Exports in February 2026 slowed, while imports accelerated to the highest level in 50 months; monitoring the impacts of the Middle East war and the outlook for US tariffs.

SCB EIC assesses that Thailand’s international trade this year will face increasing external pressures.

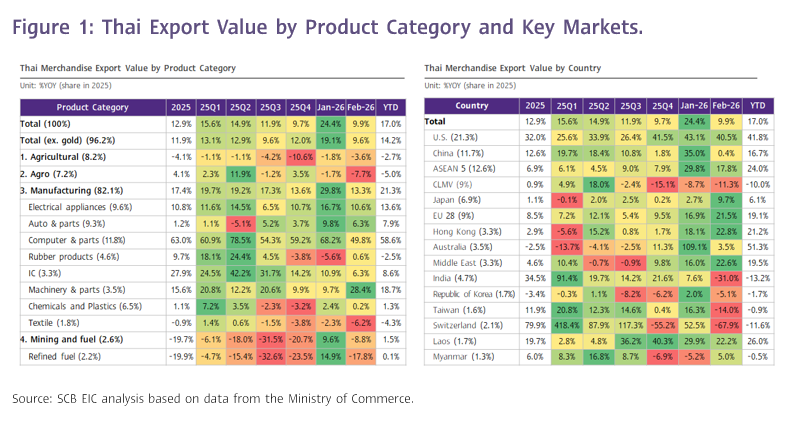

Thai exports in February 2026

Thai exports in February 2026 slowed but still recorded strong growth of 9.9%YOY, with export value reaching USD 29,439.7 million. This represented a deceleration from the previous month’s high growth of 24.4%YOY and was lower than earlier estimates (SCB EIC and the Reuters Poll median projected 15.8%). Seasonally adjusted export value contracted sharply from the previous month by -11.1%MOM_SA. Overall, Thai export value during the first two months of this year still expanded strongly by 17% (Figure 1 and 2), prior to the onset of the Iran conflict on February 28.

Exports this month were mainly driven by electronic products, while the US remained a key trading partner.

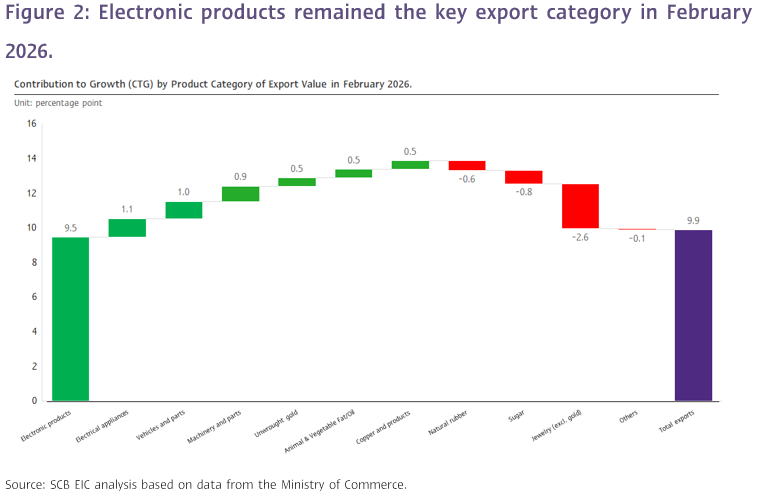

(1) Exports of electronic products expanded strongly by more than 56.8%YOY, including computers, equipment and parts; electronic calculating machine; Teleprinters, telephone sets and parts; radio transmission equipment, telegraph, telephone and television equipment; and electrical transformers and parts, which increased by 49.8%, 41.8%, 217.6%, 251.5%, and 47.1%, respectively. Growth continued to be supported by the upcycle in the global electronics cycle and expanding investment in the electronics industry and Data center infrastructure worldwide. Exports of Thai electronic products to 11 out of the 15 key trading partners continued to expand. Overall, electronic products contributed 9.5 percentage points to Thailand’s export growth (CTG) this month, accounting for almost the entirety of the total export expansion of 9.9%.

