MPC holds at 1% as expected, viewing inflation spike as temporary amid Middle East war, in wait-and-see mode

SCB EIC expects the MPC to remain in wait-and-see mode amid the war situation, likely holding the rate at 1% for the next 1–2 quarters.

Key Summary

|

The MPC voted 6:0 to maintain the policy rate at 1.0%, judging the current appropriate to support the Thai economy amid the Middle East war and heightened uncertainty. Inflation should temporarily rise above the 1–3% target range in few quarters this year due to supply-side factors, before gradually returning to the target range in 2027. Looking ahead, the MPC will monitor the impact of the war on inflation dynamics and inflation expectations, as well as its effects on production and employment, and the scale of additional government stimulus measures.

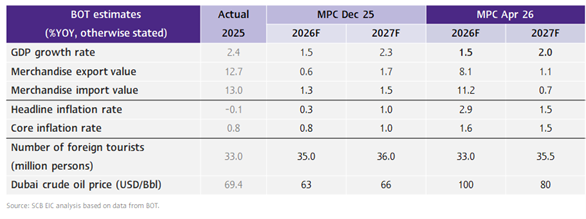

Figure 1: BOT’s Thai economic outlook (as of Apr 2026)

The Thai economy is expected to slow due to the impact of the war, though additional government stimulus measures could provide some upside.

- The MPC expects the Thai economy in 2026 to expand by 1.5%YOY, slowing from 2.4%YOY in the previous year (Figure 1). Without the war, the MPC estimates that the Thai economy would grow by 2.3%YOY.

- The MPC sees room for upside from additional government stimulus. Should new stimulus worth THB 300 billion materialize, GDP growth could be lifted by 0.5–0.7%YOY, though the impact would be temporary and limited to this year.

Inflation is set to rise this year, driven by supply-side factors, before returning to the target range next year, while medium-term inflation expectations remain anchored within the target range.

- The MPC assesses that Thailand’s headline inflation will exceed the target range starting from Q2-2026 for 4 consecutive quarters before declining in 2027 in line with global energy prices, with the 2026 average estimated at 2.9%.

- The risk of persistently high inflation due to de-anchored medium-term inflation expectations is limited, as (1) low likelihood of a wage-price spiral given Thailand's structural labor market constraints (2) medium-term inflation expectations remain within the target range, and (3) domestic demand remains subdued.

The MPC judges policy rate at 1% as appropriate to support the economy. Decisions in upcoming meetings will be data dependent.

- The MPC judges the hold as appropriate, as Thailand's flexible inflation targeting framework allows it to look through a supply-driven, temporary rise in inflation.

- A rate move in either direction at this juncture could increase risks to the Thai economy.

o A rate hike could further weigh on the fragile economy, particularly borrowers’ debt serviceability.

o A rate cut amid uncertainty could affect medium-term inflation expectations. - The MPC will remain in wait-and-see mode and adjust policy based on incoming data, which could lead to different economic growth and inflation scenarios. In a severe case where the current situation lasts throughout 2026, Thai GDP is estimated to grow by less than 1%YOY in 2026, while average headline inflation for the year would exceed 5%.