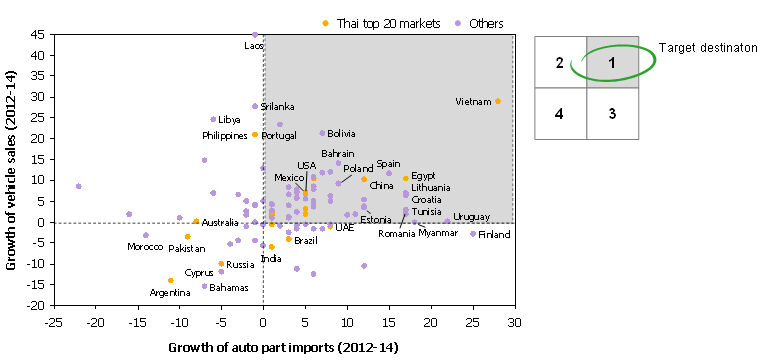

Amidst changing trends in the automotive industry, Thai auto-parts suppliers should rethink their business strategies in order to achieve sustainable growth. EIC categorizes automotive industries in countries around the world into four groups according to growth and demand for auto-parts import (Figure 2). (1) The automotive industry is expanding and demand for auto-parts imports is growing. Countries in this group are characterized by relatively large domestic markets for cars and some existing relationships with Thai auto-parts suppliers. This category includes China, Vietnam, Mexico, Poland, the Czech Republic, Columbia, Israel, Egypt, Bahrain, Kuwait, the United States, the United Kingdom, and Spain. (2) The automotive industry is expanding but demand for auto-parts import is ebbing. This group includes Indonesia and the Philippines, which are themselves developing auto-parts industries and thus rely less on imports. (3) The automotive industry is slowing down but demand for auto-parts import is expanding. This group includes Italy, France, and Germany, which have large markets for cars and depend heavily on imports of car parts due to high domestic labor costs. (4) Both the automotive industry and demand for auto-parts import are slowing down. This final group includes countries such as Russia, Argentina, and Pakistan, where economic problems in those countries have dampened demand for cars, as well as imports of auto-parts. Provided with such a landscape, Thai suppliers should focus on exporting to countries in group (1), with growing automotive industries and demand for auto-parts imports. Interestingly, the group currently accounts for only 40% of Thai auto-parts export , suggesting there is plenty more room for expansion to ensure a sustainable future for the industry (Figure 2).

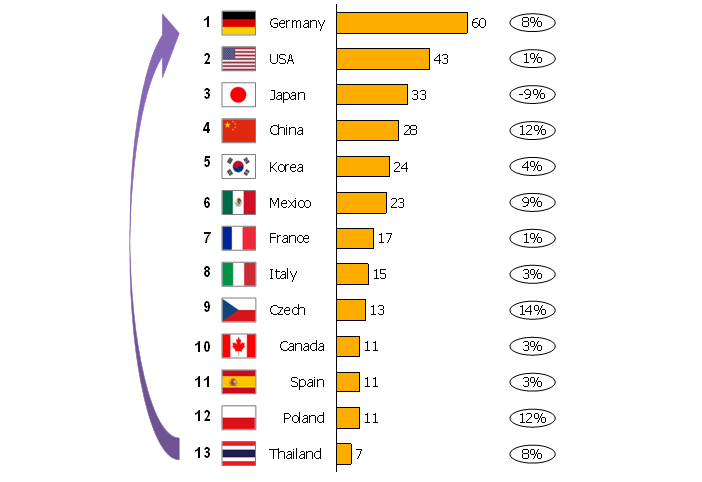

But to enter into target export destinations, Thai suppliers need to upgrade their technological capacities. As these target destinations mainly import auto-parts from developed economies such as the United States, Japan, the United Kingdom, and Germany, improvements in product quality will prove highly critical and formidable steps in positioning Thailand at the forefront of the global auto-parts industry. This is especially true considering that Thailand is now ranked 13th among exporters of auto-parts (Figure 3).

1 Original Equipment Manufacturer (OEM) are supplying auto parts directly to car manufacturers.

|

|

|

|

|

Figure 1: Automotive production in Thailand increasingly depends on exports.

Unit: ‘000 ton

Source: Analysis by EIC with data from Automotive Intelligence Unit

Figure 2: Characterization of potential export destinations by growth of domestic auto markets and demand for imports of car parts.

Source: EIC analysis based on data from Trademap and OICA

Figure 3: Top Global auto part exporters in 2014

Unit: Mn USD

Source: Analysis by EIC with data from Trademap.