(2) Thai exports to the US expanded strongly by 40.5%YOY, slightly moderating from the previous month. Exports of electronic products not yet subject to additional US import tariffs surged by as much as 97.8%, while other product categories (excluding electronics) grew by 9.7%, reflecting continued strong demand for Thai products in the US market despite relatively high import tariff barriers of 19% (before being reduced to 10% under Section 122 following the Supreme Court’s ruling that the US administration does not have the authority to impose import tariffs under the International Emergency Economic Powers Act (IEEPA)).

Among Thailand’s key export products to the US, 13 out of the top 15 items recorded solid expansion. Overall, exports to the US contributed 7.3 percentage points to Thailand’s export growth (CTG) this month, out of the total export expansion of 9.9%.

(3) Gold exports expanded by only 18.2%YOY, slowing markedly from the strong growth of 136.2%YOY in the previous month, partly reflecting the decline in global gold prices during this period. Exports of unwrought gold contributed only 0.5 percentage points to Thailand’s export growth (CTG) this month, compared with a much larger contribution of 2.7 percentage points in the previous month.

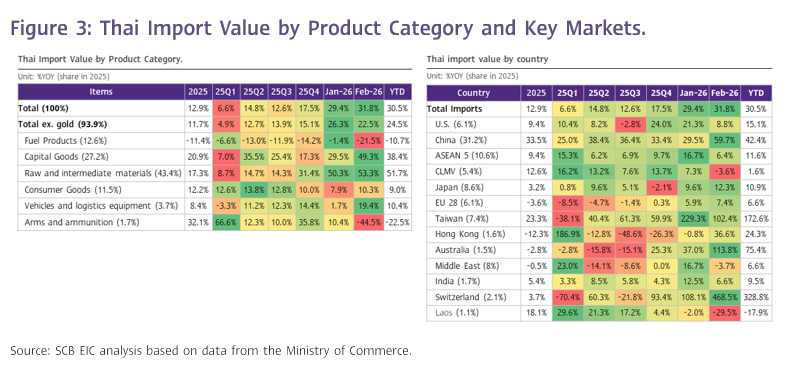

Imports surged to the highest level in 50 months, driven by raw and intermediate materials, and capital goods—particularly gold.

The value of merchandise imports in February stood at USD 32,273.3 million, expanding by 31.8%YOY—the highest level in 50 months. This marked an acceleration from 29.4%YOY in the previous month and was higher than earlier estimates (SCB EIC projected 20.5%, while the Reuters Poll median forecast was 25%). The expansion in imports was mainly driven by the following key categories (Figure 3 and 4).

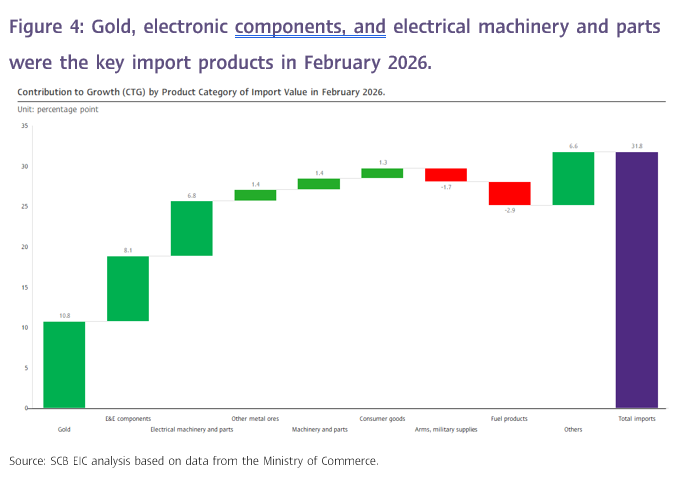

(1) Imports of raw and intermediate materials expanded strongly by 53.3%YOY, close to the level recorded in the previous month. This category contributed 22.5 percentage points to Thailand’s import growth (CTG) this month—accounting for more than half of the total import expansion of 31.8%YOY. Key imported products included gold and electrical and electronic components, which increased by more than 165% and 84.8%, respectively (CTG: 10.8% and 8.1%). Imports of electrical and electronic components were partly driven by demand for upstream and midstream inputs used in production and exports, with Thailand relying on major suppliers such as China and Taiwan for these products.

