MPC Holds Policy Rate as Expected, Upgrades Economic Outlook, Sees Inflation Outlook Largely Unchanged

SCB EIC expects the MPC to hold the policy rate at 1.0% through the rest of this year.

Key summary

|

The MPC unanimously voted 7–0 to maintain the policy rate at 1.0%, judging it sufficiently accommodative given for Thailand’s slow and uneven growth. Retail loan growth remains subdued, while SME lending continues to contract. The MPC expects headline inflation to decline in 2027 as supply-side pressures, particularly from energy and raw food prices, gradually ease. Looking ahead, the MPC will closely monitor firms’ cost pass-through, medium-term inflation expectations, and debt serviceability among SMEs and vulnerable households.

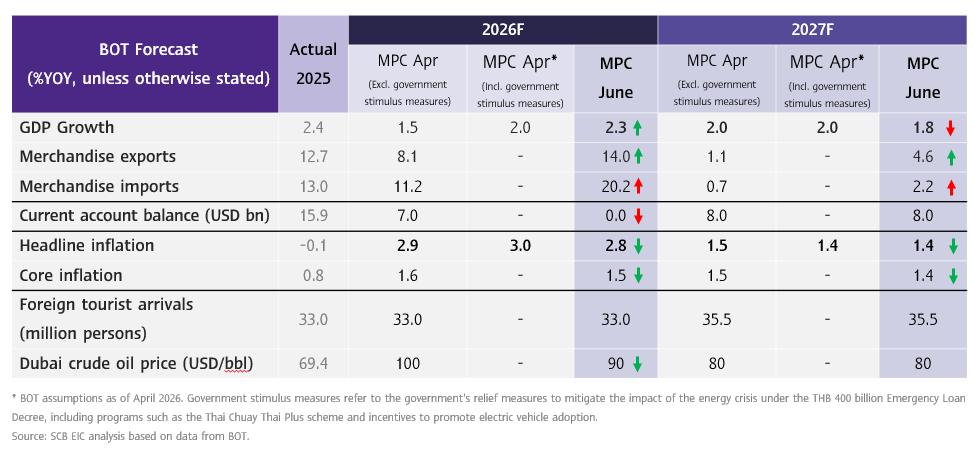

Figure 1: BOT's Thai Economic Outlook (as of June 2026)

Thai GDP growth outlook revised up from the previous meeting.

- The MPC revised up its 2026 GDP forecast to 2.3%YOY from 1.5%YOY (excluding government stimulus measures) and 2.0%YOY (including government stimulus measures), driven by:

- Tech & AI cycle momentum, export and investment momentum tied to the Tech & AI cycle has been stronger than expected, concentrated in tech-related exports and digital-sector investment.

- Milder war impact, war-related disruption has been less severe than expected as large firms have adapted by diversifying sourcing and shipping routes, while government subsidies have helped alleviate energy cost pressures.

- Government measures to mitigate the impact of the energy crisis under the THB 400 billion Emergency Loan Decree.

- The MPC continues to expect growth to stay below its potential and uneven in both 2026 and 2027. Household purchasing power remains squeezed by high cost of living and slowing income growth, while SMEs continue to face difficulties in adjusting to higher costs and have limited access to credit.

- The MPC revised down its current account balance forecast in 2026 to balance (USD 0 bn, from USD 7 bn). It expects the current account to record a deficit in Q2 due to temporary factors, including the sharp rise in crude oil prices and seasonal profit repatriation by multinational companies. However, the MPC expects the current account balance to gradually improve and return to surplus in H2/2026 and 2027.