(2) Imports of capital goods expanded strongly by 49.3%YOY, accelerating from 29.5%YOY in the previous month. This category contributed 11.7 percentage points to Thailand’s total import growth (CTG) of 31.8%YOY. Key imported items included electrical machinery and parts, and mechanical machinery and parts, which increased by 91.0% and 19.2%, respectively (CTG: 6.8% and 1.4%). This partly reflects Thailand’s still-limited domestic production capacity for such capital goods, alongside rising investment trends in technology-related industries, such as Data center infrastructure, which have led to stronger demand for machinery and technology-related imports.

The customs-basis trade balance recorded a continued deficit of USD -2,833.6 million this month. Overall, during the first two months of this year, Thailand registered a cumulative trade deficit of USD -6,137.1 million.

SCB EIC assesses that Thailand’s international trade this year will face increasing external pressures, with the Middle East conflict and higher US import tariffs further exacerbating the trade deficit.

1) Middle East conflict: Although the overall impact on Thai exports is expected to be relatively limited—given Thailand’s low dependence on the Middle East market (accounting for 3.7% of Thailand’s total export value in 2025)—some industries may face significant effects due to their high export concentration in the region. These include wood and wood products (18.2% of total exports in this category), fresh/chilled/frozen fish (15.4%), rice (13.4%), and automobiles, equipment and parts (13.1%).

In addition, Thai exports may be indirectly affected through a slowdown in the global economy, particularly in Asian and European markets, which rely heavily on energy imports from the Middle East (together accounting for 65% of Thailand’s export markets). Nevertheless, the conflict in the Middle East is likely to push up prices of Thai export products linked to oil and commodities, such as palm oil, cassava, sugar, and natural rubber (Figure 5, left).

2) Thailand’s trade balance is likely to deteriorate further in line with rising energy prices, as Thailand is a high net energy importer, accounting for around 8% of GDP (Figure 5, right), with as much as 59% of total energy imports sourced from the Middle East. In addition, prices of other imported raw materials and transportation costs are also expected to increase, further worsening the existing trade deficit trend since the COVID-19 crisis—particularly due to the substantial rise in imports from China—thereby weighing on overall economic growth.

3) US import tariffs under Section 301: Although Thai exports may receive short-term support from the reduction in US import tariffs to 10% after the US Supreme Court ruled that the Trump administration did not have the authority to impose import tariffs on trading partners under the International Emergency Economic Powers Act (IEEPA), the US government subsequently shifted to exercising authority under Section 122 of the Trade Act of 1974, announcing a temporary 10% import tariff on all countries for a period of 150 days (from February 24 to July 24).

However, on March 12, the United States further announced an investigation into 16 trading partners under Section 301 of the Trade Act of 1974 concerning issues related to structural excess capacity, with Thailand included among the countries subject to investigation.

SCB EIC finds that the US trade deficit with Thailand increased in 2025, with Thailand rising to 7th place among countries with the largest trade surplus with the United States, up from 10th place in 2024. This development reflects a heightened risk that Thailand may face additional US import tariffs after July under Section 301 following the completion of the investigation (Figure 5, middle).

In the announcement of Thailand’s international trade figures for February 2026, the Ministry of Commerce released its latest projections for Thai export value in 2026 under three scenarios as follows:

- Best-case scenario: 1.1%YOY

- Baseline scenario: -1%YOY

- Worst-case scenario: -3%YOY

SCB EIC is currently reviewing Thailand’s 2026 economic outlook, including the directions of export and import values, under the evolving Middle East conflict scenario, and will release updated projections by the end of March.