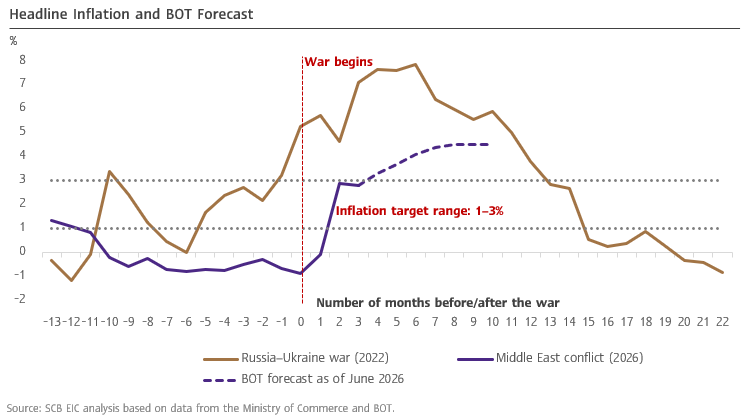

Figure 2: BOT Projects Thai Inflation to Remain Well Below 2022 Levels This Year

Inflation to rise in H2 before gradually easing back into the target range next year.

- The MPC trimmed its 2026 average headline inflation forecast slightly to 2.8% (from 2.9%). Monthly inflation should rise from 2.8% in May to a 2026 peak of 4.5% in Q4, temporarily exceeding the target range, as firms pass through costs and raw food prices rise from the impact of Super El Niño in H2. Inflation is expected to gradually return within the target range in 2027, with the MPC projecting average inflation at 1.4% (from 1.5% previously).

- Thailand’s inflation is expected to remain lower and fall faster than regional peers, reflecting weaker economic growth, which limits firms’ ability to pass through costs. In addition, services inflation in Thailand is expected to stay below peers, partly because of weaker wage bargaining power in the services sector.

- Medium-term inflation expectations have edged higher but remain within the target range. Looking ahead, inflation continues to face upside risks from geopolitical uncertainty, stronger-than-expected cost pass-through amid a high-cost environment, and a potentially more severe El Niño.

The MPC views 1.0% as appropriate for both price stability and growth support

- The MPC assesses that inflation risks remain but have not increased since the previous meeting. At 1.0%, the policy rate remains appropriate given the inflation outlook and risks, while also supporting slow and uneven growth.

- Thailand can maintain a low policy rate even as global financial markets price in hikes from major central banks. While this could put some depreciating pressure on the Thai baht, a weaker baht may help improve the competitiveness of Thai exports, particularly for small exporters and agricultural products. The BOT will continue to monitor and manage FX movements to curb excessive volatility.

- The MPC stands ready to adjust policy if conditions shift. For inflation risks, it will monitor firms’ cost pass-through and medium-term inflation expectations. For financial conditions, it will monitor serviceability among SMEs and vulnerable households.

IMPLICATIONS

SCB EIC expects the MPC to hold the policy rate at 1.0% through the rest of this year.

- The MPC can hold the policy rate steady despite markets pricing in global rate hikes, given Thailand’s distinct cyclical and structural position:

- Thailand’s inflation is largely driven by external factors, such as global oil prices, and supply-side factors, such as fresh food prices. As pressures from these factors ease, Thai inflation should gradually decline, making a prolonged period of high inflation unlikely.

- Thailand’ ample international reserves give the BOT room to manage FX volatility if episodes of large capital outflows occur, unlike some peers. In addition, the baht had already been under significant appreciation pressure before the war, partly due to idiosyncratic factors such as gold trading, strengthening to around THB 31/USD. Following the outbreak of the war, the baht weakened to around THB 33/USD, broadly in line with its level at the beginning of 2025, which remains within a normal range (versus THB 38/USD at its weakest in 2022). As a result, Thailand may not need aggressive rate hikes to defend the currency even if outflows pick up.

- Thailand's slower growth versus regional peers keeps demand-side inflation pressure subdued, and monetary policy must continue to balance price stability with the need to support the economy, unlike peers with stronger growth.

- In the policy mix, monetary policy is currently playing a stabilizing rather than a stimulative role amid ongoing volatility in global financial markets. Fiscal policy remains the primary tool for cushioning growth, while targeted financial measures, including assistance for retail borrowers and improving credit access for viable SMEs, address tight financial conditions.

- SCB EIC expects the MPC to hold the policy rate at 1.0% throughout this year. Into next year, if inflation declines rapidly and fiscal stimulus fades while growth stays below potential and remains fragile, with retail borrowers and SMEs facing persistent debt serviceability problems, the MPC may consider further monetary easing.